Okay so I've been looking through some data trying to find any evidence that buying long bonds in quantity lowers their yield.

QE2 was announced Nov 2010. On Nov 18th 2010 the Fed held 806 billion in T-notes and bonds (

here). By Jan 13 2011 they held 987 billion (

here). They increased their holdings by $180 billion.

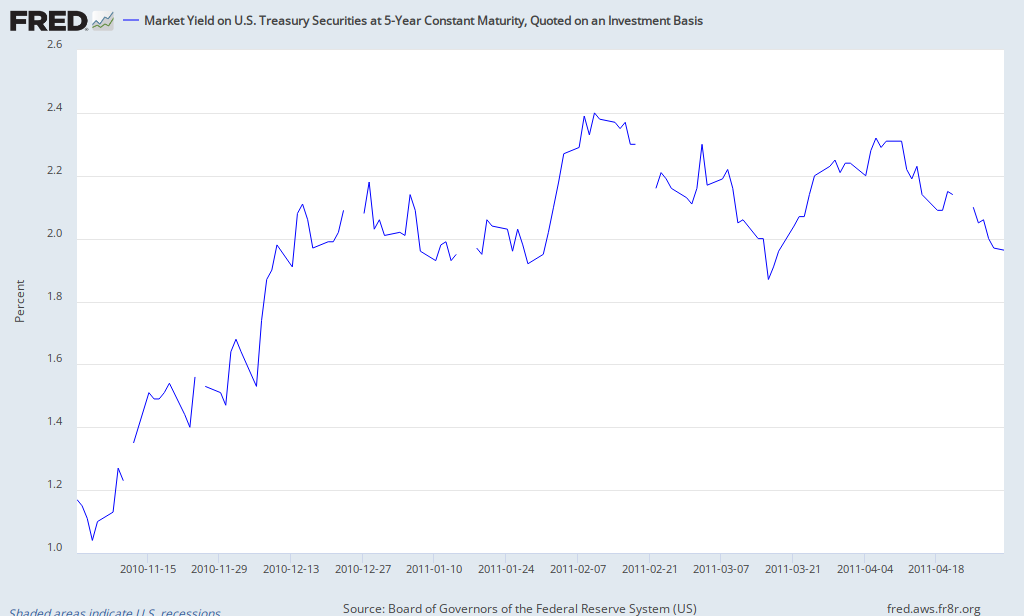

5-Year yields over that period:

Shouldn't buying up all those bonds have dramatically lowered the 5-year yield?

It did. But you're not looking at it correctly. First, you don't start in November. You start from when Bernanke gave his Jackson Hole speech on August 31, not when they actually began buying. THAT'S when the market began to price in QE. Markets moved in anticipation of the buying. The market also reacts because the market expects quantitative easing. So if the market believes that the Fed will buy again in the future, that will affect buying today. It used to be called the "Greenspan Put." Now, it's (less frequently) called the "Bernanke Put."

I should clarify. I said "rates" when I should have said "yield." Yield includes stock dividend yield. And you look at an integrated yield curve, i.e. of the entire bond and stock market, not just Treasuries. I remember when the second round of QE was announced. It caused a sell-off in bonds and a HUGE rally in stocks because investors thought it was going to goose either the economy, inflation, both, or it was just plain money printing. When it came to an end, stocks sold off and the Treasuries rallied because, at least in part, QE was ending. (The other reason for the rally in Tbonds was Greece.)

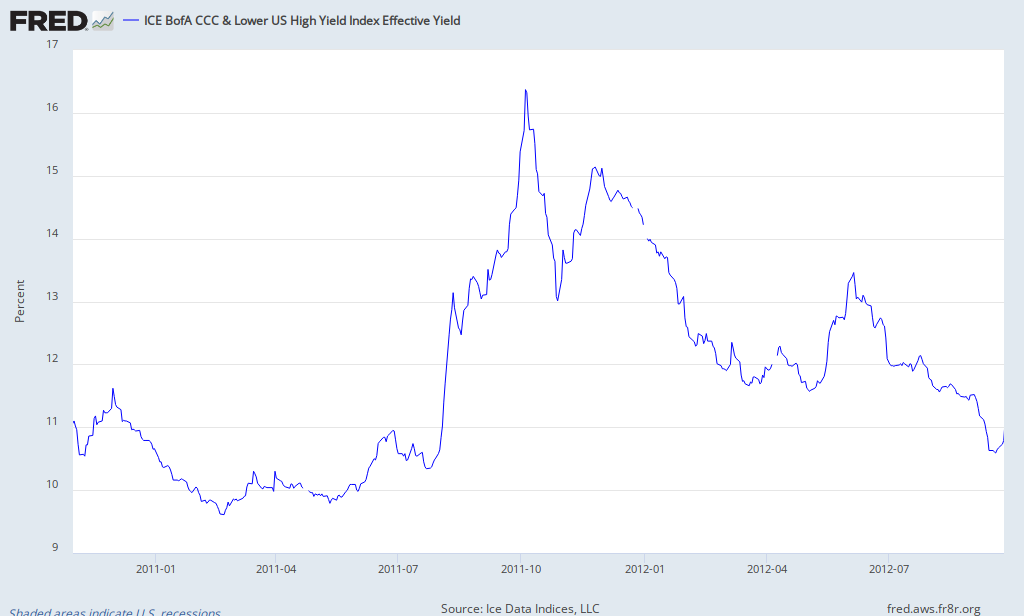

Low yields aren't exclusively because of QE. For certain, some of it has to do with a slowing global economy. But if it were entirely due to a slowing economy, you would expect high yield rates to have risen. But that isn't happening. In fact, high yield is about the same as it was when QE2 began whereas tbonds rates are significantly lower.

That is what I mean by the Fed having an influence right across the curve. The funds rate acts like an anchor to the entire bond market because spread products get bought when spreads get too wide. That buying lowers yields, or at least keeps them lower than they otherwise should be.

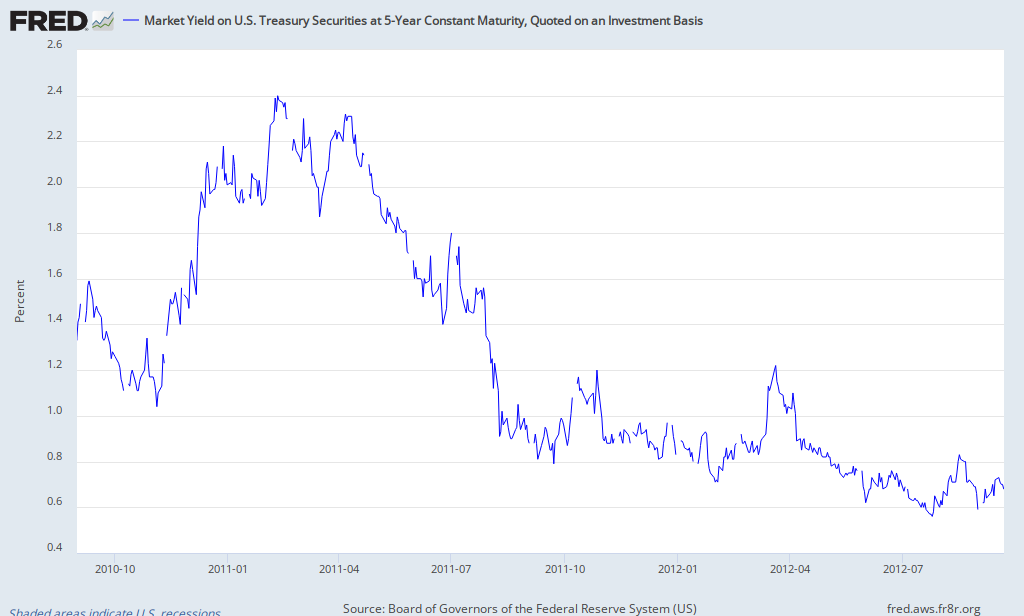

Anyways, here is the 5 year since.

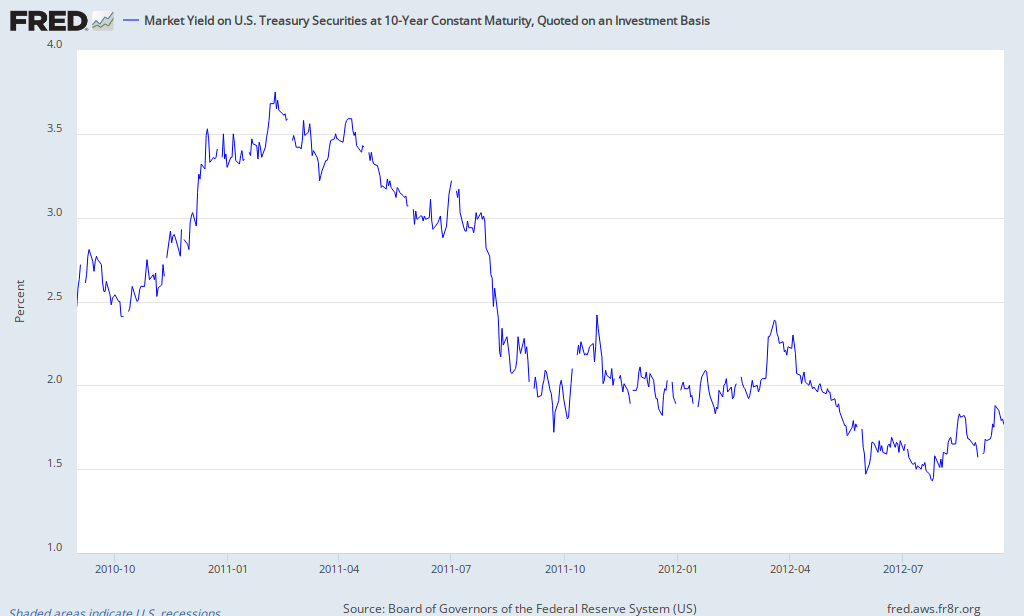

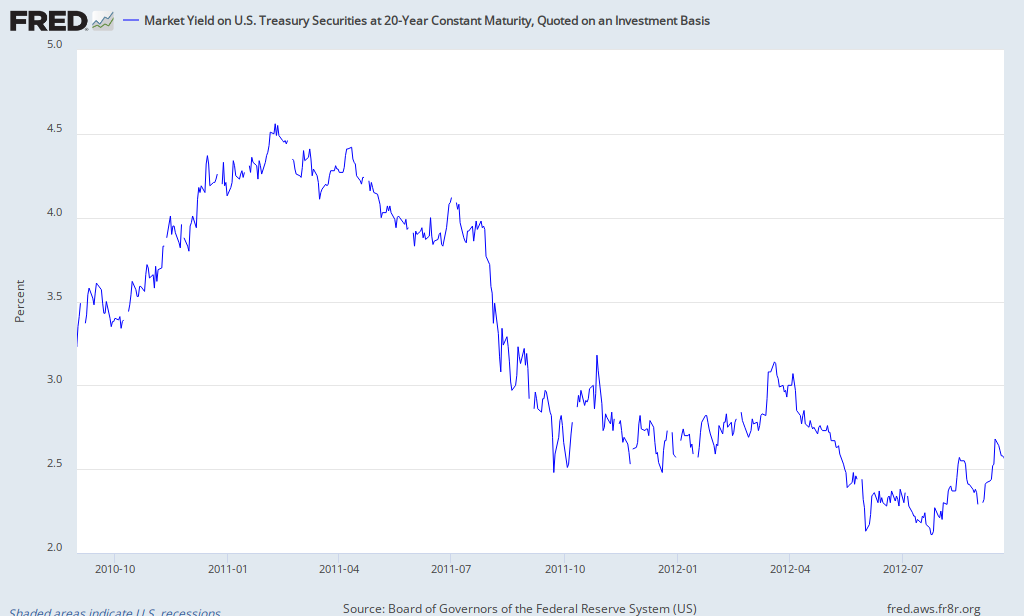

It brought the 10 year lower.

And the 30 year

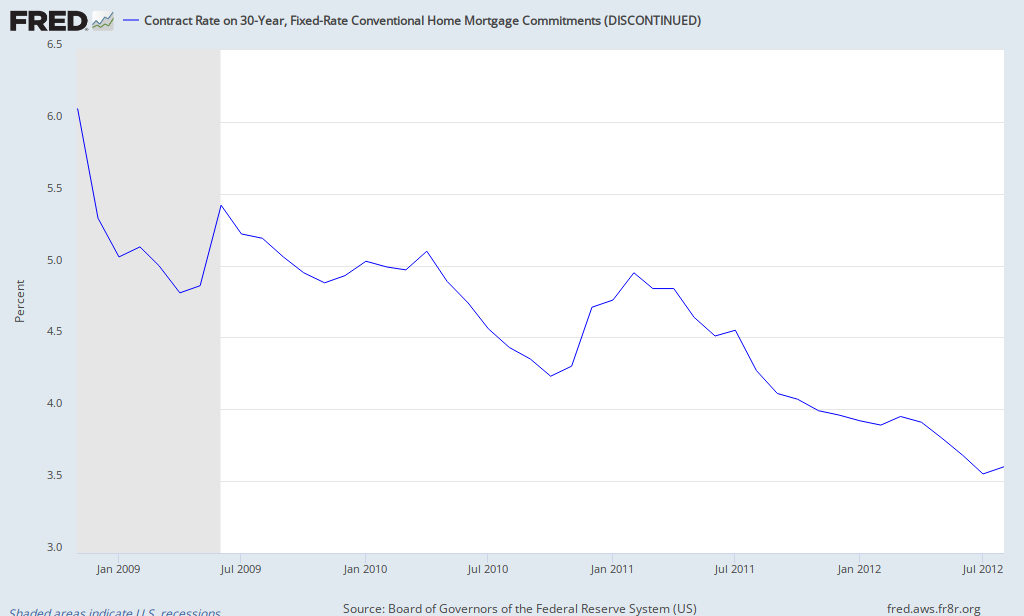

And, of course, mortgage rates have come down. The first round of QE began in November 2008.

Of course, that's not entirely due to QE, but if we're looking at hard dates to see if QE was effective, surely we can say that the Fed influenced the mortgage market.

In a piece published a few years ago, Goldman Sachs estimated that each $100 billion in QE lowered interest rates by 10 bps. If correct, rates are nearly 2% lower than they would otherwise be.

Also

ABSTRACT We evaluate the effect of the Federal Reserve’s purchase of long-term Treasuries and other long-term bonds (QE1 in 2008-09 and QE2 in 2010-11) on interest rates. Using an event-study methodology, we reach two main conclusions. First, it is inappropriate to focus only on Treasury rates as a policy target, because quantitative easing works through several channels that affect particular assets differently. We find evidence for a signaling channel, a unique demand for long-term safe assets, and an inflation channel for both QE1 and QE2, and a mortgage-backed securities (MBS) prepayment channel and a corporate bond default risk channel for QE1 only. Second, effects on particular assets depend critically on which assets are purchased. The event study suggests that MBS purchases in QE1 were crucial for lowering MBS yields as well as corporate credit risk and thus corporate yields for QE1, and Treasuries-only purchases in QE2 had a disproportionate effect on Treasuries and agency bonds relative to MBSs and corporate bonds, with yields on the latter falling primarily through the market’s anticipation of lower future federal funds rates.

The Federal Reserve has recently pursued the unconventional policy of purchasing large quantities of long-term securities, including Treasury securities, agency securities, and agency mortgage-backed securities (MBS). The stated objective of this quantitative easing (QE) is to reduce long-term interest rates in order to spur economic activity (Dudley 2010). There is significant evidence that QE policies can alter long-term interest rates. For example, Joseph Gagnon and others (2010) present an event study of QE1 that documents large reductions in interest rates on dates associated with positive QE announcements. Eric Swanson (2011) presents confirming event-study evidence from the 1961 Operation Twist, where the Federal Reserve purchased a substantial quantity of long-term Treasuries. Apart from the event-study evidence, there are papers that look at lower-frequency variation in the supply of long-term Treasuries and document its effects on interest rates (see, for example, Krishnamurthy and Vissing-Jorgensen 2010).1

www.kellogg.northwestern.edu/faculty/krisharvind/papers/QE.pdf