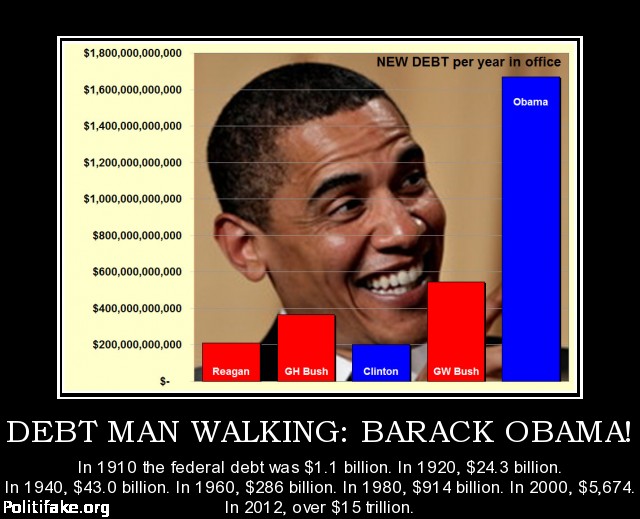

A thought provoking read.

Isn't it Time to Stop Calling it “The National Debt”? - Evonomics

What those scare-mongers don’t tell you, and generally don’t even understand: it actually makes almost no sense to call that figure “the national debt.” And no, you’re not on the hook to pay it back.

Imagine this: you’re the queen or king of a sovereign country. You decide to mint and issue a bunch of tin coins that your people will find useful. You use those coins to buy stuff from people in the private sector, and pay them to do work. Voilà, the people have money.

Is your government now in “debt” as a result of that “deficit spending”? Does it have to “pay” something to somebody at some point in the future? Do you have to redeem those coins for wheat or pigs or anything else? Obviously not. There’s just a bunch of money out there that people can use. You’ve made no promise that your treasury will ever redeem those coins for anything. They just circulate.

Those government-issued assets, held by the private sector, are only “liabilities” to the government in the most pettifogging accounting sense. If you “owed” some money that you would never, ever have to pay, would you put that on your balance sheet as a liability? Would it be anything beyond a pro formaentry designed to satisfy some obsessive impulse for accounting closure? A debt that will never be paid off is a very questionable “liability.”

That’s essentially the situation with the U.S. national “debt.” The U.S. issues money by deficit spending. It puts more money into private accounts than it takes out via taxes. The private sector has more balance-sheet assets (but no more liabilities, so it has more “net worth,” the balancing item on the righthand side of its balance sheet). The treasury has made no promises to redeem that new money for…anything (except maybe…different government-issued assets). It’s just out there.

Now it’s true that the U.S. et al operate under an arguably archaic and purely self-imposed rule: their treasuries are required to issue bonds equal to that deficit spending. This is a straightforward asset swap: the private sector gives checking-account deposits (back) to the government, and the government gives bonds in return. Private sector assets and net worth are unaffected by that accounting swap; it just changes the private-sector portfolio mix — more bonds, less “cash.” (Treasury “forces” the private sector to make that collective portfolio-adjusting swap through the simple expedient of selling bonds at an attractive price — a point or two below similar deals in the private sector.)

The same kind of asset swap happens when the Fed “prints money” for quantitative easing. The private sector gives bonds (back) to the government, and the Fed gives “reserves” in return — deposits in banks’ Fed accounts. Sure, the Fed creates those reserves ab nihilo, but they’re not a money injection into the private sector, like deficit spending. They’re just swapped for bonds. That accounting event doesn’t increase private-sector assets or net worth. It just changes the private-sector portfolio mix (more reserves, less bonds).

In any case, the private sector is holding government-issued assets. Whether they consist of bonds, “cash,” or reserves, is it realistic to call that money originally spent into private accounts a “debt” for the government? Is it in any real sense a government “liability” if it will never be redeemed for anything? Would a better term be “government-issued assets,” or similar?

Look at the U.S. and the U.K. as examples. The stock of government-issued assets from those sovereigns has been steadily (though fitfully) increasing for more than two centuries and three centuries, respectively. (And in the handful of cases where the stock was reduced significantly, the result was major economic depressions.) That centuries-long growth pattern could conceivably change at some point, but…why would governments stop issuing financial instruments all of a sudden — exchangeable instruments that their economies need to operate fluidly, and grow — while their economies continue to expand?

The government has committed itself to issuing bonds for archaic reasons, so it needs to roll over its “debt.” Old bonds mature, the government pays them off and issues new ones to replace them. Unendingly, for decades and centuries. But the stock of government-issued assets just keeps growing — as it should and must in a growing economy.

Those government-issued assets are a necessary lubricant for the operation of the private-sector economy. As the economy gets bigger, more of those assets are needed, as a kind of giant “pool” or buffer stock to avoid transactional lockups. (See: Paul Krugman’s babysitting co-op.) Realistically: will government stop issuing that necessary lubricant, or withdraw what it’s already issued, when the economic consequences of doing so are so dire?

It’s common parlance to say that the private sector is “holding government debt.” That’s understandable, since the private sector is holding bonds. But it’s a misnomer, and a pernicious, confusing one. The private sector is (obviously) holding assets on its balance sheet. The “debt,” such as it is, only exists as an offsetting accounting liability on the righthand side of the government balance sheet. (While “holding debt” is a handy verbal shorthand, if you think about it for a moment the usage makes no sense at all. How can you own something you owe? Debt can’t be an asset that you “hold.” It’s a liability.)

The private sector holds (owns) government-issued assets, not liabilities. And even the offsetting liabilities themselves are rather dodgy and iffy accounting entries. The government issues those assets as a public good. In the big picture over decades and centuries, that’s the end of it.

Another key understanding: Those different types of government-issued assets (bonds, “cash,” reserves, etc.) are straightforwardly fungible in the private market — at least at the margin, where it counts. The private sector couldn’t swap all its government bonds for currency or checking deposits at once (nor, realistically, would it). But if an individual bondholder needs cash for real-goods transactions or whatever else, the necessary asset-swap transaction happens with a mouse click. Likewise holders of checking-account deposits: if they want physical currency, their bank stands ready to make the swap; it’s called “withdrawing cash.” If the bank runs short on physical currency, the Federal Reserve provides it on demand in exchange for the bank’s reserves, its account deposits at the Fed. (With the Bureau of Engraving and Printing standing behind the Fed, presses ready to roll as the transactional economy expands.)

Now the private sector’s portfolio mix certainly has economic import (and even more so, changes in that portfolio mix). But that mix is secondary and subsequent to the total stock of various government-issued assets in play — be they bonds, checking deposits, whatever. Without a sufficient pool of those lubricatory assets, the financial economy binds up and freezes.

Which is why you, as queen or king, issued those tin coins in the first place. The economy needs them to operate smoothly. Sure, you got some one-time free labor out of the deal — “seignorage” and all that. But did you benefit? Maybe you used the labor to build roads. Both the roads and the coins are public goods. You just end up, still, as queen or king — of a more prosperous country. That one-time transaction happens — you issue coins and pay people to build roads or whatever (you “deficit spend”). But those coins (or bonds, or whatever) remain out there forever, for generations, doing the good work that needs doing in the economy. Money makes the world go round.

There’s really no reason to call those coins, or any other financial instrument the queen or king chooses to manufacture out of thin air and swap for those coins, “national debt.” Let’s switch to a term that actually describes the things that we ultimately tally up on the lefthand side of our private-sector balance sheets — something like “government-issued assets.”

There are deep political and economic implications to this kind of rethinking and renaming, but I’ll leave those implications to the ruminations of my gentle readers.

You might be able to reason that debt is meaningless in terms of paying back, but it does mean something when you consider how many tax dollars it requires to pay the interest to private and foreign holders of the debt. And what the KING OF DEBT couldn't figure out is that if we try to make those folks take haircuts, they would demand even greater interest to take any more of our debt. But I realize Donald and real life haircuts are oxymorons.