As you can clearly see the GSE's Fannie & Freddie were the biggest cause of the housing bubble & meltdown.

Incorrect. If the GSEs were the biggest causes of the financial meltdown, then GSE-funded loans would have driven up the prices of such homes the most. In fact, the opposite occurred. If you truly believe in the efficacy of the market, then GSE-funded homes should have risen the most. Didn't happen.

Also, the people making this argument seem to understand little of what happened outside the country's borders. Other countries such as Spain, Ireland, the UK, Canada, South Africa, Australia, China, etc., also experienced housing bubbles, most of those countries experiencing even bigger housing bubbles than America. This is a tad bit of an inconvenient fact to the ideologues pushing this line, but the GSEs do not lend money abroad.

Oh how stupid you are! Every day you dumbocraps regurgitate fact less talking points & lies trying to defend criminals only to get you ass kicked. Yet you somehow desire to get out of bed come on here & do it all over again. Maybe you are just to stupid to understand that the facts prove you wrong every single time.

THE KEY IS ENFORCEMENT, FEAR OF HAVING THE US ATTORNEY GENERAL SUE YOU INTO OBLIVION! --1995--"Attorney General Janet Reno, who had already won a number of bank lending discrimination settlements, sternly announces, "We will tackle lending discrimination wherever it appears." With the new policy in full force, "No loan is exempt; no bank is immune. For those who thumb their nose at us, I promise vigorous enforcement."

FEAR OF THE CONGRESSIONAL BLACK CAUCUS SCREWING UP YOUR BANKING BUSINESS.

FEAR OF HAVING THE US DEPARTMENT OF HOUSING & URBAN DEVELOPMENT SUE YOU INTO OBLIVION! [ame="http://www.youtube.com/watch?v=ivmL-lXNy64&feature=player_embedded"]HUD LAWSUIT[/ame]

NY Times - "But the storm has fallen with a special ferocity on black and Latino homeowners, the analysis shows. Defaults occur three times as often in mostly minority census tracts as in mostly white ones. Eighty-five percent of the worst-hit neighborhoods — where the default rate is at least double the regional average — have a majority of black and Latino homeowners."

--September 1999-- "A study by Freddie Mac, confirming earlier Federal Reserve and FDIC studies, contradicts race discrimination arguments for CRA. The study found that African-Americans with annual incomes of $65,000-$75,000 have on average worse credit records than whites making under $25,000. This showed that the difficulty in qualifying was not because of race but bad credit records. Accordingly, the Federal Reserve Bank of Dallas entitled a paper "Red Lining or Red Herring?" "City Journal warned that the Clinton administration had turned CRA into 'a vast extortion scheme against the nation's banks,'committing $1 trillion for mortgages and development projects, most of it funneled through the community organizers."

PEW Research Study - "From 1995 through the middle of this decade, homeownership rates rose more rapidly among all minorities than among whites. But since the start of the housing bust in 2005, rates have fallen more steeply for two of the nation's largest minority groups -- blacks and native-born Latinos -- than for the rest of the population"

THIS ALL PROVES BEYOND A SHADOW OF A DOUBT THAT THE CRA / GSE AFFIRMATIVE ACTION - SOCIALISM CAUSED THE ECONOMIC MELTDOWN!!! Just grow a spine & admit that the Congressional Black Caucus are racist who will stop at nothing to get more & more reparations from people who never benefited from & were never involved with slavery. Their poor credit scores & high default rates are due to the I am not paying the man because he owes me mentality. If OBAMACORN had spent half as much energy teaching minorities about credit & being responsible American citizens as they did going after banks this crisis would have been avoided. Instead they are taught to be African-American Dependants & how to stick it to the man.

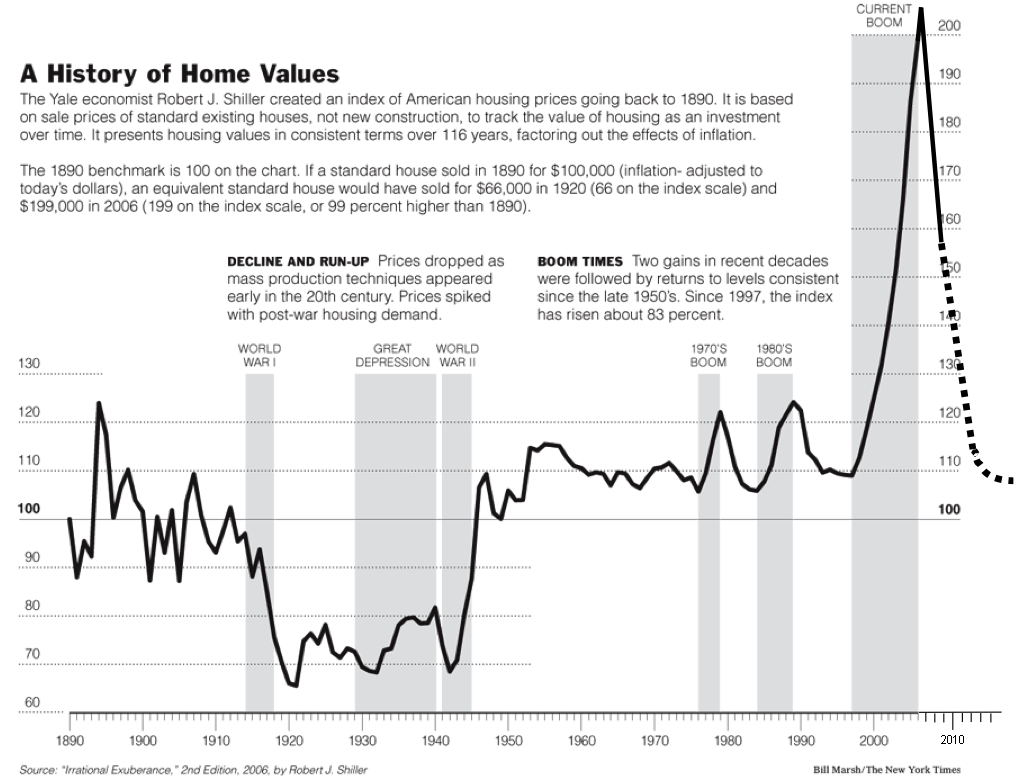

This chart shows just as clearly as that Democrat ass kissing brown nose on your stupid face that housing prices soared in 1997 when Clinton enforced the CRA. Also the GSE's Fannie & Freddie were & still the biggest part of the meltdown.

--Fall 1999-- Treasury Secretary Lawrence Summers issued a warning: "Debates about systemic risk should also now include government-sponsored enterprises, which are large and growing rapidly."

--September 1999-- New York Times "With pressure from the Clinton administration, Fannie Mae eased credit requirements on loans it would purchase from lenders, making it easier for banks to lend to borrowers unqualified for conventional loans. Fannie Mae's Raines explained that "there remain too many borrowers whose credit is just a notch below what our underwriting has required who have been relegated to paying significantly higher mortgage rates in the so-called subprime market."

With this action, Fannie Mae put itself at substantial risk in the event of an economic downturn. "From the perspective of many people, including me, this is another thrift industry growing up around us," warned Peter Wallison, a fellow in financial policy studies at the American Enterprise Institute (AEI). "If they fail, the government will have to step up and bail them out the way it stepped up and bailed out the thrift industry." The danger was known.

In 2008, Fannie and Freddie have purchased about 80% of all new home mortgages in the United States. Their combined investment portfolios held mortgage assets (loans and MBSs) valued at $1.5 trillion (as of June 30, 2008) - These GSE will never pay back tax payer for losses like all the banks have.