Dad2three

Gold Member

A summary I wrote six years ago. Still very timely today.

----------------------------------------

An hour-long program on the origins of the current financial crisis, was put together by Fox News in 2008. It contains a great many clips from various officials who were involved, interviews by news people, etc. They called it "Saving Our Economy". Someone put it on YouTube, in six segments. Go there and do a search on that title, and you should get all six segments. They vary from 5 to 10 minutes each, about 45 minutes running time total (no commercials).

It's an excellent explanation of how the crisis started, who did what, what the results were, etc. A real must-see.

Here's a summary:

-----------------------------------------

Sept. 23, 2008: Treasury Secretary Henry Paulson: "The events leading us here began many years ago, starting with bad lending practices by banks and financial institutions, and by borrowers taking up mortgages they couldn't afford."

-----------------------------------------

The Federal National Mortgage Association (FNMA, or "Fannie Mae") was created in 1938 during the Great Depression. to create a market for mortgages where they could be bought and sold.

In 1968, Lyndon Johnson and a Democratic Congress spun off Fannie Mae so that it would not show up in the Federal budget. But the Federal govt was always there, ready to bail out Fannie Mae if problems happened. This enables Fannie Mae to offer lower rates for the mortgages it bought, since it was not taking the risks that other banks and institutions had to. In 1970, the Federal Home Loan Mortgage Corporation ("Freddie Mac") was formed, to create competition for Fannie Mae, since ordinary banks could NOT compete with the government-backed rates they offered.

The Community Reinvestment Act (CRA) was passed by a Democrat Congress and signed by Jimmy Carter in 1977. It made sure banks were lending to people of all colors and income levels. But things quickly began going off the rails, as activist groups found a new weapon in the law: The could start suing lenders for discrimination if they didn't lend to enough minority families, regardless of the families' ability to pay the loans back as promised. Banks began making riskier and riskier loans for fear of having to fight expensive lawsuits.

Community groups began bullying the banks, especially one called the Association of Community Organizers for Reform Now ("ACORN"). It hired several specialized lawyers, including a young man named Barack Obama, to teach its employees how to go to the homes of bank CEOs and senior officers, harassing and publicly embarrassing them while remaining within the limits of local law to avoid prosecution.

At one point, ACORN brought a lawsuit against a thrift merger in Illinois, insisting that the lending institutions had not made as many loans to minorities as ACORN thought they should. The bank replied that such loans would be financially irresponsible, and would put ALL the bank's customers at unacceptable risk. ACORN prevailed in court, and banks began making more and more risky loans to home buyers who could have never qualified for those loans under ordinary circumstances.

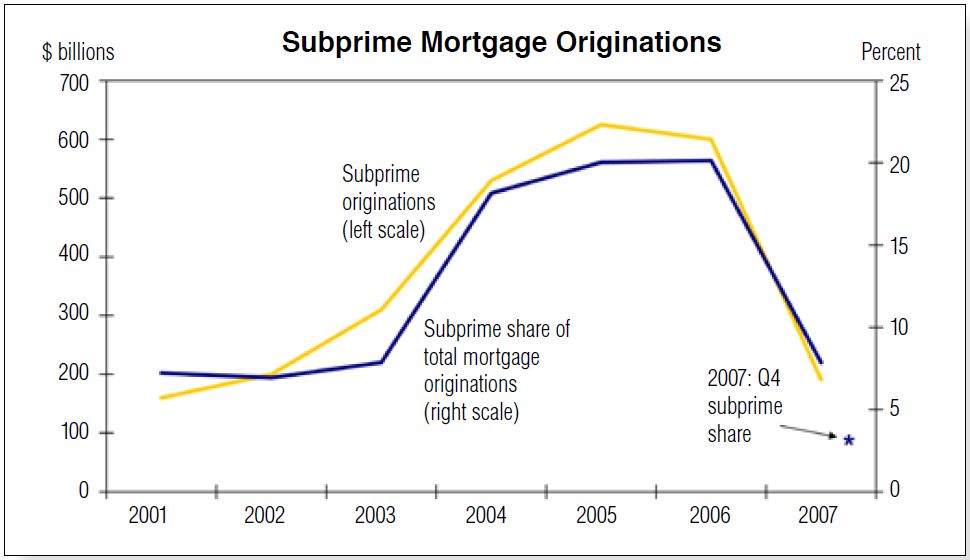

In late 2000, in the last days of the Clinton administration, the government ordered Fannie and Freddie to increase the numbers of these risky ("sub-prime") mortgages they were buying from banks and lending institutions across the country. They did, lowering their rates and buying more and more, until fully half their portfolios consisted of these risky sub-prime mortgages, combined and packaged in various ways.

The Bush administration raised red flags starting in April 2001. Their 2002 Budget Request declared that the size of mortgage giants Freddie Mac and Fannie Mae is "a potential problem" because financial trouble in either one of them "could cause strong repercussions in financial markets".

In 2003, the White House warning about Fannie and Freddie, was upgraded to a "Systemic Risk that could spread beyond just the housing sector".

As Fannie and Freddie continued to lower their rates and buy mortgages, lenders made more and more mortgages to buyers with questionable ability to pay, safe in the knowledge that they could immediately turn around and sell the mortgages to the government-sponsored Fannie and Freddie, thus avoiding any consequences if the loans were later defaulted. They were happy to make more and more such mortgages, collecting fees for each and selling the mortgages to F&F.

Countrywide Financial chairman Angelo Mazzillo literally started screaming at Wall Street Journal editor Paul Gigot, when Gigot asked him about the wisdom of making so many loans to buyers unlikely to pay them back. Mazzillo insisted loudly that Gigot had no idea what he was talking about, did not understand the first thing about mortgage lending, etc., etc. He failed, however, to answer any of Gigot's questions in even the simplest terms or explain why they were "wrong".

(to be continued)

Loans that were under government regulation did better than private loans, especially if they were regulated by the "Community Reinvestment Act."

Center for Public Integrity reported in 2011, mortgages financed by Wall Street from 2001 to 2008 were 4½ times more likely to be seriously delinquent than mortgages backed by Fannie and Freddie.

It is clear to anyone who has studied the financial crisis of 2008 that the private sector’s drive for short-term profit was behind it.

More than 84 percent of the sub-prime mortgages in 2006 were issued by private lending. These private firms made nearly 83 percent of the subprime loans to low- and moderate-income borrowers that year. Out of the top 25 subprime lenders in 2006, only one was subject to the usual mortgage laws and regulations.

The nonbank underwriters made more than 12 million subprime mortgages with a value of nearly $2 trillion. The lenders who made these were exempt from federal regulations.

Lest We Forget Why We Had A Financial Crisis - Forbes