JonKoch

Gold Member

- May 14, 2017

- 3,060

- 521

- 130

CLINTON? LMAOROG

Images

Videos

The Clinton administration's policies, particularly the Community Reinvestment Act and the actions of HUD Secretary Andrew Cuomo, significantly contributed to the rise of subprime mortgages and the subsequent financial crisis.

Key

- Community Reinvestment Act (CRA): Originally passed in 1977, the CRA was strengthened during the Clinton years. It aimed to encourage banks to lend to low-income and minority communities. Critics argue that this led to relaxed lending standards, as banks sought to meet CRA requirements by issuing loans to higher-risk borrowers, contributing to the subprime mortgage boom.

2- Andrew Cuomo's Role: As HUD Secretary from 1997 to 2001, Andrew Cuomo implemented policies that expanded access to homeownership. His initiatives included lowering credit standards and promoting loans to borrowers with poor credit histories. This approach, while aimed at increasing homeownership, also facilitated the growth of subprime lending without adequate oversight.

2- Deregulation and Risky Lending: The Clinton administration's policies encouraged a significant increase in subprime lending. By the late 1990s, the subprime loan market had grown substantially, with many loans issued without proper documentation or consideration of borrowers' ability to repay. This lack of regulation allowed lenders to engage in predatory practices, leading to widespread defaults when housing prices fell.

2- Impact on the Housing Market: The push for increased homeownership, particularly among low-income families, resulted in a surge of subprime mortgages. When the housing bubble burst, many of these borrowers faced foreclosure, contributing to the financial crisis of 2007-2008. The Financial Crisis Inquiry Commission noted that while government policies aimed to promote affordable housing, they also played a role in the crisis by encouraging risky lending practices.

2

5 Sources

Let's see if pics will help YOU

From Bush's President's Working Group on Financial Markets October 2008

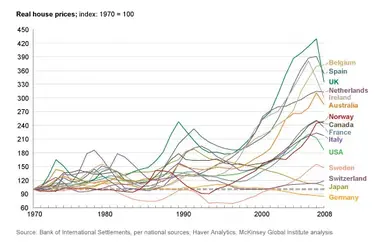

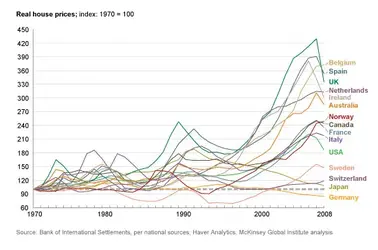

"The Presidents Working Group's March policy statement acknowledged that turmoil in financial markets clearly was triggered by a dramatic weakening of underwriting standards for U.S. subprime mortgages, beginning in late 2004 and extending into 2007.

CLINTON AMD OBAMA HUH? lol