Troll Wanker posting more foolish nonsense .

Part of a real News Report -- Zero Hedge right now

August Unemployment Rate Unexpectedly Spikes As Payrolls For Every Month In 2023 Is Revised Sharply Lower

August Unemployment Rate Unexpectedly Spikes As Payrolls For Every Month In 2023 Is Revised Sharply Lower

FRIDAY, SEP 01, 2023 - 01:59 PM

Ahead of today's payrolls report consensus was already ugly And while moments ago we got a number which was at least nominally stronger than expected, the report in general was weak enough to suggest that - as we expected - the wheels are finally coming off the US labor market (as this week's JOLTS report strongly hinted).

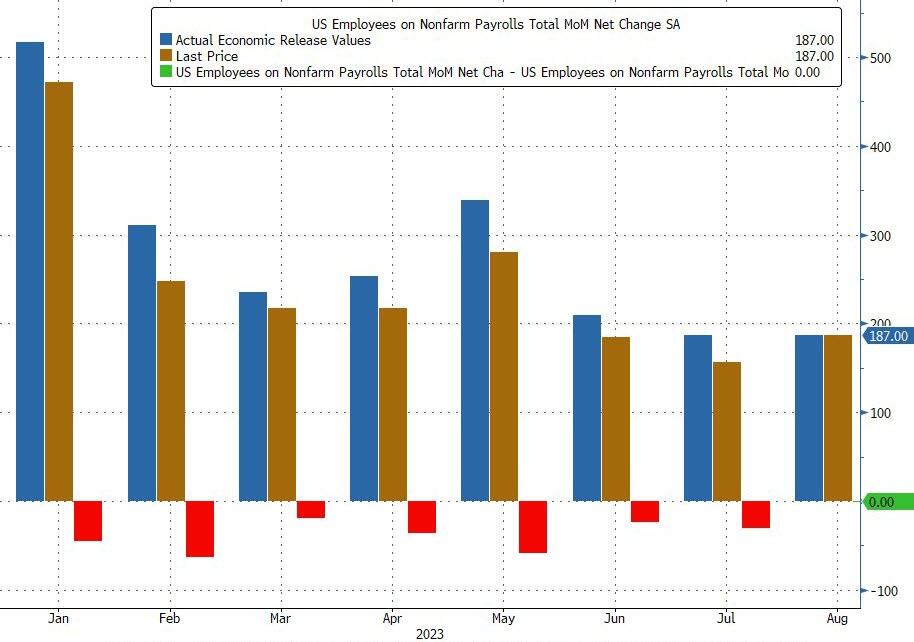

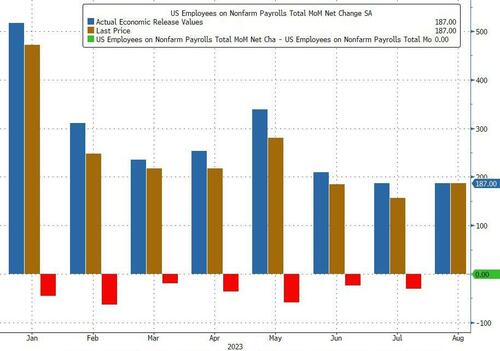

With that preamble out of the way, moments ago Biden's BLS (Bureal Of Lies and Statistics) reported that in August, the US added 187K jobs, and beating the consensus estimate of 1Superficially this would have meant an unchanged print from last month when the BLS also reported 187K jobs, however in keeping with recent trends that number was revised - drumroll - lower again, to 157K, meaning that every single monthly payrolls print in 20-23 has been revised lower (see chart below), a 12-sigma probability and virtually impossible unless there was political pressure to massage the data higher initially and then revise it lower when nobody is looking.

But wait there's more: while July was revised down by 30K from +187,000 to +157,000,

June was revised even more, by 80,000, from +185,000 to +105,000, which means that a number that was originally reported as 209K has been reivsed 50% lower, to 105K and a collapse vs original expectations of 230K. Here, the BLS was proud to report that "with these revisions, employment in June and July combined is 110,000 lower than previously reported."

In other words, we now wait for the August payrolls number to be revised sharply lower as well because that's how Biden's handlers roll.

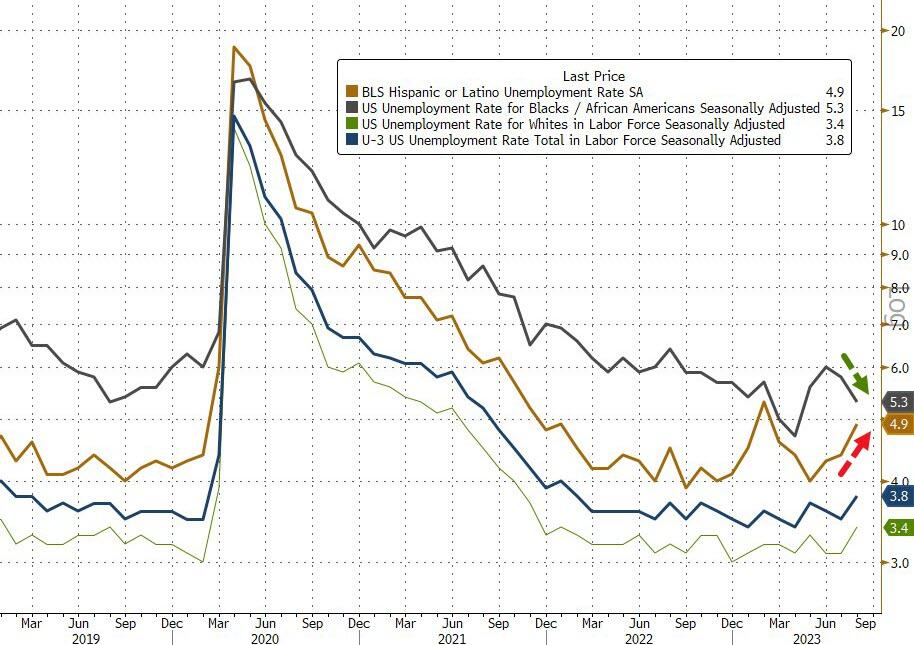

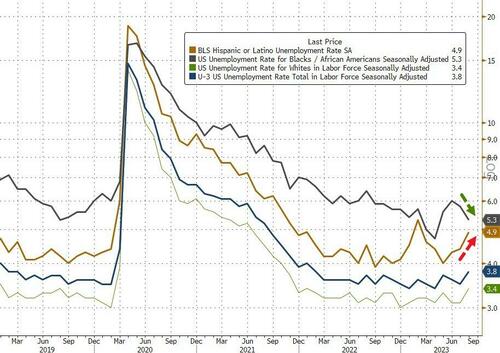

Turning to the unemployment rate, things here get really ugly: instead of the 3.5% expected print, in August the unemployment rate jumped to 3.8%, up sharply from 3.5% in July, and the result of 514K newly unemployed workers as the total civilian labor force increased by 736K individuals, as there were

597,000 new entrants in the labor market, people looking for work for the first time, and the highest level since October 2019. This confirms what we have been seeing:

the savings are tapped out and credit cards are maxed out.

The jump in the unemployment rate means that the economy was

only able to absorb a net 77K of them in August. At the same time, this surge in new workers also suppressed wage growth (as noted below).

Among the major worker groups, the unemployment rates for adult men (3.7 percent), Whites (3.4 percent), and Asians (3.1 percent) rose in August. The jobless rates for adult women (3.2 percent), teenagers (12.2 percent), Blacks (5.3 percent), and Hispanics (4.9 percent) showed little change over the month. The silver lining was that the participation rate actually rose from 62.6% to 62.8%, and is gradually catching up to where it was before the pandemic.

Next, turning to wage growth, August payrolls rose 0.2% MoM, down from 0.4% last month and missing expectations of 0.3%. On an annual basis, the 4.3% print came in as expected, and down modestly from 4.4% last month.

Some more details: In August, average hourly earnings for all employees on private nonfarm payrolls rose by 8 cents, or 0.2 percent, to $33.82. Over the past 12 months, average hourly earnings have increased by 4.3 percent. In August, average hourly earnings of private-sector production and wheels are indeed coming off the labor market, but the BLS is doing its best to make the hit as comfortable as possible. Meanwhile, as Bloomberg's Enda Curran writes, on a net basis, "these figures probably don’t change the Fed debate. They broadly show a labor market that’s cooling at a very controlled space, in line with slowing inflation. That’s a good outcome, but it’s unlikely the Fed will declare mission accomplished."

Below we share some more hot takes on today's print:

li Jaffery, an economist at CIBC Capital Markets, has this take:

“Overall, today’s report underscores that rebalancing in the labor is picking up pace and softening in labor demand could translate into even weaker income and spending ahead.”

Rubeela Farooqi, chief US economist at High Frequency Economics:

“We think these data support the case for no rate hike at the September FOMC meeting. As for the rate path past September, our base case remains that the Fed is at the end of the rate-hiking cycle. However, with the economy reaccelerating, posing a potential upside risk to inflation, another increase in rates later this year cannot be taken off the table.”

Richard Flynn, managing director at Charles Schwab UK:

“While Jerome Powell recently reassured the market that progress is being made against inflation, he did so with the caveat that if the labor market remains strong, more work still might be needed. Today’s report may signal to the Fed that inflation could remain elevated, prompting them to continue rate hikes in months to come.”

Peter Tchir of Academy Securities

“I think today’s number is perfect for that and think we could squeeze nicely into a new month!... If anything, the data is almost weak enough to spur recession fears, but I don’t think there is enough in here for that, and the reality is the Fed must be jumping up and down with joy about the unemployment rate -- not just that it moved higher, but that it moved higher for all the right reasons!”

Derek Tang, economist with LH Meyer/Monetary Policy Analytics.

“Under the surface of the strong headline payroll print there is some support for the doves’ preference for no more hiking. After all, we are seeing negative revisions to previous months, slightly lighter wage growth, and still-rising participation. A September hike hasn’t been the base case, and this only rules it out more. The real issue is how to square it with the super-strong growth numbers we’re seeing. That will keep the FOMC hesitant to declare an end to rate hikes. The window for another hike begins in November.”

Ali Jaffery, economist at CIBC Capital Markets:

“Overall, today’s report underscores that rebalancing in the labor is picking up pace and softening in labor demand could translate into even weaker income and spending ahead.”

Ian Lyngen at BMO Capital Markets says:

“Monetary policy implications are relatively straight forward -- it just got a lot harder to justify a hike in the fourth quarter.”

Stronger Banking means no Troll Wanker Wanking .