But here are the facts: The housing price bubble started in 1997. The first sub-prime MBS was created in 1997. I can find no record of them before 1997.

I think you'd be hard pressed to find much of anything from before 1997, when the internet really took off.

this is the best you have?

Look, guy, even the Banking Industry isn't blaming the CRA for the crash.

Community Reinvestment Act had nothing to do with subprime crisis - BusinessWeek

The Community Reinvestment Act, passed in 1977, requires banks to lend in the low-income neighborhoods where they take deposits. Just the idea that a lending crisis created from 2004 to 2007 was caused by a 1977 law is silly. But it’s even more ridiculous when you consider that most subprime loans were made by firms that aren’t subject to the CRA. University of Michigan law professor

Michael Barr testified back in February before the House Committee on Financial Services that 50% of subprime loans were made by mortgage service companies not subject comprehensive federal supervision and another 30% were made by affiliates of banks or thrifts which are not subject to routine supervision or examinations. As former Fed Governor Ned Gramlich said in an August, 2007, speech shortly before he passed away: “In the subprime market where we badly need supervision, a majority of loans are made with very little supervision. It is like a city with a murder law, but no cops on the beat.”

.....

Finally, keep in mind that the Bush administration has been weakening CRA enforcement and the law’s reach since the day it took office. The CRA was at its strongest in the 1990s, under the Clinton administration, a period when subprime loans performed quite well. It was only after the Bush administration cut back on CRA enforcement that problems arose, a timing issue which should stop those blaming the law dead in their tracks. The Federal Reserve, too, did nothing but encourage the wild west of lending in recent years. It wasn’t until the middle of 2007 that the Fed decided it was time to crack down on abusive pratices in the subprime lending market. Oops.

Sub-prime loans performed well, when the prices of homes was going up. They performed well because if the person ran into trouble, they could sell the house for more than the value of the mortgage, because prices were going up.

Thus, the bank made a great return on the loan with high interest rates (because they were sub-prime), and got their money back when they sold the home for more than the original loan.

The foreclosure rate on loans in the 90s wasn't all that great. They still performed well, only because lowering the mortgage standards, brought tons of people into the market, driving up prices. That's all.

The government could do the whole thing all over again, and drive up housing prices, and during the up swing in prices, sub-prime mortgages would all perform well, all over again.

None of the rest of your response changes or contradicts anything I said. So I'm not sure why you bothered posting it.

A: There is plenty of information on mortgages before 1997. I know... I read it.

B: When the law was created is irrelevant compared to the fact that until 1997, sub-prime loans were never securitized, or sold in MBSs.

C: Doesn't matter what portion of loans came from where. Once the government guaranteed the loans, they were legitimized in the broader market.

Remember Collateralized Debt Obligations themselves, were created by government. Government created them, and the market adopted them. Banks learned how to sell securities from the government. Without government, a Mortgage Backed Security, would have never existed.

My point, is that the private market takes it's que from the government. When Government put their name behind sub-prime loans, in the name of CRA, they legitimacy to those loans.

See? Something had to happen in 1997. You can't explain that with Bush did xxx. And you can't tell me that all the mortgage lenders on in the country magically all decided at one magic moment, to start flooding the market with sub-prime loans.

When I read the accounts from mortgage lenders before 1997, the common answer is that no sub-prime loans were ever sent in for rating by rating agencies, because they were already assumed to be junk on the risk rating. Why rate anything that you know has a junk status before it is ever rated?

Getting that key rating is absolutely required to getting money for sub-prime loans. Remember, most mortgage companies do not make mortgages to own.... they make them to sell. Without that AAA rating, you can't sell your mortgage backed securities. Without being able to sell those mortgage backed securities, you can't make new loans.

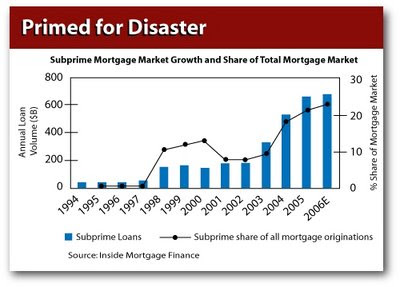

So prior to 1997, the sub-prime market was completely flat, and I argue, would have stayed that way forever, if not for one change. In 1997, Freddie Mac signed a deal with Bear Stearns and First Union (Wachovia), to guarantee sub-prime loans under the CRA.

Suddenly, sub-prime loans bundled in mortgage backed securities could get a AAA rating, and guaranteed by a Government Sponsored Enterprise. Then you say "most sub-prime loans were not at institutions governed by the CRA"? Of course. We would expect that.

Most Mortgage Backed Securities are not created at GSEs, and yet the government created MBS to begin with. They never existed before government made GSEs. The market followed governments lead. This is normal and expected.

And isn't interesting that some of the biggest failures came with institutions with direct government ties? Countrywide was one of the leading mortgage originators, praised by Fannie Mae for meeting their lending goals. Bear Stearns, and Wachovia? Two of the first banks to sign the deal selling sub-prime loans with guarantees by Freddie Mac? Coincidence?

Did the government start the CDO biz?

Did the government start the CDO biz?