AntonToo

Diamond Member

- Jun 13, 2016

- 38,873

- 12,162

- 1,560

It actually doesn't. It simply subsidizes it. That's a subtle, but important, difference. ACA provides temporary relief for some, but it doesn't do anything to lower health insurance rates or, more importantly, health care prices.

A see a lot of assertions but not much of an argument.

I listed all the things Obamacare does, so when you say "it actually doesn't strive to make health insurance affordable and accessible" you have some 'splaing to do because the list directly contradicts that. And there is nothing "temporary" about any of it.

As to overall healthcare spending, while AHCA is fairly incomplete in that regard there is still much in the law that reduces spending. A lot of noise was made about the SIZE of the law, but half of the pages are filled with pilot programs that further study best ways to approach healthcare delivery (I urge you to read up on that). It puts in incentives to providers to switch away from paper and towards electronic medical records, it cuts medicare/medicaid re-reimbursement rates that drive a lot of pricing in the market, it sets an even playing field for insurance competition that with time will hopefully result in tighter price control on the provider side. And yes, to be fair it also has some provisions that increase costs a bit (insuring and caring for sick people is not free).

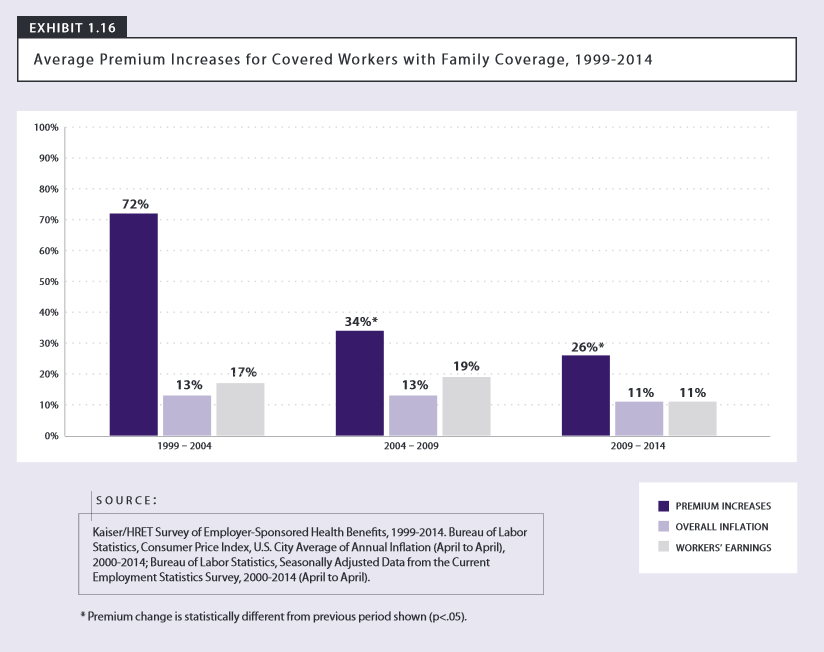

Since AHCA was passed we've had record slow growth in healthcare costs and premiums growth, with about a third of the slowdown attributed to AHCA effects.

Slower Premium Growth Under Obama