Exactly. The whole thing was about being able to brag about how many people had insurance - or, more realistically, insurance CARDS.The Affordable Care Act does not provide access to health care. It provides access to health insurance. Just because you have insurance doesn't mean you can afford health care.

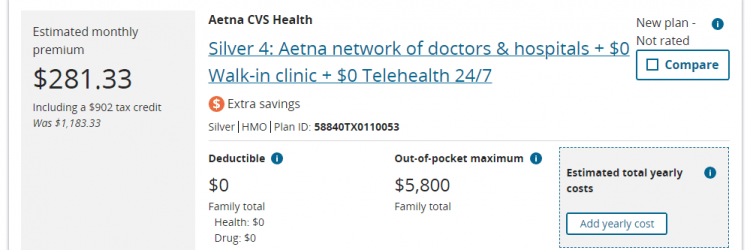

The ACA allows plans to have a deductibles/co-pays of up to $8,700 and required them to have deductibles of at least $2,800. With those kind of deductibles, a worker at McDonald's is not going to be able to access much health care. Not unless he tell the hospital to bill him with a plan to declare bankruptcy. But we were told that the ACA was needed to prevent such financial ruin.

View attachment 743980

Even if you have a subsidy, you are in bad shape under the ACA:

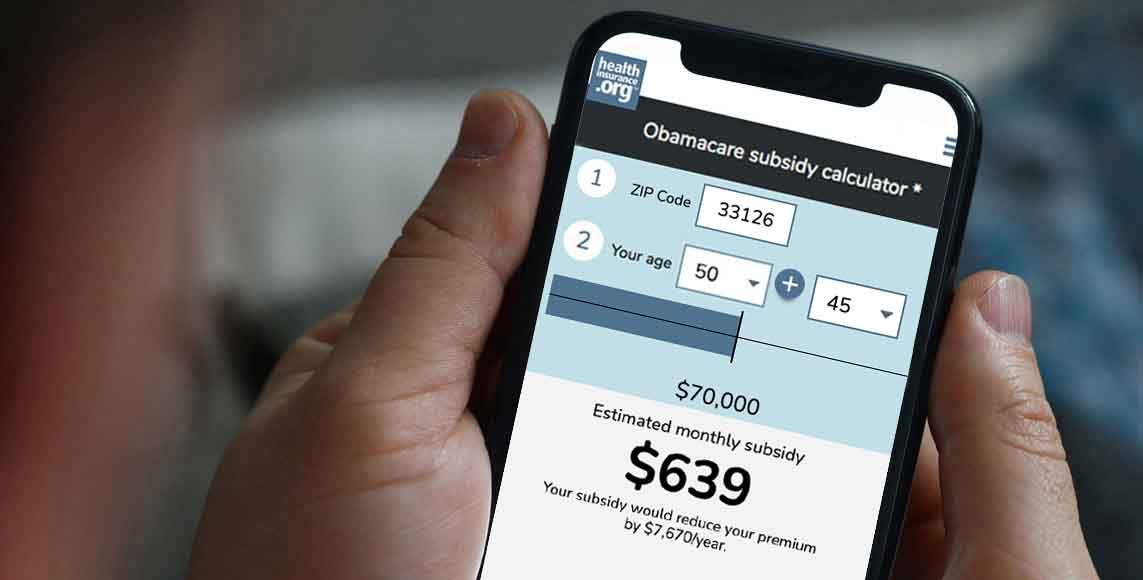

Here is what the healthinsurance.org calculator says the subsidy would be for a working-class family in a small Texas city:

View attachment 743982

Will you receive an ACA premium subsidy? | healthinsurance.org

See who's eligible for the Affordable Care Act's premium tax credits (premium subsidies), how subsidies are calculated, and why they are more robust in 2023.www.healthinsurance.org

Here is a little math:

17,244 (the average yearly premium for a family of four stated above)

Divided by

12 (the number of months in a year)

=

1,437 (the monthly premiums before subsidy is applied)

Minus 458 (estimated monthly subsidy as stated above)

=

979 (the monthly premium the family above would have to pay. Monthly. As in every month.

Nine hundred and seventy-nine dollars for a family of four earning $$3,500 per month before taxes and other deductions is the exact opposite of affordable.

Those are the exact type of people for whom the phrase "it is expensive to be poor" applies. It's not expensive to be a lifelong welfare dolee with no desire to break the dependancy cycle. Everything is free then. It is expensive to try and play by the rules and work hard to achieve the American dream. Those are exactly the people that Democratic policies seem designed to harm.

Suppose that somehow the family is able to afford $979 per month on a gross income of only $3,500 per month. Somehow. Now their daughter has a burst appendix and is rushed to the emergency room for treatment which is an emergency surgery. That treatment will cost well over the $7,767 deductable, leaving the family with that debt.

Again, financial ruin due to medical debt is what the ACA promoters promised to stop.

Obamacare was so bad for me that in some cases, I was better off pretending I had NO insurance and paying the “cash price” rather than the ”discounted insurance price”. One time I needed PT, and the cost per session was $99 for cash payers and $130 for those with the Obamacare plan. So….I was paying $800 a month for insurance for the privilege of having to pay more for medical care than people without insurance at all!