Q: I did the math and it seems like a family of four (two adults age 40) and two children would pay about $12,000 a year in premiums for a silver plan, along with 70 percent of the medical costs and $1000 to $3,000 deductibles. Thats a lot of money. I heard there are limits on how much you have to spend on premiums and out-of-pocket expenses. Can you explain?

A: The law limits the percentage of your income that you have to spend on premiums, as well as the amount you have to spend out-of-pocket on deductibles and cost sharing.

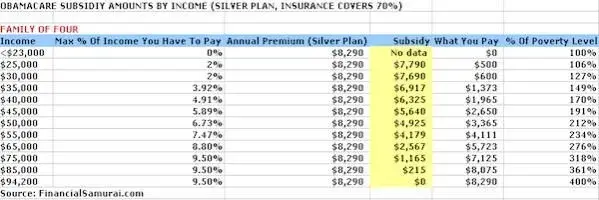

The premium limits vary from 2 percent to 9.5 percent, depending on income. Out-of-pocket expense limit, which changes each year; will be $6,350 for an individual and $12,700 for a family in 2014.

Out-of-pocket expenses include money spent on reaching your deductible and cost sharing (coinsurance and co-pays) but not premium costs. This applies to individual plans sold both inside and outside the exchange.

Q: Can you give me an example of how the out-of-pocket cap works?

A: Say you have a plan with a $2,500 deductible. You fall off your skateboard and break a lot of things you think you might need later on in life.

If you have a silver level plan that pays 70 percent, youll pay 30 percent of your $50,000 hospital bill you needed lots of fixing until youve paid out $6,350, which is your (maximum out-of-pocket for the year).

Insurance kicks in at that point. You still have to pay the premiums, but youre done paying health care expenses so long as they are for essential health benefits for the year.

There's plenty of choices.

There's plenty of choices.