Navigation

Install the app

How to install the app on iOS

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: This feature may not be available in some browsers.

More options

Style variation

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Democrats Caused The Global Financial Meltdown

- Thread starter KissMy

- Start date

Titanic Sailor

Senior Member

- Aug 31, 2009

- 1,908

- 149

- 48

Oh, Bush and the GOP helped get us here, and I must have missed the vote where Democrats opposed Bush...................

and now, well, we are racing down hill my friends..................., and nothing but rocks at the bottom.

and now, well, we are racing down hill my friends..................., and nothing but rocks at the bottom.

KissMy

Free Breast Exam

- Thread starter

- #105

Committee on Oversight and Government Reform released a report on "The Role of Government Affordable Housing Policy in Creating the Global Financial Crisis of 2008"

PRIOR TO DEREGULATION --September 1999-- New York Times

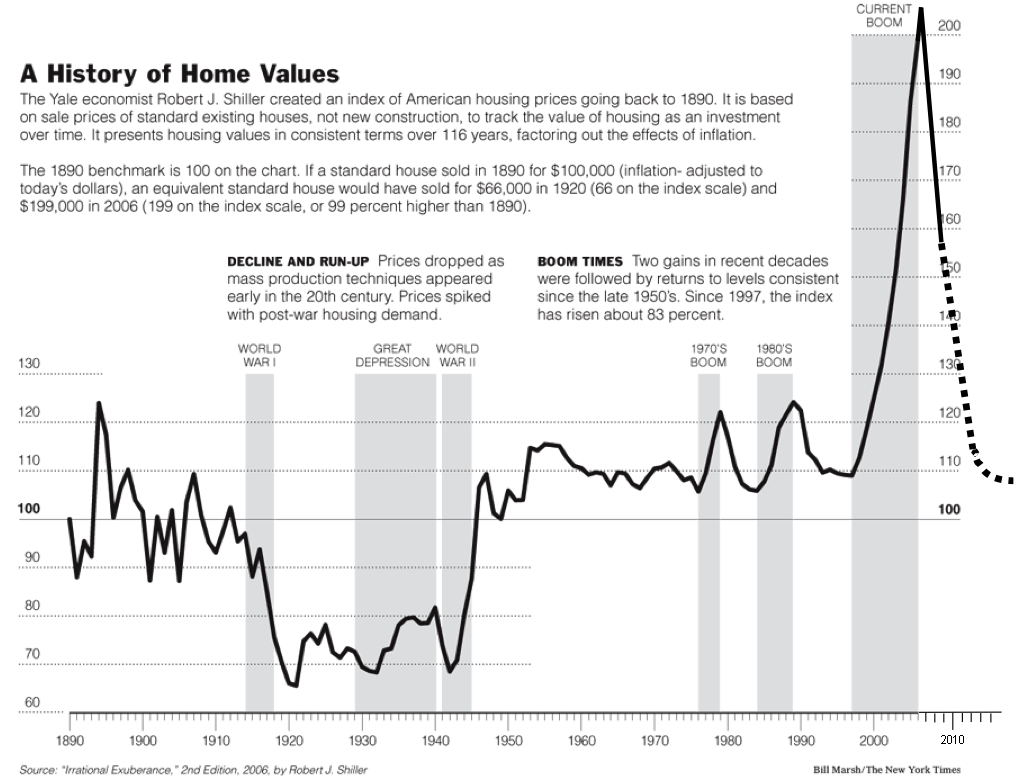

See Housing price chart. The prices shot up in 1997 due to CRA enforcement. That was 2 years prior to deregulation. Deregulation allowed these already ticking time bomb risky CRA assets to be sold to other countries & banks causing the contagion to spread world wide. Deregulation was not the prime cause it just added fuel to the fire.

GSE Conservatorship "In 2008, Fannie and Freddie have purchased about 80% of all new home mortgages in the United States."

The bailout for Fannie & Freddie was larger than all the other banks combined. The other banks have paid back nearly all the tarp funds while Fannie & Freddie continue to require more tax payer funds. They will not be paying us back!

"In retrospect, President Clintons rebranding of prudent down payments of 10 to 20 percent as barrierto home purchase takes on great significance. As with the 1995 CRA reform and the Clinton Administrations decision to allow the GSEs to count subprime loans toward their affordable housing goals, this represented a shift in government policy from one that emphasized equity of procedure to equity of outcome. This emphasis on equity of outcome inevitably created tremendous pressure on regulated institutions to make more loans to low-income borrowers. It also created pressure for secondary market investors such as Fannie Mae and Freddie Mac to buy these loans. The correspondingly lower emphasis on how the loans were being made inevitably meant less attention would be paid to their quality and sustainability.

A Freddie Mac spokeswoman later acknowledged that the Clinton HUDs decision on subprime loans forced us to go into that market to serve the targeted populations that HUD wanted us to serve. Clintons HUD Assistant Secretary William C. Apgar, Jr. has since called the decision a mistake, while his former advisor Allen Fishbein called the loans that the GSEs started buying to meet their affordable housing goals contrary to good lending practices, and examples of dangerous lending. President Clinton himself acknowledged his role in efforts to loosen mortgage lending standards when he admitted that there was possible danger in his administrations policy of pressuring Fannie Mae to lower its credit standards for lower- and middle-income families seeking homes. These accumulated government affordable housing policies, including the Clinton Strategy, trapped millions of Americans in mortgages they could not afford."

"Nonprime loans, which accounted for only 34% of the GSEs risk exposure at the end of 2008, were suffering a 6% delinquency rate, accounting for 90% of the GSEs losses. Put another way, the GSEsnonprime loans were 14 times more likely to be in serious delinquency than their prime loans. In the end, failures on nonprime GSE mortgages may account for the failure of roughly 1 in 6 home mortgages in the U.S., or 8.8 million foreclosures. The continuing losses caused by Fannie and Freddies binge on junk mortgages have already cost the taxpayers dearly. Under the terms of their conservatorship, the U.S. Treasury is committed to inject up to $400 billion of capital into Fannie and Freddie to offset their losses and maintain solvency. These capital injections take the form of Treasury purchases of preferred stock in the companies."

"Even more than Wall Street firms, Fannie and Freddie used high leverage to borrow money and gamble on low-down payment affordable and speculative mortgages. Unlike Wall Street, however, the GSEs did this with the mandate and the blessing of Congress and successive Administrations, which encouraged them to use their government-granted competitive advantages to engage in a race to the bottom, boosting the national homeownership rate for political gain."

"Washington must reexamine its politically expedient but irresponsible approach to encouraging higher levels of homeownership based on imprudently small down payments and too little emphasis on borrowers creditworthiness and ability to repay their loans."

PRIOR TO DEREGULATION --September 1999-- New York Times

"With pressure from the Clinton administration, Fannie Mae eased credit requirements on loans it would purchase from lenders, making it easier for banks to lend to borrowers unqualified for conventional loans. Fannie Mae's Raines explained that "there remain too many borrowers whose credit is just a notch below what our underwriting has required who have been relegated to paying significantly higher mortgage rates in the so-called subprime market."

With this action, Fannie Mae put itself at substantial risk in the event of an economic downturn. "From the perspective of many people, including me, this is another thrift industry growing up around us," warned Peter Wallison, a fellow in financial policy studies at the American Enterprise Institute (AEI). "If they fail, the government will have to step up and bail them out the way it stepped up and bailed out the thrift industry." The danger was known.

See Housing price chart. The prices shot up in 1997 due to CRA enforcement. That was 2 years prior to deregulation. Deregulation allowed these already ticking time bomb risky CRA assets to be sold to other countries & banks causing the contagion to spread world wide. Deregulation was not the prime cause it just added fuel to the fire.

GSE Conservatorship "In 2008, Fannie and Freddie have purchased about 80% of all new home mortgages in the United States."

The bailout for Fannie & Freddie was larger than all the other banks combined. The other banks have paid back nearly all the tarp funds while Fannie & Freddie continue to require more tax payer funds. They will not be paying us back!

MajikMyst

Honorary Non-member

Hmmmm..

Let's see..

Under Bill Clinton our nation had the most prosperous 8 years of our history..

Under Shrub, our nation had the worst 8 economic years of our nations history..

Clinton left a surplus and Bush left a MAMMOTH deficit..

Thems the facts, case closed!!

Now when are you repukes going to just learn to live with the reality that you suck when it comes to the economy.. Our economy historically is always better under a liberal.. Feel free to check the historical numbers..

Reagan did nothing for our economy but grow the deficit and the government.. History proves that..

As for Kissmy?? He needs to check his facts a bit more.. This melt down started under Reagan when the deregulation begain..

Why do you repukes always try to rewrite history??

Let's see..

Under Bill Clinton our nation had the most prosperous 8 years of our history..

Under Shrub, our nation had the worst 8 economic years of our nations history..

Clinton left a surplus and Bush left a MAMMOTH deficit..

Thems the facts, case closed!!

Now when are you repukes going to just learn to live with the reality that you suck when it comes to the economy.. Our economy historically is always better under a liberal.. Feel free to check the historical numbers..

Reagan did nothing for our economy but grow the deficit and the government.. History proves that..

As for Kissmy?? He needs to check his facts a bit more.. This melt down started under Reagan when the deregulation begain..

Why do you repukes always try to rewrite history??

Hmmmm..

Let's see..

Under Bill Clinton our nation had the most prosperous 8 years of our history.. Under Shrub, our nation had the worst 8 economic years of our nations history.. Clinton left a surplus and Bush left a MAMMOTH deficit..

Thems the facts, case closed!!

Now when are you repukes going to just learn to live with the reality that you suck when it comes to the economy.. Our economy historically is always better under a liberal.. Feel free to check the historical numbers..

Reagan did nothing for our economy but grow the deficit and the government.. History proves that..

As for Kissmy?? He needs to check his facts a bit more.. This melt down started under Reagan when the deregulation begain..

Why do you repukes always try to rewrite history??

You can't even lie well.

You have no idea what your talking about. Tell everyone just what exactly did Clinton do to have such a prosperous economy? Truth be known, it was fuzzy math that Clinton did to have a surplus with the deficit, so don't go thumping your chest over that one.

The economy was doing pretty well under shrub, until the democrats took over the Congress and the Senate...but don't let those facts get in the way of your story. I have no idea how you come up with the entire 8 years of his tenure. Remember that it was both parties that got the lending institutions in trouble, and shrub tried to warn them about the problem, but fell on deaf ears.

Why do whacked out wingnuts like yourself try and rewrite history, I'll never know

Misty

Gold Member

- Aug 11, 2009

- 7,137

- 1,970

- 245

Rebuffed by Fact Check and the Daily Show?!?!??

My cup runneth under.

The sad truth is; from huffington, "Well, in a result that he will probably accept as downright apocalyptic for America, The Daily Show's Jon Stewart has been selected, in an online poll conducted by Time Magazine, as America's Most Trusted Newscaster,".

drsmith1072

Senior Member

- Jul 30, 2009

- 6,031

- 250

- 48

Much of the first 35% of this post comes from The American Thinker artical: "Why the Mortgage Crisis Happened" The research & add ins are all mine. Much of the last 30% came from a Whitehouse.gov web page that disapeared the first day Obama took office.

--1991-- ACORN interfered with a House Banking Committee meeting for two days protesting a move to bring CRA reform. "According to the Times, "the same study showed no evidence that nonwhite mortgage applicants were being discriminated against."

--1992-- Enforcement of CRA was "sporadic," as the Washington Times notes, until a Federal Reserve Bank of Boston study asserted that there were "substantially higher denial rates for black and Hispanic applicants than for white applicants."

Lynn Browne was approached by co-author Alicia Munnell to do the study because "community activists were complaining that mortgage loans were not being made in minority communities." According to the Times, however, "the study had mishandled statistics on minority default rates. When the errors were accounted for, the same study showed no evidence that nonwhite mortgage applicants were being discriminated against."

Frank Quaratiello, writing in the Boston Herald, cites Stan Liebowitz: "My guess is that they were interested in finding a particular result." Said Liebowitz, "Richard Syron was head of the Boston Fed at the time. He went on to be the head of Freddie Mac. They were looking for mortgage discrimination, and they found it." According to Quaratiello, Syron became Freddie Mac CEO and chairman in 2003 and "faced increasing pressure to buy up more and more risky mortgages, some of which the Boston Fed's guide had, in effect, served to legitimize." Regarding Syron's total compensation in 2007 of $18.3 million, Liebowitz reportedly quipped, "Nice reward for presiding over unprofessional research behavior, bankrupting Freddie Mac and crippling our financial system, all in the name of politically correct lending."

--September 1992-- The Chicago Tribune described the ACORN agenda as "affirmative action lending." And writes Stanley Kurtz, senior fellow with the Ethics and Public Policy Center in Washington, "ACORN was issuing fact sheets bragging about relaxations of credit standards that it had won on behalf of minorities."

--October 1992-- Congress, enacting the Federal Housing Enterprises Financial Safety and Soundness Act of 1992, It "established HUD-imposed housing goals for financing of affordable housing and housing in central cities and other rural and underserved areas." Rep. Jim Leach, R-Iowa, warned about the impending danger non-regulated GSEs posed. According to the Washington Post, he was concerned that Congress was "hamstringing" the regulator. The complaint was that OFHEO was a "weak regulator." Leach worried that Fannie Mae and Freddie Mac were changing "from being agencies of the public at large to money machines for the stockholding few." Democrat Barney Frank, countered that "the companies served a public purpose. They were in the business of lowering the price of mortgage loans."

--September 1993-- The Chicago Sun-Times reports an initiative led by ACORN's Talbott with five area lenders "participating in a $55 million national pilot program with affordable-housing group ACORN to make mortgages for low- and moderate-income people with troubled credit histories." Kurtz notes that the initiative included two of her former targets, Bell Federal Savings and Avondale Federal Savings, who had apparently capitulated under pressure.

--July 1994-- Represented by Obama and others, plaintiffs filed a class-action lawsuit alleging Citibank had "intentionally discriminated against the plaintiffs on the basis of race with respect to a credit transaction" and calling its action "racial discrimination and discriminatory redlining practices." Buycks-Roberson v. Citibank

--November 1994-- President Clinton addresses the housing issue: "I think we all agree that more Americans should own their own homes, for reasons that are economic and tangible and reasons that are emotional and intangible but go to the heart of what it means to harbor, to nourish, to expand the American dream"..."I am determined to see that you have the opportunity and together we can make that opportunity for the young families of our country. I am committed to a new and unprecedented partnership between industry leaders and community leaders and government to recommit our nation to the idea of homeownership and to create more homeowners than ever before." "The Clinton administration announced the bold new homeownership strategy, which included monumental loosening of credit standards and imposition of subprime lending quotas."

--May 1995-- The FDIC's Board of Directors approved a final rule implementing the Community Reinvestment Act (CRA). The Comptroller of the Currency, the Board of Governors of the Federal Reserve System, and the Office of Thrift Supervision have approved parallel regulations for the institutions they supervise. The joint final rule largely retains the principles and structure of the proposals issued in December 1993 and October 1994. The new CRA regulation replaces the 12 assessment factors contained in the old rule with a more performance-based evaluation process to assess whether financial institutions are meeting the credit needs of their communities, including low- and moderate-income neighborhoods. The new rule establishes different tests for large and small institutions, as well as for retail and wholesale or limited purpose banks.

--June 1995-- Republicans had won control of Congress and planned CRA reforms. The Clinton administration, however, allied with Rep. Frank, Sen. Ted Kennedy, D-Mass., and Rep. Maxine Waters, D-Calif., did an end-around by directing HUD Secretary Andrew Cuomo to inject GSEs into the subprime mortgage market. As Kurtz notes, "ACORN had come to Congress not only to protect the CRA from GOP reforms but also to expand the reach of quota-based lending to Fannie, Freddie and beyond." What resulted was the broadening of the "acceptability of risky subprime loans throughout the financial system, thus precipitating our current crisis."

The administration announced the bold new homeownership strategy, which included monumental loosening of credit standards and imposition of "SUBPRIME LENDING QUOTAS." HUD reported that President Clinton had committed "to increasing the homeownership rate to 67.5% by the year 2000." The plan was "to reduce the financial, information and systemic barriers to homeownership" which was "amplified by local partnerships at work in over 100 cities."

Kurtz concludes, "Urged on by ACORN, congressional Democrats and the Clinton administration helped push tolerance for high-risk loans through every sector of the banking system far beyond the sort of banks originally subject to the CRA. So it was the efforts of ACORN and its Democratic allies that first spread the subprime virus from the CRA to Fannie and Freddie and thence to the entire financial system. Soon, Democratic politicians and regulators actually began to take pride in "LOWERED CREDIT STANDARDS" as a sign of "fairness" and the contagion spread. Attorney General Janet Reno, who had already won a number of bank lending discrimination settlements, sternly announces, "We will tackle lending discrimination wherever it appears." With the new policy in full force, "No loan is exempt; no bank is immune. For those who thumb their nose at us, I promise vigorous enforcement."

--1997-- HUD Secretary Cuomo said, "GSE presence in the subprime market could be of significant benefit to lower-income families, minorities, and families living in underserved areas. "

--1998-- By falsifying signatures on Fannie Mae accounting transactions, $200 million in expenses was shifted from 1998 to later periods, thereby triggering $27.1 million in bonuses for top executives. James A. Johnson received $1.932 million; Franklin D. Raines received $1.11 million; Lawrence M. Small received $1.108 million; Jamie S. Gorelick received $779,625; Timothy Howard received $493,750; Robert J. Levin received $493,750.

--April 1998-- HUD announced a $2.1 billion settlement with AccuBanc Mortgage Corp. for alleged discrimination against minority loan applicants. Affirmative Action Lending The funds would provide poor families with down payments and low interest mortgages. "Discrimination isn't always that obvious," said Secretary Cuomo in announcing the AccuBanc deal. "Sometimes more subtle but in many ways more insidious, an institutionalized discrimination that's hidden behind a smiling face." Before the camera, Cuomo admitted the mandate amounted to "affirmative action" lending that would result in a "higher default rate."

The institution would "take a greater risk on these mortgages, yes; to give families mortgages who they would not have given otherwise, yes; they would not have qualified but for this affirmative action on the part of the bank, yes. It is by income, and is it also by minorities? Yes. "With the $2.1 billion, lending that amount in mortgages which will be a higher risk, and I'm sure there will be a higher default rate on those mortgages than on the rest of the portfolio." The CRA allowed ACORN "organizations to collect a fee from the banks for their services in marketing the loans. The Senate Banking Committee had estimated that, as a result of CRA, $9.5 billion had gone to pay for services and salaries of the organizers."

--May 1999-- The Los Angeles Times reports that African-American homeownership is increasing three times as fast as that of whites, with Latino homeowners growing five times as fast, attributing the growth to breathing "the first real life into enforcement of the Community Reinvestment Act." Mandateing that Fannie Mae and Freddie Mac buy mortgages with deviant down payments and debt-to-income ratios, which allowed lenders to approve mortgages for lower-income families that would have been denied otherwise. By now, all pretense had disappeared and lending practices were based upon concerns of discrimination in the banking system regardless of the consequences. Clinton threatened to veto a bill passed by the Senate that had "shortsightedly voted to retrench" CRA, as the Times put it. Under pressure, Fannie Mae was resisting increased targeting, arguing that the result would be more loan defaults. Barry Zigas, head of Fannie Mae's low-income efforts, argued, "There is obviously a limit beyond which (we) can't push (the banks) to produce," the Times reported.

--Fall 1999-- Treasury Secretary Lawrence Summers issued a warning: "Debates about systemic risk should also now include government-sponsored enterprises, which are large and growing rapidly."

--September 1999-- New York Times "With pressure from the Clinton administration, Fannie Mae eased credit requirements on loans it would purchase from lenders, making it easier for banks to lend to borrowers unqualified for conventional loans. Fannie Mae's Raines explained that "there remain too many borrowers whose credit is just a notch below what our underwriting has required who have been relegated to paying significantly higher mortgage rates in the so-called subprime market."

With this action, Fannie Mae put itself at substantial risk in the event of an economic downturn. "From the perspective of many people, including me, this is another thrift industry growing up around us," warned Peter Wallison, a fellow in financial policy studies at the American Enterprise Institute (AEI). "If they fail, the government will have to step up and bail them out the way it stepped up and bailed out the thrift industry." The danger was known.

A study by Freddie Mac, confirming earlier Federal Reserve and FDIC studies, contradicts race discrimination arguments for CRA. The study found that African-Americans with annual incomes of $65,000-$75,000 have on average worse credit records than whites making under $25,000. This showed that the difficulty in qualifying was not because of race but bad credit records. Accordingly, the Federal Reserve Bank of Dallas entitled a paper "Red Lining or Red Herring?"

"City Journal warned that the Clinton administration had turned CRA into 'a vast extortion scheme against the nation's banks,'committing $1 trillion for mortgages and development projects, most of it funneled through the community organizers."

--November 1999-- President Bill Clinton signed into law S.900 Financial Services Modernization Act of 1999 This bill had CRA loan mandates & allowed banks to sell the mandated bad loans to GSEs Fannie, Freddie, pension funds, foreigners & anyone else. This made it legal for banks to create bad risky loans with the government backing it allowing it to get a AAA rating.This gave banks a license to steal!!!

--December 2000-- President Bill Clinton signed into law H.R. 4577: Consolidated Appropriations Act, 2001. Consolidated in this bill was Commodity Futures Modernization Act of 2000. This law made most over-the-counter derivatives (OTC derivatives) transactions between sophisticated parties un-regulated as futures under the Commodity Exchange Act (CEA) or as securities under the federal securities laws. Instead, banks and securities firms would continue to have their dealings in OTC derivatives supervised by their federal regulators under general safety and soundness standards. Functional regulation. This was to create an international derivatives market for comodities securities. Clinton & Gore were trying to built the framework for Carbon Cap & Trade Energy Trading Market Scheme with this law. This gave birth to the Enron Loophole.Gore and the Enron Loophole.

--April 2001-- The Bush Administration's FY02 budget declares that the size of Fannie Mae and Freddie Mac is "a potential problem," because "financial trouble of a large GSE could cause strong repercussions in financial markets, affecting Federally insured entities and economic activity."

--May 2002-- President Bush calls for the disclosure and corporate governance principles contained in his 10-point plan for corporate responsibility to apply to Fannie Mae and Freddie Mac. (OMB Prompt Letter to OFHEO, 5/29/02)

--September 2003-- Treasury Secretary John Snow testifies before the House Financial Services Committee to recommend that Congress enact "legislation to create a new Federal agency to regulate and supervise the financial activities of our housing-related government sponsored enterprises" and set prudent and appropriate minimum capital adequacy requirements.

The New York Times published on Sept 10th 2003 "The Bush administration today recommended the most significant regulatory overhaul in the housing finance industry since the savings and loan crisis a decade ago. Under the plan, disclosed at a Congressional hearing today, a new agency would be created within the Treasury Department to assume supervision of Fannie Mae and Freddie Mac, the government-sponsored companies that are the two largest players in the mortgage lending industry. The new agency would have the authority, which now rests with Congress, to set one of the two capital-reserve requirements for the companies. It would exercise authority over any new lines of business. And it would determine whether the two are adequately managing the risks of their ballooning portfolios."

--November 2003-- Council of the Economic Advisers (CEA) Chairman Greg Mankiw explains that any "legislation to reform GSE regulation should empower the new regulator with sufficient strength and credibility to reduce systemic risk." To reduce the potential for systemic instability, the regulator would have "broad authority to set both risk-based and minimum capital standards" and "receivership powers necessary to wind down the affairs of a troubled GSE." (N. Gregory Mankiw, Remarks At The Conference Of State Bank Supervisors State Banking Summit And Leadership, 11/6/03)

--February 2004-- The President's FY05 Budget again highlights the risk posed by the explosive growth of the GSEs and their low levels of required capital, and called for creation of a new, world-class regulator: "The Administration has determined that the safety and soundness regulators of the housing GSEs lack sufficient power and stature to meet their responsibilities, and therefore should be replaced with a new strengthened regulator." (2005 Budget Analytic Perspectives, pg. 83)

--February 2004-- CEA Chairman Mankiw cautions Congress to "not take [the financial market's] strength for granted." Again, the call from the Administration was to reduce this risk by "ensuring that the housing GSEs are overseen by an effective regulator." (N. Gregory Mankiw, Op-Ed, "Keeping Fannie And Freddie's House In Order," Financial Times, 2/24/04)

--June 2004-- Deputy Secretary of Treasury Samuel Bodman spotlights the risk posed by the GSEs and called for reform, saying "We do not have a world-class system of supervision of the housing government sponsored enterprises (GSEs), even though the importance of the housing financial system that the GSEs serve demands the best in supervision to ensure the long-term vitality of that system. Therefore, the Administration has called for a new, first class, regulatory supervisor for the three housing GSEs: Fannie Mae, Freddie Mac, and the Federal Home Loan Banking System." (Samuel Bodman, House Financial Services Subcommittee on Oversight and Investigations Testimony, 6/16/04)

--Late 2004-- Democrats in congress blocked action to regulate the GSEs Fannie & Freddie.

These same Democrats & Obama were paid off by by GSEs Fannie & Freddie!!!

--December 2004-- ACORN used congress to force Trillions in CRA loans & payoffs. They recently hit Bank of America for over $800 billion. (see page 25) of this congress hearing. That is some serious money. Don't tell me ACORN is not pouring on some serious pressure using the CRA compliance criteria.

--2005-- Fannie Mae CEO Frank Raines affirms partnership with Barack Obama & The Congressional Black Caucus" Frank Raines

--April 2005-- Treasury Secretary John Snow repeats his call for GSE reform, saying "Events that have transpired since I testified before this Committee in 2003 reinforce concerns over the systemic risks posed by the GSEs and further highlight the need for real GSE reform to ensure that our housing finance system remains a strong and vibrant source of funding for expanding homeownership opportunities in America Half-measures will only exacerbate the risks to our financial system." (Secretary John W. Snow, "Testimony Before The U.S. House Financial Services Committee," 4/13/05)

--August 2007-- President Bush emphatically calls on Congress to pass a reform package for Fannie Mae and Freddie Mac, saying "first things first when it comes to those two institutions. Congress needs to get them reformed, get them streamlined, get them focused, and then I will consider other options." (President George W. Bush, Press Conference, The White House, 8/9/07)

--September 2007-- Obama - "Subprime lending started off as a good idea - helping Americans buy homes who couldnt previously afford to. Financial institutions created new financial instruments that could securitize these loans, slice them into finer and finer risk categories and spread them out among investors around the country and around the world. In theory, this should have allowed mortgage lending to be less risky and more diversified." Top Contributors to Barack Obama's Campaign

--December 2007-- President Bush again warns Congress of the need to pass legislation reforming GSEs, saying "These institutions provide liquidity in the mortgage market that benefits millions of homeowners, and it is vital they operate safely and operate soundly. So I've called on Congress to pass legislation that strengthens independent regulation of the GSEs and ensures they focus on their important housing mission. The GSE reform bill passed by the House earlier this year is a good start. But the Senate has not acted. And the United States Senate needs to pass this legislation soon." (President George W. Bush, Discusses Housing, The White House, 12/6/07)

--February 2008-- Assistant Secretary David Nason reiterates the urgency of reforms, says "A new regulatory structure for the housing GSEs is essential if these entities are to continue to perform their public mission successfully." (David Nason, Testimony On Reforming GSE Regulation, Senate Committee On Banking, Housing And Urban Affairs, 2/7/08)

--March 2008-- President Bush calls on Congress to take action and "move forward with reforms on Fannie Mae and Freddie Mac. They need to continue to modernize the FHA, as well as allow State housing agencies to issue tax-free bonds to homeowners to refinance their mortgages." (President George W. Bush, Remarks To The Economic Club Of New York, New York, NY, 3/14/08)

--April 2008-- President Bush urges Congress to pass the much needed legislation and "modernize Fannie Mae and Freddie Mac. [There are] constructive things Congress can do that will encourage the housing market to correct quickly by helping people stay in their homes." (President George W. Bush, Meeting With Cabinet, the White House, 4/14/08)

--May 2008-- President Bush issues several pleas to Congress to pass legislation reforming Fannie Mae and Freddie Mac before the situation deteriorates further.

--June 2008-- President once again asks Congress to take the necessary measures to address this challenge, saying "we need to pass legislation to reform Fannie Mae and Freddie Mac." (President George W. Bush, Remarks At Swearing In Ceremony For Secretary Of Housing And Urban Development, Washington, D.C., 6/6/08)

In 2008, Fannie and Freddie have purchased about 80% of all new home mortgages in the United States. Their combined investment portfolios held mortgage assets (loans and MBSs) valued at $1.5 trillion (as of June 30, 2008) - These GSE will never pay back tax payer for losses like all the banks have.

--April 2009-- Obama on his world appology tour in Strasbourg, France "difficult to imagine that the inability of somebody to pay for a house in Florida could contribute to the failure of the banking system in Iceland. Today what's difficult to imagine is that we did not act sooner to shape our future."

--JULY 2009-- Committee on Oversight and Government Reform released a report on "The Role of Government Affordable Housing Policy in Creating the Global Financial Crisis of 2008"

LOL where to begin with the dishoenst drivel??

Let's start with from 1993 to 2007 the congress was controlled by republicans with the exception of 2 years from 2001 to 2003 after jeffords switched to independent to give control of the senate to the dems. So how is all of that legislation proposed and passed by a republican controlled congress supposed to be the fault of the democrats??

Your cut and paste mentions HR 4577 and tries to blame clinton because he signed it into law but did you happen to know who proposed that legislation?? Rep, John Porter [R-IL]

The vote in the house was 292-60 with 80 representatives not voting more dems did vote in favor of it. However, the vote in the senate was 52-43 with 5 not voting with 44 republicans voting yea and only 10 republicans senators voting nay.

Oh and I just love how you include that spliced together youtube video from 2004 with the dishonest title "democrats in congress blocked action to regulate GSEs fannie and freddie" when the FACT is that THE REPUBLICANS CONTROLLED CONGRESS AND THE AGENDA and still they CHOSE to do NOTHING about what they called a threat.

So how is the ineptitude of the right the fault of the dems??

I believe that the republicans even had a bill that was co-sponsored by mccain that made it out of committee. However, the republicans CHOSE not to send the bill to the floor for a vote.

How could dems block something that passed the committee but was never put on the floor for a debate or a vote by the majority republicans??

Toro

Diamond Member

This should be in the humor section.

drsmith1072

Senior Member

- Jul 30, 2009

- 6,031

- 250

- 48

Great work.

I am aware of the long list of conspirators - but you put it all together very very well.

While Republicans, and a hungry for easy profits Wall St. certainly share in some of the blame, the warnings were in fact being issued from the Republican side and all but ignored by Democrats, whose easy-lending policies initiated what later became the subprime crisis.

And yet, the media has repeatedly failed to follow up on this.

Make no mistake, if the roles were reversed, and it was Republicans who had passed easy credit race based legislation, and ignored all the warnings, the Democrats would now be undergoing repeated Congressional hearings on the whole sordid affair.

As it is, these same Democrats who built the mess, now point the finger at all but themselves...

LOL yeah the republcians side "warned" and did nothing despite the FACT that they controlled both houses of congress and therefore controlled the agenda.

In case you missed it the only two bills mentioned in that long rant, HR4577 and S.900, were both sponsored by REPUBLICANS and passed by republican contolled sentate and house.

See previous post for info on HR4577

S.900 was sponsored by REPUBLICAN Phil Gramm and passed the REPUBLICAN controlled senate 90-8 and then passed the REPUBLICAN controlled house 362-57.

Republicans DID pass this legislation and the democrats are NOT the ones trying to make a huge deal out of this. It was the republicans who passed the legislation and they are now trying to blame the democrats for it. LOL

Soggy in NOLA

Diamond Member

- Jul 31, 2009

- 40,565

- 5,361

- 1,830

Nah, it's all Sarah Palin's fault... didn't you hear?

Soggy in NOLA

Diamond Member

- Jul 31, 2009

- 40,565

- 5,361

- 1,830

Hmmmm..

Let's see..

Under Bill Clinton our nation had the most prosperous 8 years of our history..

Under Shrub, our nation had the worst 8 economic years of our nations history..

Clinton left a surplus and Bush left a MAMMOTH deficit..

Thems the facts, case closed!!

Now when are you repukes going to just learn to live with the reality that you suck when it comes to the economy.. Our economy historically is always better under a liberal.. Feel free to check the historical numbers..

Reagan did nothing for our economy but grow the deficit and the government.. History proves that..

As for Kissmy?? He needs to check his facts a bit more.. This melt down started under Reagan when the deregulation begain..

Why do you repukes always try to rewrite history??

To each Point:

The Clinton years were NOT the most prosperous in U.S. history.

8 years under Bush were NOT the worst in history... where the **** do you even get this shit from?

Clinton did not leave a surplus, he transferred the deficits from public borrowings to intergovernmental borrowings. (like saying, I made $50k, I spent $80k, but since I took the other $30k from my 401k and didn't run up debt, I ran a surplus)

Reagan did NOTHING for the economy? How idiotic. History proves you an ignoramous or just plain STUPID.

Educate yourself you imbecile.

drsmith1072

Senior Member

- Jul 30, 2009

- 6,031

- 250

- 48

DevNell said:

Greenspan Admits Errors to Hostile House Panel - WSJ.com

Lawmakers read back quotations from recent years in which Mr. Greenspan said there's "no evidence" home prices would collapse and "the worst may well be over."

The 82-year-old Mr. Greenspan said he made "a mistake" in his hands-off regulatory philosophy, which many now blame in part for sparking the global economic troubles. He quoted something he had written in March: "Those of us who have looked to the self-interest of lending institutions to protect shareholder's equity (myself especially) are in a state of shocked disbelief."

He conceded that he has "found a flaw" in his ideology and said he was "distressed by that." Yet Mr. Greenspan maintained that no regulator was smart enough to foresee the "once-in-a-century credit tsunami."

Greenspan, dems & repubs alike did make mistakes, but even Greenspan recognized them before it was to late.

On February 17th 2005 Alan Greenspan testified before congress saying "Enabling these institutions to increase in size...and they will once the crisis in their judgment passes...we are placing the total financial system of the future at a substantial risk."

Congress did not listen to Greenspan, Bush, Snow or other experts. It is almost as if democrats took this opportunity to let the financial system run off the tracks creating a disastrous train wreck to sweep the republicans from power. It was so obvious that the tracks were broken & the train was roaring towards them. Yet when someone tried to fix them democrats said we don't have a problem with the tracks, we don't here a train coming.CRASH - OMG it was all the repubs fault, elect me & I will fix it. [ame="http://www.youtube.com/watch?v=_MGT_cSi7Rs&feature=related"]See no evil, Here no evil[/ame]

Of course democrats have long dreamed of destroying the financial system in order to bring in socialism. Their plan has worked like a dream. Politicians are scumbags!!!

UH you do know who was in charge of congress from jan 2003 to to jan 2007 don't you??

I have to ask because it seems that you do not know that REPUBLICANS controlled congress during that time and therefore REPUBLICANS controlled the agenda. Republcians chose to do NOTHING and for the republican ineptitude you try to blame the democrats. LOL

The republicans couldn't have passed anything without the help of the democrats. That's the bottom line. It's both parties, and they both have been equal in the problems that we are facing today.

drsmith1072

Senior Member

- Jul 30, 2009

- 6,031

- 250

- 48

Wow, so you fuckers are still trying to blame bill the most because he signed something , go figure, pathetic

even by your own biased list it would be really hard to figure this fiasco out and don't try and tell me you are that ******* smart , because you aren't

The sad thing is that aren't these the same morons that piss and moan everytime obama points back to W and his "mistakes?" However, it's ok for them to try to blame clinton and the dems as they ignroe the FACT that W was president for 8 years and republicans controlled both houses of congress for SIX of those eight years. LOL

drsmith1072

Senior Member

- Jul 30, 2009

- 6,031

- 250

- 48

In the final analysis, it really wasn't "caused" by any politician, but by the lawyer-lobbyists and Wall Street financial wizards who saw through existing regulations and took advantage of loopholes that fed the American Dream and all the pigs at the trough (that's everyone, folks) eager to grab a share and dumb enough to believe that the trough would always be full. (And tax free to boot!)

I disagree because I believe derivatives should be illegal. They allow one person to have way more power & leverage over many others & screw up more lives than just their own with risk taking. This is clearly not a principal of the free market. They are financial WMDs & create far more problems than they solve. In the final analysis, this crisis was caused by politicians on both sides, but when problems started to appear democrats dug in the most to protect the scheme that they believed was getting more money to their people & were blinded by racism, greed & power.

Yes the lawyer-lobbyists and Wall Street financial wizards who saw through existing regulations and took advantage of loopholes that fed the American Dream and all the pigs at the trough (that's everyone, folks) eager to grab a share and dumb enough to believe that the trough would always be full. (And tax free to boot!)

The reason we have laws is even though most people will pass on a get rich quick scheme is it is unethical yet legal. A few will not resist & do major damage. If you leave a stack of money laying around in public someone is going to take it. Not only did some of the politician's blatantly refuse stop this when they had a chance, but they lined up at the trough & took their cut. To make matters even worse they feed at the GSE trough paid for by taxpayers.

You built up all the facts and stopped short of naming names. Do you know who took the most money from GSEs? Obama

Do you know who else got huge amounts of money from GSEs? Barney Frank

Do you know who blocked all GOP attempts to regulate GSEs? Obama & Barney Frank

I want derivatives stopped, and only investments that create capital & jobs allowed. No short-selling, no options, no more financial casino. No more "capturing" of government agencies like the SEC by Wall Street companies. How can someone like Bernie Madoff brag about becoming the next SEC head, and almost buy his way in?

How did obama block legislation in the US Senate BEFORE he was a US senator??

Back in 2004 there was a bill that made it out of a the republican controlled committee but when no furhter because REPUBLICANS CHOSE TO DO NOTHING and you claim that obama "blocked ALL GOP attempts to regulate the GSEs." Sorry but that is a flat out LIE.

Fact is that REPUBLICANS had control of both houses of congress from jan 2003 to jan 2007 and they CHOSE to do NOTHING about it. No legislation was put on the floor for a debate or a vote during that time so how was something that was never put on the floor, in a congress whose agenda was controlled by REPUBLICANS, blocked by the dems??

Now, all of the lemmings are jumping on this bandwagon and trying to blame the democrats all because the republicans CHOSE to do NOTHING when they had the chance. LOL

Wicked Jester

Libsmackin'chef

These dem apologists are just too damn funny.

We'll just see how apologetic these kool-aid drinking lil' weasels are come november when we steamroll their hero's straight out of the house and senate!

New Jersey, Virginia Massachussets. Yep, the steamrollers headed to a state near you real soon!

Best get outta the way, lib's!

We'll just see how apologetic these kool-aid drinking lil' weasels are come november when we steamroll their hero's straight out of the house and senate!

New Jersey, Virginia Massachussets. Yep, the steamrollers headed to a state near you real soon!

Best get outta the way, lib's!

drsmith1072

Senior Member

- Jul 30, 2009

- 6,031

- 250

- 48

Let me get this straight...This legislation, which is responsible for re-legalizing derivatives, was crafted, written, and voted into law by a Republican Senate and a Republican House of Representatives. Derivatives had in fact been illegal since the great depression, prior to this.

By 1999 and into 2000, thanks to that same Republican congress, Bill Clinton, as we know, was the lamest of lame ducks.

But instead of blaming the Republican Congress for this piece of shit law, instead of blaming it's primary author, Phil Gramm...

You're trying to blame Bill Clinton because he didn't veto it?

And how the hell does Al Gore fit in? Was there a tie in the Senate that he had to decide concerning this bill?

Seriously, blaming the president for legislation crafted by a Republican congress which could have easily overridden his veto?

Just another example of crazy right-wing fanatics attempting to re-write history...

A better question is: why didn't the dems undo this crap when they had an unstoppable majority? because they are whores just like the GOP

Why didn't the dems stop tax breaks for moving jobs overseas? same answer

The dems do a lot of whining and finger-pointing instead of actually fixing problems. You can't name anything that the dems did during 2009 that created jobs and made the financial system sounder. They are all addicted to K-street money.

Uh answer to question 1.

The dems only had the super majority for about 6 months. Had to wait until we got the 60th vote when al franken was confirmed in july. So how would undoing this crap AFTER the vent in question had already happened have changed anything??

Question 2. What REAL affect would that have had in the last year and would republicans have supported it or would they just continue to say NO like they have to everything else?

Response to your last statement.

Correct me if I am wrong but was this thread start by whining republicans who are engaging in finger pointing instead of actually fixing the problems?? LOL

drsmith1072

Senior Member

- Jul 30, 2009

- 6,031

- 250

- 48

The republicans couldn't have passed anything without the help of the democrats. That's the bottom line. It's both parties, and they both have been equal in the problems that we are facing today.

LOL that's the best spin you have?? LOL

Let's see, the bills in question were sponsored by republicans and then passed through republican controlled committees and then passed the republican controlled congress however, according to you, the republicans couldn't have done it without the dems. LOL

It's funny how republicans didn't and don't feel that way when describing a congress with a democrat majority. Oh well, just the usual dishonest political expediency. LOL

Last edited:

Similar threads

- Replies

- 102

- Views

- 2K

- Replies

- 153

- Views

- 1K

- Replies

- 80

- Views

- 2K

- Replies

- 3

- Views

- 153

New Topics

-

Violent riot breaks out in Belfast after sudanese man tries to behead irish man

Violent riot breaks out in Belfast after sudanese man tries to behead irish man- Started by Mortimer

- Replies: 0

-

-

Are the White House Ring Girls violating the flag code with their outfits?

Are the White House Ring Girls violating the flag code with their outfits?- Started by airplanemechanic

- Replies: 0

-

-