As for your links, the national average is 26% for individuals and 33% for families, Texas is at 24% and 25% respectively, family premiums far surpass the cost of individuals, BTW Texas is 8% below the average for families, most would consider 8% significant....

Also, your new math is interesting when you claim their premiums are slightly below the national average.....

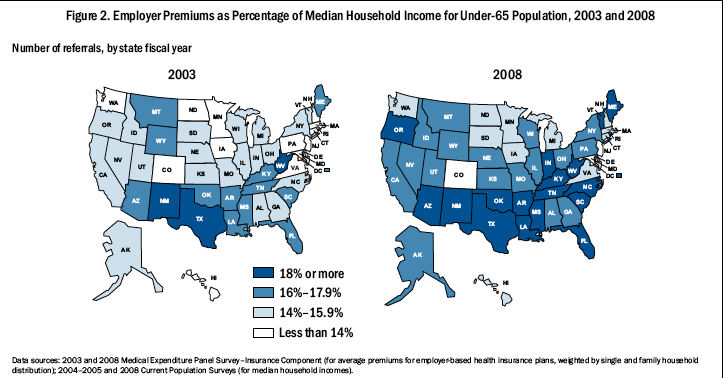

What do you notice about all of the states that had the highest costs in 2003 (i.e. those with average premiums above 16% of median household income: Texas, New Mexico, Arizona, Wyoming, Montana, Kentucky, Tennessee, Mississippi, Louisiana, Tennessee, Florida, South Carolina, New York, and Vermont)? Almost

all of them saw premium growth at or below the national average from 2003-2008 (the only exceptions were New York, Vermont, and Arizona; Mississippi and Florida saw growth in family premiums above the national average). Why is that? In part the cost growth will reflect local factors--certainly that's what you're arguing about Texas--and in part we would expect states that already have the highest rates to grow more slowly than states that have a ways to go to "catch up."

But consider this. We know from

Kaiser that from 1994-2003, the average annual growth in health care expenditures in Texas was 5.3%. If we assume for a moment that the growth in insurance premiums closely tracks the growth in expenditures (which may or may not be correct), if we continued this trend we would expect to see a roughly 29% growth in premiums costs over a five year period (which you can compare with Texas's actual 25% growth rate in employer premiums from 2003-2008). So premiums in Texas over that period grew at about 4.7% annually, not 5.3% (which they would if 1) premiums track costs and 2) the 1994-2003 trend continued through 2008). So let's say we could attribute that entire difference to malpractice reform--that's a 0.6% reduction in cost growth every year. That's actually not very far-fetched, as this assumption-laden back-of-the-envelope calculation comes remarkably close to

the CBO's estimates of how much tort reform would reduce spending:

CBO now estimates that implementing a typical package of tort reform proposals nationwide would reduce total U.S. health care spending by about 0.5 percent (about $11 billion in 2009). That figure is the sum of a direct reduction in spending of 0.2 percent from lower medical liability premiums and an additional indirect reduction of 0.3 percent from slightly less utilization of health care services.

Does tort reform have zero effect on costs? No, but the claim that it's a silver bullet (with its ~0.5% reduction in cost growth annually) to controlling health care costs seriously overestimates the magnitude of its effects. Texas is doing slightly better than it was a decade ago. And since you don't like my usage of words like "significant" or "slight," I'll put a number on that--our back-of-the-envelope exercise here suggests annual cost growth might've been reduced by between a half a percent and three-quarters of a percent. Hardly an authoritative estimate but it does agree with the literature.

Let's see, so when 34 of 50 states have significantly larger increases in both single & family premiums than Texas over the same period of time, you should consider revising your use of slightly, just a thought....

Without examining provider consolidation, state premium oversight rules, coverage initiatives, benefit levels, insurance markets, or even the variable you're claiming is determinative (medical liability climate), it's tough to say why Texas falls where it does and other states fall where they do. For example, Kentucky's family premium growth rates were comparable to those of Texas and its single premium growth rate was actually lower, yet it has the

absolute worst medical liability climate rating. If medical liability climate is the key factor to cost growth, how can a state that's rated worst be doing as well as one that has one of the best ratings?

Your use of fig. 2 shows even more support for my position. The median household income for 16 of the 18 states with an increase of 18% or more for Employer Premium cost are beneath the national median average for household incomes....

I'm not sure what you're trying to say here.

Every state had an increase in family premiums of more than 18% between 2003 and 2008--the smallest increase was Michigan's 20% increase over that period.

The map is showing you, as it says, employer premiums as a percentage of median household income. States marked as "18% or more" have the most expensive premiums--with respect to incomes in the state--in the nation. That 18% isn't a growth rate (i.e. it's not "an increase of 18%"), that's the percentage of incomes going toward health insurance premiums in that state.

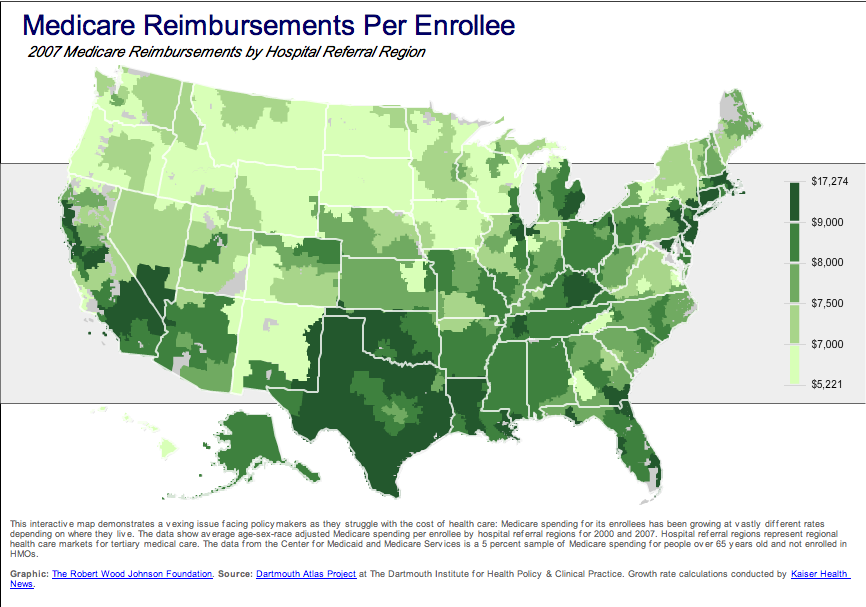

The 5% sampling in your second map fails to break down Medicaid vs Medicare

Of course it breaks down Medicaid vs Medicare--it refers

only to Medicare reimbursements. Medicaid doesn't need to be disentangled because it isn't involved here at all (and since Medicaid reimbursements differ from state to state, we wouldn't want it to be).

it does however clearly show that population growth in Texas far exceeds all other major metro areas, hence more Medicare claims,

"Reimbursements per enrollee" is independent of population. This is a picture of per capita spending, not total spending.

and Texas also has the second (closing in on #1) largest population of illegal immigrants.....

And?