I would like to see an insurable interest requirement for all credit default swaps. It is amazing to me such a regulation does not exist to this day. The lack of this requirement played a big part in the last crash.

That still turns my head

round & round.....to my understanding (

limited) the entire scenario orbits profiting on an impending

failure.....

this big, dynamic, complicated economy of ours needs basic regulations in place, my friends, to make sure markets work.

We had 'em, they broke 'em......now i don't profess intricate knowlege beyond what i read.....but it would appear the punsihment (if any) justifies the crime.....

Bloomberg - Are you a robot?

~S~

This is a strange line of thought to me.

"insurable interest requirement for all credit default swaps"

Huh? Credit default swaps ARE the insurance.

There is nothing super complicated about it. It is actually one of the most easy to understand concepts in the world.

I am a lender. I am lending to a large corporation. The debt is large enough, that I worry about if the company defaults.

I want insurance on this debt, that just in case there is an off chance the company defaults, that my company will be able to survive the loss.

So I take out a credit-default swap. I pay this bank a quarterly payment, and in return I have a payout if the company defaults on their debt.

This would be the same as car insurance. I pay a monthly premium, and in return if there is an accident, the company gives a payout for what is covered.

A credit default swap, is nothing complicated or mystical. It is simply insurance for a default.

There was no crime here. Without credit default swaps, the crash would have be far worse. A ton more institutions would have been in financial difficulty, if not for the mitigating effect of Credit Default Swaps.

You are terribly, horribly, seriously wrong.

Insurance requires an insurable interest. CDS do not.

When you say "There was no crime here", you are also being terribly misguided. CDS is like burning down your neighbor's house and saying "There is no crime here" because there are no laws against arson. While technically correct, it is a truly fuckwit thing to say.

Now pay attention.

If you borrow $200,000 to buy a house and it burns down, you still have to pay back that $200,000. And you have no house.

That totally sucks.

So you buy insurance. In fact, for a government backed loan, you are required to buy insurance.

Cool. All is good.

But what about the other end of this deal? You loan $200,000 to someone and then they default. They don't pay you back. ****! You're out 200 grand!

And that is what the CDS was invented for. It was insurance a lender could buy to cover the risk of default.

But here is where our politicians really screwed the pooch, ladies and gentlemen.

The inventors, sellers, and buyers of CDS did not want a CDS to be called "insurance". In federal law, there are all kinds of rules surrounding any insurance product. And the free wheeling marketeers HATE regulations. They dodge and evade them as much as possible.

So let's not call a CDS insurance any more, mm-kay? SHHHH! (*wink wink*)

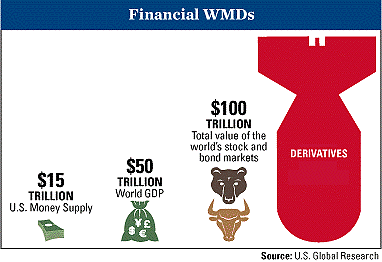

We will call a CDS a...ummm...hmmm...aha! We will call it a "derivative"! Yeah, that's it.

Now why didn't anybody want to call a CDS what it is? Why didn't they want to call it insurance?

Because insurance has this annoying thing called an "insurable interest" requirement.

This simple regulation prevents homicides, arsons, and all kinds of other nasty things. Man, I hate regulation!

If you own a house, you buy fire insurance against that house because you stand to lose money if it burns down.

If the house of someone across town burns down, you don't suffer a financial loss. This means you do not have an "insurable interest" in that stranger's house.

You cannot buy fire insurance against a stranger's house because of the insurable interest requirement.

The reason you cannot buy insurance against a stranger's house is pretty obvious. There would be a shitload of arsons. A guy could buy insurance against a stranger's house, make a single premium payment, and then torch that stranger's house to the ground and collect the insurance.

If there wasn't an insurable interest requirement for life insurance, we could all insure that black guy down the street and then lynch the shit out of him and make some profit at the same time! U-S-A! U-S-A! U-S-A!

So not all regulations are bad, eh? Some save lives and money.

But imagine if you could buy fire insurance against a stranger's house. Imagine if everyone could.

A $200,000 house could have ten policies against it by strangers. Now if the house burns down, the insurance company isn't out $200,000. It is out $2 million!!!

And that is the problem with CDS.

They do not have an insurable interest requirement. They are totally unregulated.

That is why all the players went out of their way to get the regulators not to call a CDS "insurance".

But why would they do that? Isn't that ******* CRAZY!?!

Yep.

But we are talking about people who have moral qualms about lynching for profit, so to speak.

With a CDS, a person could bet against your mortgage burning down. Not kidding.

Now think about that.

If you are an arsonist, what's a sure way to guarantee a bunch of mortgages are going to burn to the ground?

You lend money to people you know can't possibly make the payments. Then you build a CDO out of those mortgages. Then you build a synthetic CDO on top of that toxic CDO.

But since there isn't even an insurable interest requirement for CDS, you can go out and find toxic mortgages which you didn't even make, and pack them into your synthetic CDO!

Then you sell the tranches for that synthetic CDO to some mushroom investors who you don't tell you built this whole firetrap. They have no idea you are on the other side of the bet, because you used a broker-dealer at Goldman Sachs as your cutout.

Then you throw the match and collect the insurance.

And that, ladies and gentlemen, is exactly what ABACUS 2007 AC-1 was all about.

FMI:

Factbox: How Goldman's ABACUS deal worked | Reuters