If the fed funds rate were to return to 3.5%, the 10 year would need to return to 4.7% and the 3 month would return to 3.5%. This would double our interest payments, and also make it impossible to service, considering the increase would have just as negative impact on the economy as leaving it as zero.

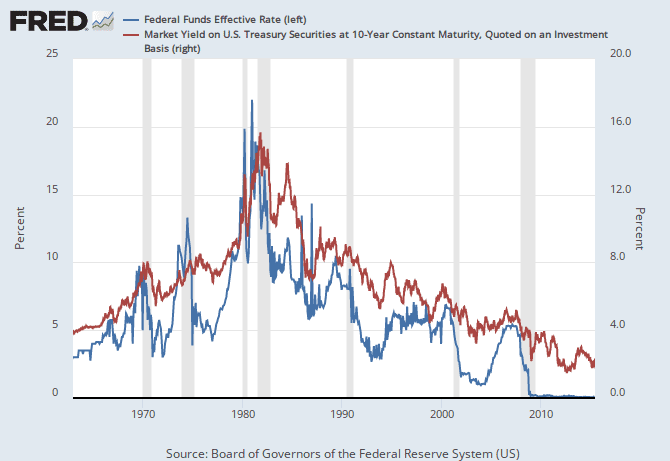

The Fed Funds rate is only vaguely related to the 10 year yield. For example, our current fed funds rate is essentially 0. Yet the 10 year Treasury Notes interest rates are around 2.2%. At the end of 2013, it was also essentially 0. And interest rates on the 10 year treasury note shot up to 3%. In January of this year, the fed funds rate was essentially 0. And the 10 year treasury note was 1.7.

A vacillation of nearly double....on the exact same fed funds rate.

And when the Fed funds rate was at 4%, as it was in December 2007, the 10 year Tnote yield was only a quarter percent higher. Yet in december of 2009 when the Fed Funds rate as at essentially 0 (0.12%), the 10 year Tnote yield was at 3.85.

Barely a half point tick downward in the yield despite the fed funds rate dropping almost 8 times more.

When the fed funds rate is higher, the 10 year Tnote is generally slightly lower. From 2006 to 2008 the Fed Funds rate hovered at or very near 5%. While the 10 year Tnote yield hovered closer 4.5, dropping as low at 4 (twice) and climbiung as high as 5 (twice).

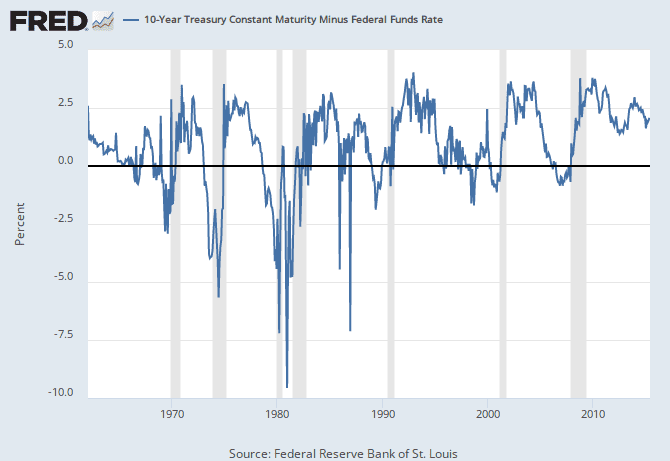

So your estimates of the Tnote needing to be a clean 1.2% higher than the fed funds rate is just not supported by the historical evidence. At least not in the last 10 years.

Very bad examples, for a number of reasons. Especially on your first point in explaining the relationship between yields and zero lower bound. Bond yields were never constrained by zero lower bound like the shorter term 1 and 2 year treasuries. Longer term yields on the other hand, have extreme sensitivities to increases in the Fed Funds Rate. The

Federal Reserve Bank of San Fransisco has already explained why pretty well.

Also, your time period covers 10 years we've had interest rates near record lows at a constant floating rates, which means rates hold steady for a very long period of time (more than 2 financial quarters or more). The scenario I discussed requires interest rates to be free flowing (or increasing). This is what interest rates do during normal times, not the time frame you have used. The time frame you've used is not even a good explanation of interest rates and yields.

To understand how yields work, you need to understand some basic facts: 1) the short term interest rates are influenced by central banks however 2) long term interest rates are influenced by supply and demand.

T-Bills and notes are more predictably influenced by the fed funds rate than bonds because the fed funds rate and bonds are competing investments in the money market. Bonds, on the other hand, are less influenced because of their longer maturities, which means more can happen within a lifetime. This means bonds have the potential to undergo huge price changes, which is what happens when yields rise, which will occur when the fed funds rate rises.

Fed funds rate drops when the Fed purchase assets (or bonds) in the open market, and the Fed is still one of the largest net acquirers of US Treasuries. Bond yields are highly sensitive to supply and demand, which depends on whether or not the Treasury is issuing fewer bills than investors want. If the Fed were to decide in the recent future to increase interest rates, this would require the Fed to sell treasuries instead of purchasing them. Selling more bonds puts more assets into the open market, decreasing their price, and increasing yields. That's really basic.

In fact, you can probably see that relationship if you realistically look further than the past 10 years.

As you can see, interest rates and 10 treasury yelds are more likely to in tandem than not. There are a few exceptions. The past 10 years being one of them.

Also, the spread between the 10 year treasuring and the fed funds rate has always been higher than 1.2% under normal circumstances, so I don't understand what you are talking about on your last sentence.