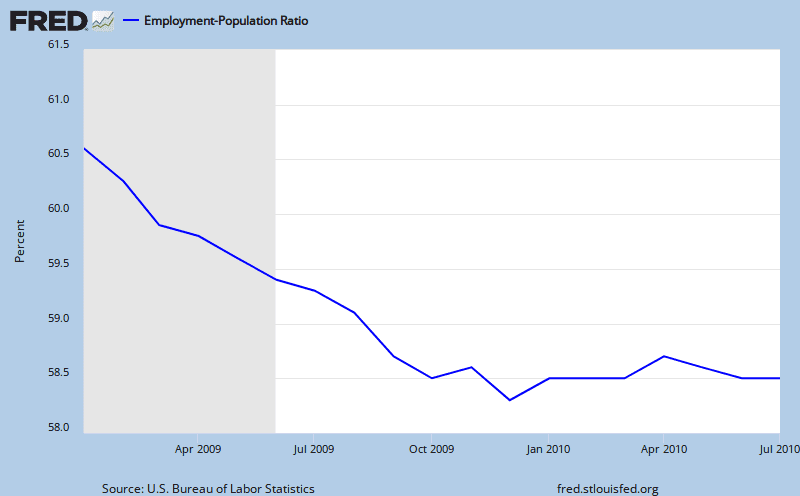

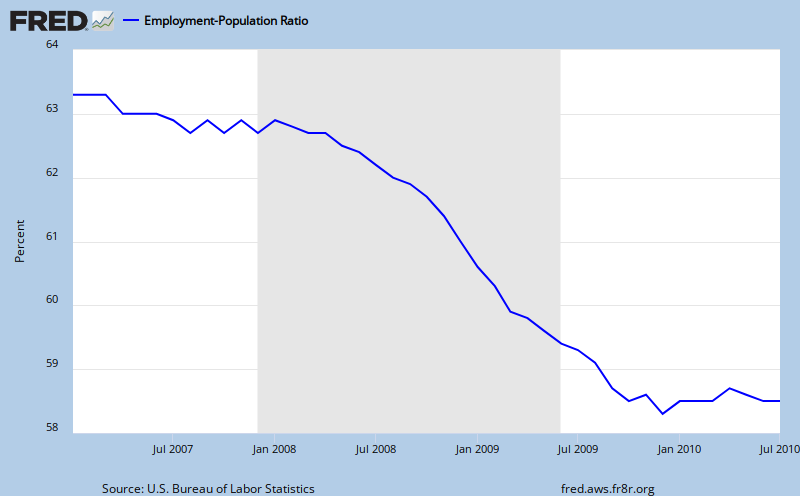

WOW... Did kiss my declare that it was both sides fault? All I can say is...HACK.

WHAT litany of points??? The first point is a DEAD link that has no article attached to it.

--1991-- ACORN interfered with a House Banking Committee meeting for two days protesting a move to bring CRA reform.

Irony...if people had listened to ACORN, maybe the foreclosure crisis would have been averted...

Acorn Led Financial Sector With Warnings on Lending

The national advocacy group appears to deserve recognition for its prudent -- and ignored -- early advice about home loan practices.

In fact according to a string of 1999 and 2000 reports in American Banker, a 173-year-old publication calling itself "the leading information resource serving the banking and financial services community" ACORN was an outspoken, consistent advocate for exactly the kinds of regulations that experts across the political spectrum now agree could have prevented the global economic crisis.

On August 4, 2000, American Banker reported on ACORN protests at nationwide offices of Lehman Brothers the investment bank that went bankrupt last month because of its investment in over-valued mortgage-backed securities:

"Acorn members said they want Lehman and other investment banks to sign a code of ethics, pledging to adhere to 'best practices' in the mortgage lending business. Though the banks are not lenders, the group argues that they provide capital and financial support to abusive lenders by buying and securitizing their loans.

'They have to look at the terms of the loans they are funding and say they won't buy or securitize loans with unconscionable terms,' said Bertha Lewis, executive director of Acorn in New York. 'These secondary market players can see what kind of loans these are. They must refuse to buy loans from predatory lenders.'"

ACORN's campaign to get investment banks to adopt best practices for the mortgages they bought was aimed at drying up the secondary market for the toxic mortgages now at the bottom of the fallen financial house of cards. If investment banks didn't buy the shady loans, predatory lenders wouldn't receive the capital to make such loans, ACORN reasoned.

Acorn Led Financial Sector With Warnings on Lending - City Limits Magazine - CityLimits.org

ACORN to Protest Predatory Lending at Wells Fargo Annual Meeting

Publication: Business Wire

Date: Thursday, April 22 2004

Business Editors

WASHINGTON--(BUSINESS WIRE)--April 22, 2004

More than 125 ACORN members will demonstrate at Wells Fargo's annual meeting on April 27 to protest the company's predatory lending practices. Members will travel to Wells' San Francisco headquarters to confront Wells' top managers about abusive mortgage loans.

ACORN to Protest Predatory Lending at Wells Fargo Annual Meeting; ACORN Members Will Also Speak at Meeting in Support of Anti-Predatory Lending Resolution. | Trends & Events > Talks & Meetings from AllBusiness.com

Poor People Protest predatory lending practices by Wells Fargo

WASHINGTON - The racially discriminatory, predatory lending practices of Wells Fargo, along with President George Bushs Social Security Privatization plan, were targets of hundreds of ACORN members protesting in Washington March 7.

Demonstrators from Florida to Massachusetts, to Ohio, to as far away as Chicago descended on Washington, bringing with them ACORNs take-it-to-streets tactics to make known their opposition to the privatization of Social Security; to rally at the offices of major tax preparation firms which make quick tax-return loans; and to release a new report demonstrating racial discrimination and predatory lending by Wells Fargo during the groups 2005 Legislative Conference.

We have actually been doing a campaign on Wells Fargo, to improve their practices on lending for several years now, Matthew Mayers, legislative director of the Association of Community Organizations for Reform Now (ACORN), said in an interview.

A lot of ACORNs attention has been focused on predatory lending practices by banks and mortgage companies that result in low-income people, the elderly, and non-Whites being much more likely to get bad loans that take money away from them unfairly, said Mr. Mayers. Predatory lending involves charging exorbitant interest rates, failing to disclose all loan terms, and marketing to people with financial and credit problems who likely cannot repay a loan. They are loans which are doomed to fail.

In early February, about 100 ACORN demonstrators protested inside and outside the Wells Fargo Financial building in Harrisburg, the capital of Pennsylvania. The protesters occupied the lenders downtown Harrisburg office for about 20 minutes until police arrived and dispersed the crowd, according to WNEP-TV 16.

Many predatory lending victims have lost their homes, said Mr. Mayers. Theyre sort of bait and switch and people dont know the kind of loan theyre going to get and then they find out when its too late. Our new study actually shows that people of color, particularly African Americans, are much more likely to be singled out for some of these bad loans.

Were really calling on (Wells Fargo) to change their practices, he said.

In another case, after seven years of litigation by the Federal Trade Commission, the agency reached an agreement with Capital City Mortgage Corp. in late February. Capital City is a Washington-based company whose home-lending practices triggered a national assault on abusive lending. Capital City agreed it would stop making consumer loans that use a house as security and that it would disclose fees and terms on future commercial loans.

Capital City was alleged to have used fraud and deception to put minority homeowners with credit problems into loans they couldnt afford. The high fees and high-interest penalties reportedly sent many into foreclosure.

Capital City foreclosed on one in five mortgage loans made from 1984 to 1995, and on one in three made from 1989 to 1991. The national foreclosure rate has stayed around one in 100 in recent years, and the percentage of subprime loans in foreclosurethose loans made at higher cost to people with faulty creditis on the order of four in 100.

The FTC has subsequently sued 19 other companies, mostly national or regional firms, and has won millions of dollars in those cases.

Companies know they can make a lot of money by going into low-income areas and into minority areas where there may not be other options for loans, said Mr. Mayers. Years ago, the fight was about red-lining, about not getting any type of loans or credit, particularly in urban areas, inner city areas. Now its about, not the quantity of the credit, but the quality. Theyre giving loans, but a lot of them are really kind of rip-off loans.

The group can claim some successes, said Mr. Mayers. ACORN has pressured some companies to change their ways, he noted.

Probably, the most well known was Household Finance, where we did our typical ACORN tactics of taking it to the streets and mobilizing people. At the same time, the attorney-general had a suit against them and they really cleaned up their act in a lot of ways, worked to get people better loans, and a lot of people found a much more cooperative relationship with (Household Finance), he said. The other part of it is that weve really pushed for good legislation on the state level. We passed legislation in places like New York and Illinois.

Poor People Protest predatory lending practices by Wells Fargo

Like most reasonable, unbias people would admit....it was from both parties where the real estate mess developed.

September 30, 1999

"Fannie Mae Eases Credit To Aid Mortgage Lending

By STEVEN A. HOLMES

In a move that could help increase home ownership rates among minorities and low-income consumers, the Fannie Mae Corporation is easing the credit requirements on loans that it will purchase from banks and other lenders.

The action, which will begin as a pilot program involving 24 banks in 15 markets -- including the New York metropolitan region -- will encourage those banks to extend home mortgages to individuals whose credit is generally not good enough to qualify for conventional loans. Fannie Mae officials say they hope to make it a nationwide program by next spring.

Fannie Mae, the nation's biggest underwriter of home mortgages, has been under increasing pressure from the Clinton Administration to expand mortgage loans among low and moderate income people and felt pressure from stock holders to maintain its phenomenal growth in profits.

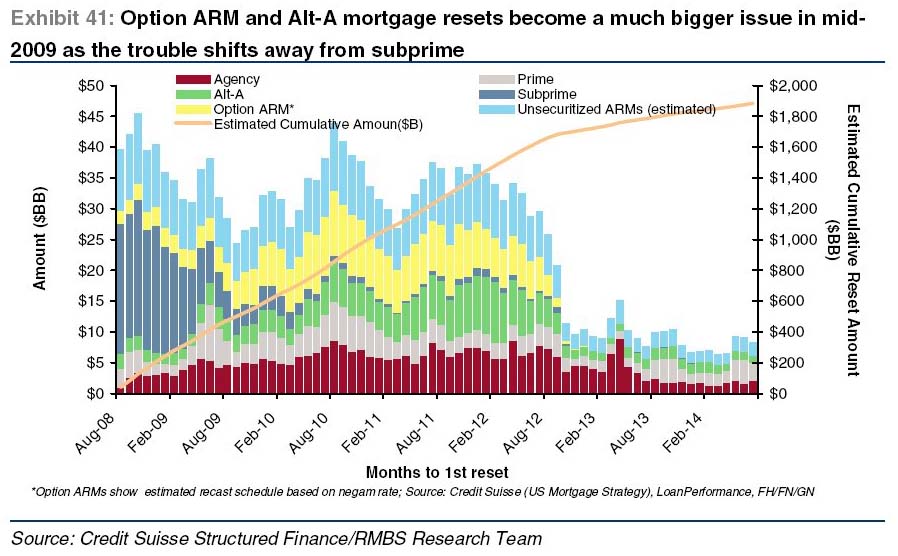

In addition, banks, thrift institutions and mortgage companies have been pressing Fannie Mae to help them make more loans to so-called subprime borrowers. These borrowers whose incomes, credit ratings and savings are not good enough to qualify for conventional loans, can only get loans from finance companies that charge much higher interest rates -- anywhere from three to four percentage points higher than conventional loans."

Fannie Mae fiasco started under Clinton's watch. | The Hive

And ACORN led the fight AGAINST subprime borrowers, predatory lending practices and WARNED people buying homes not to fall for their shady practices.

And your point is.......?