.

The sub-prime loans would not made if there were not consumers willing to sign on the dotted line.

The sub-prime loans would not have been made if there were not buyers and sellers for them on secondary markets via MBS's.

The MBS's would not have existed if regulators had taken a look at them, realized pretty much no one knew what the hell they were, and acted accordingly.

There would not have been buyers for the MBS's if the ratings agencies had given them appropriate ratings, such as S&P's CCC, about where they should have been.

Those selling the MBS's would not have been able to move risk off their books if someone not been willing to sell them CDS's.

Those selling the CDS's would not have been able to sell them if they had been required by regulators to maintain standard insurance reserves.

On and on. All kinds of different people, all over the freakin' place.

But instead, let's just simplistically and transparently point the finger at those guys, over there. Yeah, those guys. Oh look, they just happen to have (R)'s after their name.

Yeah, that's easier.

.

And even there you have problems.

For example, who created Mortgage Backed Securities? Government.

Who created derivatives? Government.

Who gave sub-prime mortgage backed securities a AAA rating? Government.

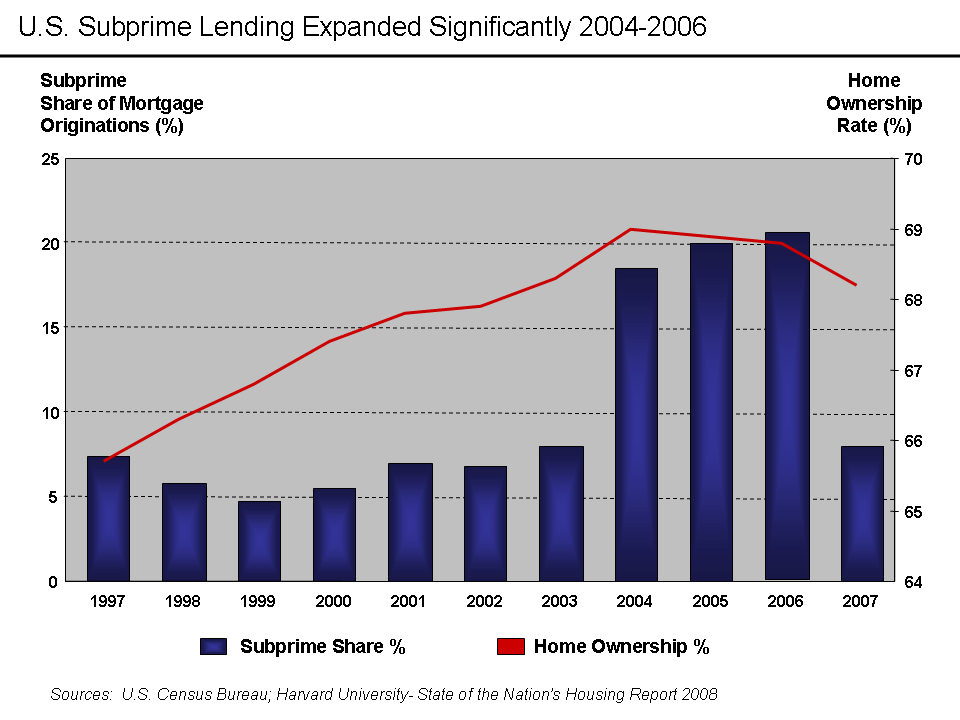

The left doesn't even bother to try an isolate out, when the problem began. When did this whole sub-prime loan bubble, and housing price bubble start?

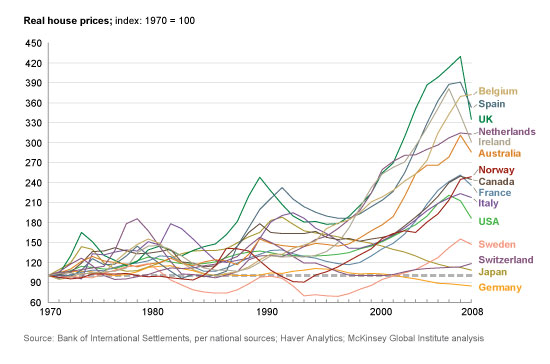

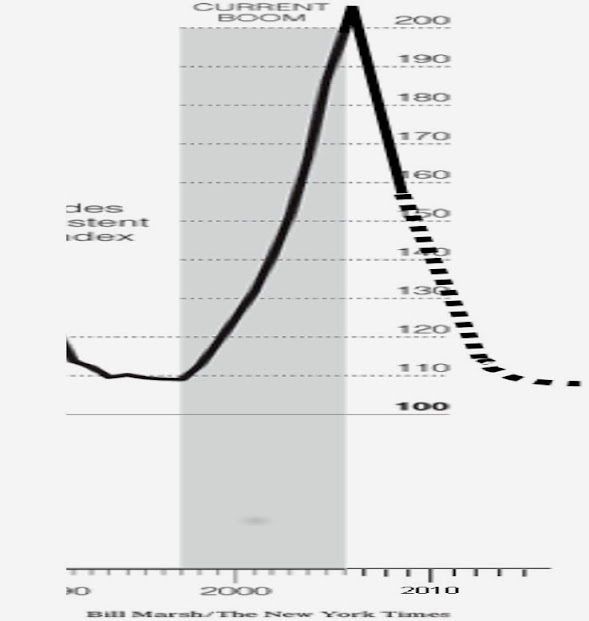

Well it's pretty clear that something happened in 1997. Because before 1997, there were barely any sub-prime mortgage backed securities.

Of course the left now claims that's all bogus. But when did the housing price bubble start?

Well looky there! Let me blow that up for you.

That's 1997 when housing prices started to rise.

So according to trade publications, the documented expansion of sub-prime mortgages, coincides with the start of the housing bubble..... what a coincidence....

And wait a second... didn't the repeal of Glass Steagall happen in 1999? Two full years AFTER the dramatic raise in sub-prime mortgage backed securities, and the start of the housing bubble? Why yes that's true!

Which leads me to what I personally believe is the smoking gun...

First Union Capital Markets Corp., Bear, Stearns & Co. Price Securities Offering... -- re> CHARLOTTE, N.C., Oct. 20 /PRNewswire/ --

First Union Capital Markets Corp.

and Bear, Stearns & Co. Inc. have priced a $384.6 million offering of

securities backed by Community Reinvestment Act (CRA) loans - marking the

industry's first public securitization of CRA loans.

The affordable mortgages were originated or acquired by First Union

Corporation and subsidiaries. Customers will experience no impact - they will

continue to make payments to and be serviced by First Union Mortgage Corp. CRA

loans are loans targeted to low and moderate income borrowers and

neighborhoods under the Community Reinvestment Act of 1977.

"The securitization of these affordable mortgages allows us to redeploy

capital back into our communities and to expand our ability to provide credit

to low and moderate income individuals," said Jane Henderson, managing

director of First Union's Community Reinvestment and Fair Lending Programs.

"First Union is committed to promoting home ownership in traditionally

underserved markets through a comprehensive line of competitive and flexible

affordable mortgage products. This transaction enables us to continue to

aggressively serve those markets."

The $384.6 million in senior certificates are guaranteed by Freddie Mac

and have an implied "AAA" rating. First Union Capital Markets Corp. is the

investment banking subsidiary of First Union Corporation (NYSE: FTU).

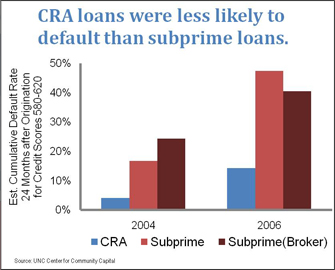

Now let's review the highlights.... FIRST securitization of sub-prime loans.

Before 1997, I can not find a single example of a sub-prime loan being guaranteed by Freddie or Fannie.

Note.... securitizing, does not mean buying. Freddie and Fannie did not buy the loan, they stamped their approval on the loan. So when leftists look at the balance sheets of Freddie or Fannie, they don't see the sub-prime loans, but in reality their are directly and intimately involved in the sub-prime loans.

They gave the loan an implied AAA rating. Before 1997, I can find no record of any rating agency given a sub-prime loan any rating, let alone a AAA rating.

Rating agencies tend to not bother to rate something they know, will not score high enough to be above junk status. They only give junk status to something that prior to, had a higher rating.

All of that was the carrot.... where the stick? Here's the stick.

[ame=http://youtu.be/gpj4gcdm_JQ]HowThe Democrats Caused The Financial Crisis Starring HUD Sec Andrew Cuomo & Barack Obama - YouTube[/ame]

Andrew Cuomo of the Clinton administration, in 1998 suing banks to make bad loans. He openly admits these are loans to people who are not qualified, and that defaults will be higher.

So on the one hand, we're securitizing bad loans with Freddie Mac, and on the other we're taking banks to court for not making those loans.

Then we look at the sub-prime loans shooting off in 1997, and the housing bubble starting in 1997, and we're just SHOCKED! SHOCKED I SAY! That banks agreed to engage in the sub-prime market?

It doesn't seem that hard to figure out to me.