The point of this is that two people here are attempting to arrive at a better understanding of the macroeconomy through a process known as having an intellectual discussion. Note that while they often disagree, they do so without being DISAGREEABLE? ...This thread is an exploration by two intellectually honest guys trying to determine how to figure out the relationship between money supply and macroeconomic outcomes. Those of us, like myself, not well versed in macroeconomic theory, CAN follow it, if we're willing to read their posts thoroughly. First of all, they question how do we measure the monetary supply (and its velocity within the economy at any given time) and how does (or how should) that economy alter the money supply to continue to best serve the economy? What I especially like about their style is both of them are coming at this discussion admitting that they don't have the answers. They both know they are SEEKING the answers. This kind of humility is quite typical in great SOCIAL SCIENCE discussions. The target of this KIND of discussion is to find the TRUTH, not win the debate.

Here is what I've learned so far.

Actually, the pure math guy, the applied economics guy, and the applied math guy haven't disagreed in the least. There can be no disagreement because any appearance of disagreement is inevitably due to looking at different things or based on preference. Preference is just preference.

Oh, sure, the pure math guy says something like, "You don't map variables to objects, you look for interesting things you can do with the math." But then, we understand he has this wealth of doing the "look for interesting things", so it's more like his personal preference.

And sure, the "applied economics guys says something like, "but you can use any money supply you choose and then you have this liquidity trap thing". But then, we understand that, in practice, the monetary base is what the Fed measures so it makes sense, from an applied position, to use that.

I know that there are interesting things that can be done with the math that also has utility. I know that it is true that the V_Mb = GDP/Mb has utility.

What the pure math guy and the applied econ guy have given me is a better understanding of how Friedman approached it and how the applied science of economics approaches it to come up with something that either the business guy or the Federal Reserve guy can use.

As more of an applied math guy, I know that it is true that you can map variables to objects and that it has utility. I also know that a lot can be gleaned from economics without needing to go to calculus. Algebra and trig is enough. I also know that most people intelligent enough to read are intelligent enough to understand the stuff. Any problems they have experienced had to do with how the studies went or a matter of being use to it. It's just a second language. All I am after is some basic insight that can be gleaned from a comprehensive view of the basics.

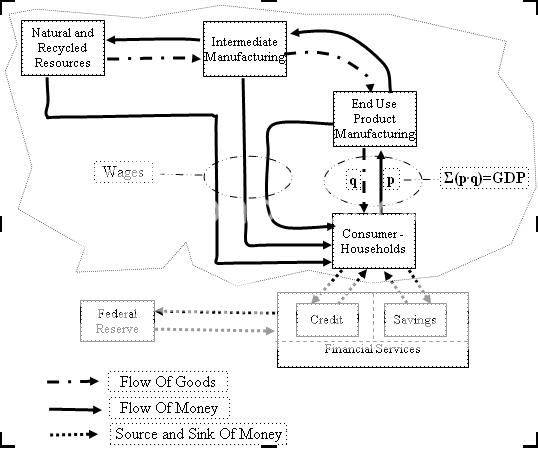

From an applied math standpoint, we can go downtown, observe people and what they do, and construct a model that is a viable representation of how the economy functions. Of course, we've been downtown and actually been the "people" that we just need to think about it. What we end up with is M=PQ. In fact, if M is the money we are spending at the store and PQ are the groceries, then it's pretty obvious that if we had more M then we can buy more PQ.

And when we think about the entire economy, we recognize that it's just more of the same multiplied a couple of hundred million times. So we can create a flow diagram like

I haven't invented anything here. It's just a flow diagram and another version of the same economic flow diagram found all over the place. I've boiled it down to the basics, the things that are significant.

And because anything worth saying in the first place, is worth repeating, let me explain. The money flows in a closed loop. Ignoring the financial services thing, all the money goes around in a closed loop so wherever you cut into the flow, it's the same. Total wages equals total purchases. What is spent on consumption has to equal income. I can't take home stuff from the store that I didn't pay for and I can't pay for stuff with money I don't have.

So, by definition, GDP is the total of the prices times the quantities of all the goods that are purchased at the final use level. That is GDP = PQ. And obviously, it is equal to the total amount of money in the flow with one caveat. Someone was clever enough to notice that the dollars often go around that loop more than once in accounting for P.

So, M_flow*V_flow= PQ = GDP.

If we go back to Hume, we see that he said, M_flow = PQ. He wasn't so formal about it, but that's what he said.

Over the history of economics, it went from Hume, to Mills, to Fisher, to god knows who else, to Keynes, to god knows who else.

Somewhere along the way, the velocity of money was added. A good thing to because that isn't so obvious. Then Keynes adapted it to Money Demand and changed the V to a 1/k.

And, because we can't measure M_flow, someone came up with using the monetary base, and it became Mb * V = PQ. Except, then V isn't V_flow, it's partly V_flow and partly the "liquidity trap" or whatever it is that is keeping Mb from getting into M_flow.

All this history is a bit beside the point, because M_flow*V_flow = PQ = GDP is absolutely correct. And because P is using the money from M_flow, just more than once, as measured by V_flow, then a few simple things can be concluded. And, they are the same things that Hume was nice enough to write down in the first place in his essay "On Money".

One thing to note is that, without other information, MV=PQ doesn't say anything about causality, just what must happen together. Assuming V is constant, if M goes up, P and/or Q go up. This was Hume's observation. Whenever a country or region had more money introduced into it, the standard of living increased. And, often enough, prices also went up. In "On Money" he spells out what happens to make the different. He also points out that, in every region where the supply of money was depleted, the standard of living fell. Hume must have traveled a lot.

Of course, it is interesting to notice that in those days, people actually had to carry a purse with gold coins around. Now, we never need to even go to the bank. Our paycheck just gets electronically deposited and we use a debit card for purchases. It should be apparent that the velocity of money has been increased due to that. Though it is actually frequency, the number of times around a circle. If it goes faster along the edge of the circle, it's going around the circle faster.

Oh, if you want to, you can stick the government and taxes in there. But, effectively, the government is just another company, that we all subscribe to, with a different pricing scheme that depends on the "board of directors" that we appoint during the election process. Splitting it out doesn't add any new information. If you think it does, by all means, split it out and make things more complicated. I don't like things any more complicated than necessary. Things should be only so complicated as they need to be, and no more.

Now, I haven't touched on that savings and credit thing. Those are sinks and sources for M_flow. As far as I can tell, that is all the sources and sinks. Obviously, money goes into saving and comes back out later, even with a little bit more money. And that little bit more money doesn't just materialize out of thin air. It got there because someone else took out credit, then put that back in again, with a little bit more money.

And now, were discussing how this think changes over time.

And, you might want to stick China in there, but functionally, it's just another big company in the flow. Money flows into it and they put it into the bank, then the other company called the government, borrows on credit from them and puts the money into the flow. And, every so often, one of those big companies, like Dubai, actually do buy, or try to buy, something.

You might want to have the intermediate companies have savings and credit. This doesn't add any new information.

The savings and credit balance. They have to unless the Fed does something to change the amount of money.

Still none of this changes Hume's fundamentals that M_flow * V_flow = PQ or the BEA PQ = GDP. And it points out that, if GDP, CPI, or population are to go up, then M_flow has to go up if V_flow doesn't change. It must go up, just like your income must go up with your expenses because the bank isn't going to let you carry a negative balance. Well, for that matter, that is why it must go up. Because all those households don't get to use any more money than they have. That is how our accounting system works. That is how the banks do accounting. That is how the economy does accounting.

None of this says anything about how prices and quantities find that equilibrium point in the market. It's not suppose to. But it does say that if M and V stay the same, and one PQ goes up, then other PQs go down.

It's not meant to predict inflation. It's not suppose to. But it does say that, if there is inflation, then M_flow has to go up or the quantity of something must come down, assuming V_flow doesn't change.

And, as far as I know, the only way M_Flow does go up, is if the Fed "prints" money and sticks in it that financial institution thing. As far as I know, they don't stick in any savings account for free. They stick it in the reserves account of banks where it becomes a source of credit. In order for it to get to M_flow, someone borrows it. But that means, they pay it back later.

You can make that financial services all more complicated by detailing every fractional reserve and private bank, but it doesn't add any new information.

But, by all means, if anyone can tell me how M_flow increases without the requirement of credit, I'm dying to know. There is no magic here, no complicated annuity expressions. CDSs, derivatives, straddles and swaps, MBS, stock, T-bills, whatever, is just moving back and forth between savings and credit accounts. An IPO moves money from one guys savings to a companies savings in trade for a contract of repayment and dividends. That is great. But it's just another, out of a savings and into the flow. Sure, some company makes a business loan which increases their savings that then pays for intermediate capital equipment that then creates a new product stream for Q. But, that loan gets paid back and it doens't permanently increase M_flow.

All it takes, is one little connection from that block labeled "Fed" to that block labeled "savings". Just one little line will fix it.