Nope. A crappy mortgage would be one, for instance, that was given to someone with a low credit score with a very low, or no, downpayment. The technical term for a crappy mortgage is subprime.

But if the borrower can pay it, who cares? It's not crappy if the borrower can repay. A subprime may be

riskier, but it's only crappy if it enters delinquency, which would turn the security it backed toxic, which is what caused the collapse of the secondary mortgage markets, which caused the credit freeze, which caused the recession.

Not all crappy mortgages defaulted. Not all conforming mortgages escaped default.

So I see what you're doing...you're applying your own standard to "crappy". You are interchanging "crappy" with "risky". Sure, those subprimes were

riskier, but the risk paid off for the GSE's since their mortgages entered delinquency at rates far below that of private labels.

Again, that's not surprising considering they bought better mortgages.

So did they buy "crappy" mortgages, or did they buy "risky" mortgages? There's a difference. Subprimes were risky, but private-label subprimes were crap. They were crap because they entered delinquency at rates far higher than their GSE counterparts. So you need to make up your mind; did the mortgages GSE's backed cause delinquencies or not?

Your own source showed the government forced them to buy 50% subprime loans, rising to 56% subprime loans. This isn't a claim I manufactured.

Rising to 56% when? After the private label subprime market had already popped. And what of the loan performance for the GSE-backed loans? Consistently better than that of private labels. Hence, GSE-backed loans were not responsible for the bubble or the pop of that bubble. Just like all mortgages, they were swept up in the aftermath of the

private label mortgages defaulting and the recession.

They were worse than the ones they bought pre-bubble, obviously.

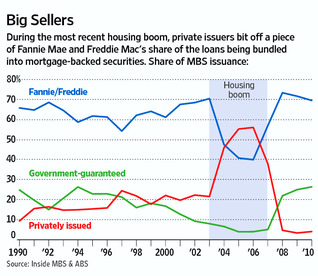

NO THEY ******* WEREN'T! That's why the line on the chart below for GSE's remains steady and consistent as the line on the chart for private label subprimes and subprime ARMS shot up:

Default rates for GSE's rose in the aftermath of private labels popping the bubble, along with

all other kinds of mortgages. So GSE loans were no worse than they were prior to the collapse and bubble, as the chart shows.

eah, their crappy loans took longer to default. And?

No, they ******* didn't!

Look at the goddamned chart! The defaulting of GSE-backed loans started the same time the defaulting of all other loans happened,

as the ******* chart above shows. So just like all the other non-subprime mortgages, GSE-backed ones entered delinquency at the same time as other loans because there was a recession that caused job loss which caused borrowers to not be able to repay.

A few hundred billion dollars in government bailout funds disprove your claim.

They had to get the bailout because the private label subprime bubble popped mid-2006, and the resulting delinquencies and foreclosures led to a drop in home prices, which led to a cooling of the market, which led to job loss because the only growth that happened from 2004-7 was because of the housing bubble. Job loss means the borrowers weren't able to repay, which means their mortgages entered delinquency. Because GSE's are

government-sponsored, they had to get bailed out. But they wouldn't have had to have been bailed out if private label subprimes hadn't created and popped a bubble. Again, that's why

delinquency rates for all mortgages rose starting in 2008.