This is an article that was posted 2 months before Obama took office. Everything in it has proven to be true. It's strange how all of this information has been out there for years yet little bits and pieces of it keep surfacing. The left will claim that it's all old news and they'll say that anyone who brings it up is just trolling. I expect the usual USMB members to do their jobs and attack me personally. Well, bring it on:

As a

New York Post article describes it:

A 1995 strengthening of the Community Reinvestment Act required banks to find ways to provide mortgages to their poorer communities. It also let community activists intervene at yearly bank reviews, shaking the banks down for large pots of money.

Banks that got poor reviews were punished; some saw their merger plans frustrated; others faced direct legal challenges by the Justice Department.

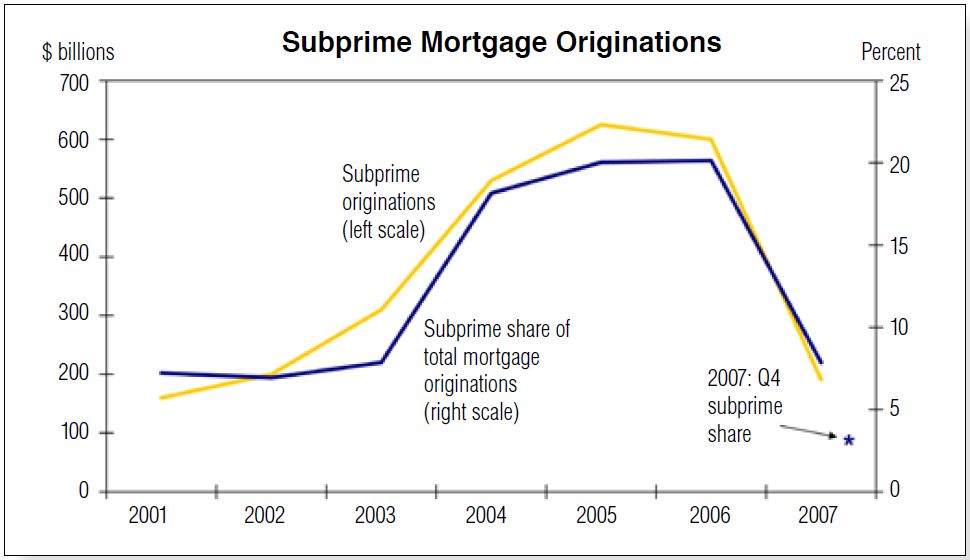

Flexible lending programs expanded even though they had higher default rates than loans with traditional standards. On the Web, you can still find CRA loans available via

ACORN with "100 percent financing . . . no credit scores . . . undocumented income . . . even if you don't report it on your tax returns." Credit counseling is required, of course.

Ironically, an enthusiastic Fannie Mae Foundation report singled out one paragon of nondiscriminatory lending, which worked with community activists and followed "the most flexible underwriting criteria permitted." That lender's $1 billion commitment to low-income loans in 1992 had grown to $80 billion by 1999

and $600 billion by early 2003.

The lender they were speaking of was

Countrywide, which specialized in subprime lending and

had a working relationship with

ACORN.

Investor's Business Daily added:

The revisions also allowed for the first time the securitization of CRA-regulated loans containing subprime mortgages. The changes came as radical "housing rights" groups led by ACORN lobbied for such loans.

ACORN at the time was represented by a young public-interest lawyer in Chicago by the name of Barack Obama. (Emphasis, mine.)

Since these loans were to be underwritten by the government sponsored Fannie Mae and Freddie Mac, the implicit government guarantee of those loans absolved lenders, mortgage bundlers and investors of any concern over the obvious risk. As

Bloomberg reported:

"It is a classic case of socializing the risk while privatizing the profit."

And if you think Washington policy makers cared about ACORN's negative influence, think again. Before this whole mess came down, a

Democrat-sponsored bill on the table would have created an "Affordable Housing Trust Fund," granting

ACORN access to approximately $500 million in Fannie Mae and Freddie Mac revenues with little or no oversight.

Even now, unbelievably -- on the brink of national disaster --

Democrats have insisted ACORN benefit from bailout negotiations! Senator Lindsay Graham reported last night (9/25/08) in an interview with Greta Van Susteren of

On the Record that

Democrats want 20 percent of the bailout money to go to ACORN!

This entire fiasco represents perhaps the pinnacle of ACORN's efforts to advance the Cloward-Piven Strategy and is a stark demonstration of the power they wield in Washington.

Enter Barack Obama

In attempting to capture the significance of Barack Obama's Radical Left connections and his relation to the Cloward Piven strategy, I constructed following flow chart . It is by no means complete. There are simply too many radical individuals and organizations to include them all here. But these are perhaps the most significant.

In his few years as a U.S. senator, Obama has received campaign contributions of $126,349, from Fannie and Freddie, second only to the $165,400 received by Senator Chris Dodd, who has been getting donations from them since 1988. What makes Obama so special?

His closest advisers are a

dirty laundry list of individuals at the heart of the financial crisis: former Fannie Mae CEO

Jim Johnson; Former Fannie Mae CEO and former Clinton Budget Director

Frank Raines; and billionaire

failed Superior Bank of Chicago Board Chair Penny Pritzker.

........

Most significantly,

Penny Pritzker, the current Finance Chairperson of Obama's presidential campaign helped develop the complicated investment bundling of subprime securities at the heart of the meltdown. She did so in her position as shareholder and board chair of

Superior Bank. The Bank failed in 2001, one of the largest in recent history, wiping out $50 million in uninsured life savings of approximately 1,400 customers. She was named in a RICO class action law suit but doesn't seem to have come out of it too badly.

As a young attorney in the 1990s, Barack Obama represented ACORN in Washington

in their successful efforts to expand Community Reinvestment Act (CRA) authority. In addition to making it easier for ACORN groups to force banks into making risky loans, this also paved the way for banks like Superior to package mortgages as investments, and for the Government Sponsored Enterprises Fannie Mae and Freddie Mac to underwrite them.

These changes created the conditions that ultimately lead to the current financial crisis.

Note the repeated theme of using existing laws and expanding their reach thus changing their intended purpose. This has been repeated over and over throughout Obama's tenure as president. He expands on existing laws or programs and renders them unrecognizable. He did this with Fast & Furious and several other programs. The excuse is always that it was a law or program from a previous administration. He's doing the same thing with the Patriot Act. Many liberals here think this is funny, but this is no joke.

ACORN has split up and changed it's name, but it is still highly active. Ferguson was one of it's babies.