Those MBS's would not have existed if it werent for the people lying on their loan applications.

Untrue.

So good grief to you who doesnt care what causes something....all you care about is the end result.

The end result was a collapse of the financial sector far, far out of proportion to the collapse of mortgages, all due to the fact that the banks took mortgage debt and gambled with it, as they were allowed to do because of the repeal of Glass-Steagal.

The housing market had a bubble. The bubble burst. Mortgages were defaulted on. If the problem lay with the mortgages themselves, it would have stopped there, and no serious damage would have been done to the economy. But because the mortgage debt had been used by the banks to leverage additional money-making instruments, those crashed when the mortgages were defaulted, and the economy went into a tailspin.

If you're going to talk about cause and effect, you need to identify the real cause correctly. You have not done that; in fact, what you have done is to put forth a scapegoat that can divert attention from the real culprits.

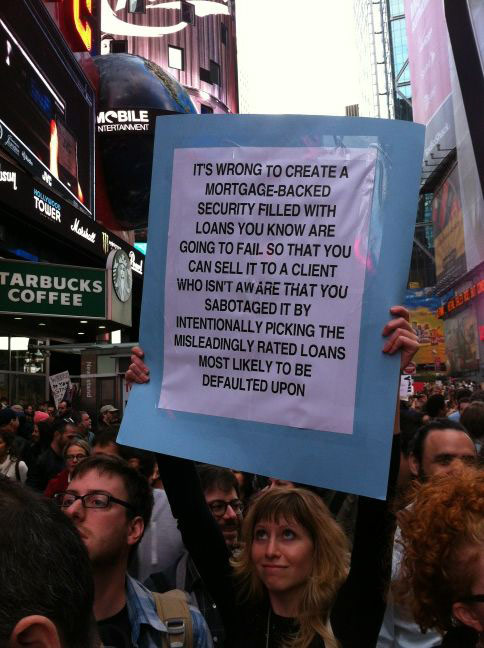

The sign is also alleging deliberate misdeeds by the vendors of MBSs, in that it says they knew those instruments were going to fail. I don't know if that's true or not, but what I do know is enough to indict the big banks, and the federal government for repealing the regulations that used to keep this kind of crap from happening. Those are the real bad-guys here, not people who defaulted on their mortgages.