Yes it is. If it's impossible for new companies to enter a state's market, how did any which are there NOW do it when they were new? Sorry, you're not making any sense.

I didn't say it's impossible for companies to enter the market, I pushed back on the oversimplified assertion that simply having more insurers in the market leads to lower premiums (a claim you yourself also rejected in this thread). The reality is that the situation in most health insurance markets is different from that in many markets. To quote

Austin Frakt:

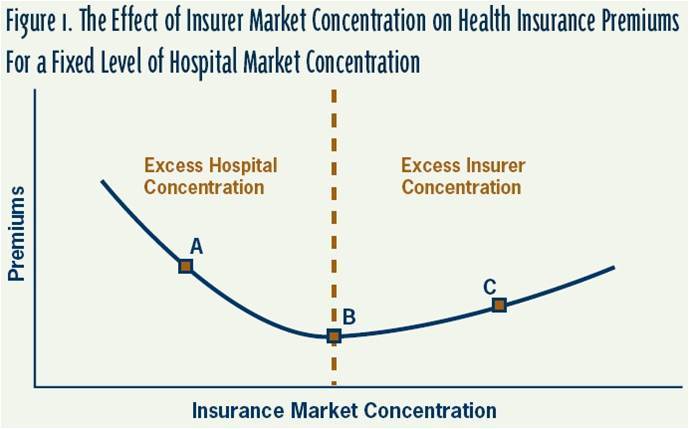

Understanding how hospital versus insurance concentration affects hospital prices and premiums is difficult due to the complex nature of price competition in the market for hospital services. A simplified picture of this complex relationship is illustrated in Figure 1, which shows how health insurance premiums in a market would be expected to vary depending on the balance of power between insurers and hospitals. This curve assumes a fixed level of concentration among hospitals so that the relative balance of power varies as insurer concentration changes along the horizontal axis. When insurance market concentration is low relative to that of hospitals (point A), the dominant hospitals can exercise market power and command relatively high prices from insurers, which are passed on to consumers in the form of higher premiums. As insurer concentration and relative power vis-à-vis hospitals increase (moving from point A toward point B), dominant insurers gain monopoly-busting power and can use the threat of network exclusion to negotiate lower prices and, thereby, offer relatively lower premiums. If, however, insurer market concentration far exceeds that of hospitals (point C), insurers can mark up the lower prices they obtain from hospitals and retain the difference as profit with little fear of losing enrollees to other insurers.

The rough shape of the curve illustrated in Figure 1 can be reproduced with formal economics models and features of it have been empirically verified by numerous studies.

Diluting the insurance market with too many insurers can in fact lead to a significant

rise in premiums due to the alteration in the payer-provider interaction.

You said I want to federalize tort law. Once more, I said no such thing, but pointed out one example how the federal government can encourage reform by sanctioning states if they don't reform their >>>OWN<<< state law.

I said if you're advocating for a federalization of tort law, you're going to run into opposition from far right lawmakers, states, and other allies on the right. I'll also say that if you're simply advocating for federal sanctions on states that don't conform to the federal government's vision of tort reform, you're likely to meet resistance from the very same people.

Positive incentives for state-level tort reform, namely seed money for states to test new and alternative models, were enacted by the feds last year. It remains to be seen what the state response will be.

I don't want to tell fat people or smokers what to do (as long as I don't have to breath their exhaust) but then by same token I shouldn't have to pay, even indirectly, for the consequences of their bad habits.

Health insurance premiums can still be rated for tobacco use.

Be careful. You'll be on a "terruh suspect" list.

Be careful. You'll be on a "terruh suspect" list.