AdvancingTime

Senior Member

- Feb 8, 2015

- 150

- 20

- 46

A slew of stories and articles have hit the news recently about how companies buying back their own stock are driving the market higher. I would be amiss not to comment on this and point out the impact and importance of stock buybacks and how they add to both low volatility and at the same time support the already crazy high valuations. Decades ago stock buybacks were illegal because they were considered to be a form of stock market manipulation. They were legalized in 1982 by the SEC and since then have become a tool for companies and management to boost share prices. Buybacks have been described as "smoke and mirrors," because when a company buys back shares of their own stock they reduce the "share float" and increase earning per share.

Buybacks Have Created A Dangerous Illusion (click here)

Buybacks should be viewed as a double-edged sword with great power in that they reduce the number of shares over which earnings are divided at the same time they add to market demand. This gives the impression the companies earnings are increasing while in reality, overall earnings may be flat or even on the decline. The deregulation of buybacks years ago has returned to haunt us because it tends to create a dangerous illusion that draws less sophisticated investors into a market that is not nearly as strong as it appears. The new recently passed tax law which lowers corporate taxes and encourages repatriation of cash that has been stored overseas is feeding fuel into the share buyback frenzy.

To be perfectly clear, buybacks are a tool corporate boards and CEOs use to manipulate the prices of their own shares higher. This means insiders can get out or hedge their positions before reality sets in and prices fall back to earth. Call it a well constructed exit strategy if you like. This is where I remind you it is major investors that sit on the board or hold executive positions and the same CEOs and other top managers who have received much of their compensation over the years in stock options. Yes, these are often the shareholders in the company that have reaped the largest benefits of QE over the years and added to inequality.

Buybacks Have A Darkside And Drive Inequality

This is already causing a backlash among politicians as they learn the talk about the money corporations saved from the tax cut would flow to develop businesses. They are not building new plants, developing new products or boosting wages, it was simply a lie. Murmurs are beginning to grow in Washington this situation needs to be addressed, however, do not expect any action soon. This issue sits low on the agenda of a dysfunctional government and lawmakers that are already slammed by more pressing matters. Casting their eyes towards coming elections, however, this is an area of law Democrats will focus on during the mid-term election cycle but the fact is a Democrats would need a massive victory before a law could be passed that would end buybacks. I suspect the issue will not be addressed until long after the damage is done and investors have been raped and plundered.

Several unusual currents are running through the market right now, one of those is low volatility of which share buybacks are a major contributor. This is because buybacks are insensitive to price and simply steps in and are ready to purchase on any weakness. With this in mind. it is important to remember that much of the buyback action over the last several years prior to the Trump’s tax changes has been financed from debt raised by selling corporate bonds. This means many companies will not have the money to keep their stock flying when the market begins to fall and leveraged companies will get hammered. These most likely are not the companies with cash stockpiles overseas that can now be repatriated cheaply and to make matter worse they now face higher interest rates.

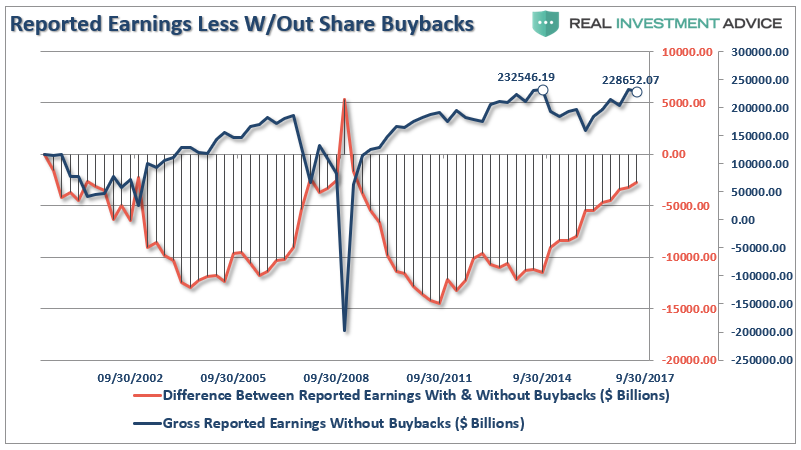

Buybacks are why we have been hearing so many analysts touting the line that stocks are not overvalued and how earnings are growing. What they are referring to is earnings per share, and what is really doing better in that fraction is the denominator. Records show U.S. firms have spent roughly $4 trillion on buybacks since 2009, this means corporations have been the biggest single source of demand for U.S. shares during the so-called recovery. It is reported by 13D Research that buybacks have “accounted for more than 40% of the total earnings-per-share growth since 2009, and an astounding +72% of the earnings growth since 2012. Simply put, many corporate boards have made the decision to drain the company coffers in order to buy back shares, often from themselves and sometimes even in special deals offered only to themselves off the general market.

This is why according to an IMF estimate from last spring that large U.S. corporations have experienced a negative net equity issuance of $3 trillion since 2009. Linked to these share buybacks we have seen U.S. corporate debt to soar to an all-time high of $13.7 trillion. Companies are not investing this money because the demand for new production simply does not exist, sure a few upgrades are in order but that is already figured into business on a year by year basis. Also, little reason exists to buy a competitor or attempt a takeover while stock prices are so high.

Instead what we have seen and continue to see is that companies are plowing money into stock buybacks. All this reinforces what I and many others thought regarding the strong tilt of Trump's tax bill towards rewarding America's wealthy. The bill was not about tax reform and will only add to the trend of growing inequality. The fact is Trump's tax reform has prompted a surge in buybacks courtesy of offshore cash repatriation. It is estimated this will boost EPS growth by more than twice what U.S. economic growth would do. This, of course, does little in the way of creating real economic growth. Tomorrow in part two of this series titled; "Stock Buybacks Driving Market - Where It Might Take Us!" I will put forth some ideas on where this stock buyback mania will eventually end.

Part two has now been published. To continue reading, (CLICK HERE)

Buybacks Have Created A Dangerous Illusion (click here)

Buybacks should be viewed as a double-edged sword with great power in that they reduce the number of shares over which earnings are divided at the same time they add to market demand. This gives the impression the companies earnings are increasing while in reality, overall earnings may be flat or even on the decline. The deregulation of buybacks years ago has returned to haunt us because it tends to create a dangerous illusion that draws less sophisticated investors into a market that is not nearly as strong as it appears. The new recently passed tax law which lowers corporate taxes and encourages repatriation of cash that has been stored overseas is feeding fuel into the share buyback frenzy.

To be perfectly clear, buybacks are a tool corporate boards and CEOs use to manipulate the prices of their own shares higher. This means insiders can get out or hedge their positions before reality sets in and prices fall back to earth. Call it a well constructed exit strategy if you like. This is where I remind you it is major investors that sit on the board or hold executive positions and the same CEOs and other top managers who have received much of their compensation over the years in stock options. Yes, these are often the shareholders in the company that have reaped the largest benefits of QE over the years and added to inequality.

Buybacks Have A Darkside And Drive Inequality

This is already causing a backlash among politicians as they learn the talk about the money corporations saved from the tax cut would flow to develop businesses. They are not building new plants, developing new products or boosting wages, it was simply a lie. Murmurs are beginning to grow in Washington this situation needs to be addressed, however, do not expect any action soon. This issue sits low on the agenda of a dysfunctional government and lawmakers that are already slammed by more pressing matters. Casting their eyes towards coming elections, however, this is an area of law Democrats will focus on during the mid-term election cycle but the fact is a Democrats would need a massive victory before a law could be passed that would end buybacks. I suspect the issue will not be addressed until long after the damage is done and investors have been raped and plundered.

Several unusual currents are running through the market right now, one of those is low volatility of which share buybacks are a major contributor. This is because buybacks are insensitive to price and simply steps in and are ready to purchase on any weakness. With this in mind. it is important to remember that much of the buyback action over the last several years prior to the Trump’s tax changes has been financed from debt raised by selling corporate bonds. This means many companies will not have the money to keep their stock flying when the market begins to fall and leveraged companies will get hammered. These most likely are not the companies with cash stockpiles overseas that can now be repatriated cheaply and to make matter worse they now face higher interest rates.

Buybacks are why we have been hearing so many analysts touting the line that stocks are not overvalued and how earnings are growing. What they are referring to is earnings per share, and what is really doing better in that fraction is the denominator. Records show U.S. firms have spent roughly $4 trillion on buybacks since 2009, this means corporations have been the biggest single source of demand for U.S. shares during the so-called recovery. It is reported by 13D Research that buybacks have “accounted for more than 40% of the total earnings-per-share growth since 2009, and an astounding +72% of the earnings growth since 2012. Simply put, many corporate boards have made the decision to drain the company coffers in order to buy back shares, often from themselves and sometimes even in special deals offered only to themselves off the general market.

This is why according to an IMF estimate from last spring that large U.S. corporations have experienced a negative net equity issuance of $3 trillion since 2009. Linked to these share buybacks we have seen U.S. corporate debt to soar to an all-time high of $13.7 trillion. Companies are not investing this money because the demand for new production simply does not exist, sure a few upgrades are in order but that is already figured into business on a year by year basis. Also, little reason exists to buy a competitor or attempt a takeover while stock prices are so high.

Instead what we have seen and continue to see is that companies are plowing money into stock buybacks. All this reinforces what I and many others thought regarding the strong tilt of Trump's tax bill towards rewarding America's wealthy. The bill was not about tax reform and will only add to the trend of growing inequality. The fact is Trump's tax reform has prompted a surge in buybacks courtesy of offshore cash repatriation. It is estimated this will boost EPS growth by more than twice what U.S. economic growth would do. This, of course, does little in the way of creating real economic growth. Tomorrow in part two of this series titled; "Stock Buybacks Driving Market - Where It Might Take Us!" I will put forth some ideas on where this stock buyback mania will eventually end.

Part two has now been published. To continue reading, (CLICK HERE)