Can't you read?

Under Reagan, the debt went up $1.7 trillion, from $900 billion to $2.6 trillion.

But….the national wealth went up $ 17 trillion

Can't you calculate?

Profits ten times the debt

Obama would give anything to be able to point to Reagan's record of accomplishment vs his own record of utter and abject failure.

See what happens when you vote based on melanin versus ability?

why do you continually ignore the worst economy in many many years GWB handed down to Obama? Why do you make mock of that and feed me all these numbers that mostly don't mean squat What was the DOW under Reagan ??Under gwb?? Clinton left nothing to gwb like gwb left for Obama

"why do you continually ignore the worst economy in many many years GWB handed down to Obama?"

Au contraire, eddie.....I don't ignore it.....I related to the cause of same: Democrats and Democrat policies.

These:

1. Democrat FDR shredded the Constitution....ignoring article I, section 8, the enumerated powers.

He created GSE's Fannie, and his drones followed with Freddie, to do something the Constitution didn't authorize: meddle in housing.

2. Democrat Carter....the CRA, constraining banking policy

3. Democrat Clinton....strengthened the CRA

Under Clinton, HUD threatened banks, again, to give unrequited loans.

Henchmen: Democrats Cisneros and Cuomo.

4. Democrats Frank and Dodd barred any governmental discipline in this area.

It was Democrats and Democrat policies that caused the Mortgage Meltdown

That's the CliffNotes version.

Bush tried over and over to hold back the Democrats:

"Democrats Were Wrong on Fannie Mae and Freddie Mac

The White House called for tighter regulation 17 times.

Seventeen. That's how many times, according to

this White House statement (hat tip

Gateway Pundit), that the Bush administration has called for tighter regulation of the government-sponsored enterprises (GSEs) Fannie Mae and Freddie Mac.

Much if not all of that could have been prevented by a bill cosponsored by John McCain and supported by all the Republicans and opposed by all the Democrats in the Senate Banking Committee in 2005. That bill, which the Democrats stopped from passing, would have prohibited the GSEs from speculating on the mortgage-based securities they packaged. The GSEs' mission allegedly justifying their quasi-governmental status was to package or securitize such mortgages, but the lion's share of their profits—which determined top executives' bonuses—came from speculation."

http://www.usnews.com/opinion/blogs...rats-were-wrong-on-fannie-mae-and-freddie-mac

"Yet Barney Frank and his chums blocked all Bush's attempts to put a rein on Raines. During the House Financial Services Committee hearing following Bush's initiative, Frank declared: "The more people exaggerate a threat of safety and soundness [at Freddie Mac and Fannie Mae], the more people conjure up the possibility of serious financial losses to the Treasury which I do not see. I think we see entities that are fundamentally sound financially." His colleague on the committee, the California Democrat Maxine Walters, said: "There were nearly a dozen hearings where we were trying to fix something that wasn't broke. Mr Chairman, we do not have a crisis at Freddie Mac and particularly at Fannie Mae under the outstanding leadership of Mr Franklin Raines."

Bubble Meter: Barney Frank and Christopher Dodd deserve blame for Fannie and Freddie

THE LIARS KEEP GOING ON THIS DEAD HORSE I SEE

GSE Critics Ignore Loan Performance

Money talks. It says the only way to measure the quality of mortgage underwriting is to track loan performance delinquency and default rates, loss severity in comparison with the rest of the mortgage market. Otherwise, any analysis of the government-sponsored enterprises' role in housing finance is meaningless.

And yet, critics demanding GSE reform ignore the topic altogether. Search through any book or article promoting the thesis that the GSEs helped cause the mortgage crisis for a passage comparing GSE loan performance with the rest of the market. Almost certainly, you will come up empty-handed.

There is no data anywhere to cast doubt on the vastly superior loan performance of the GSEs. Year after year, decade after decade, before, during and after the housing crash, GSE loan performance has consistently been two-to-six times better than that of any other segment of the market. The numbers are irrefutable, and they show that the entire case against GSE underwriting standards, and their role in the financial crisis, is based on social stereotyping, smoke and mirrors, and little else.

https://www.americanbanker.com/opinion/gse-critics-ignore-loan-performance\

BUT DUBYA WANTED TO REFORM F/F? WEIRD HE HAD A GOP HOUSE FOR 6 YEARS WHICH BILL GOT THROUGH THE HOUSE AGAIN? YOU KNOW THE ONE DUBYA OPPOSED?

Bush talked about reform. He talked and he talked. And then he stopped reform. (read that as many times as necessary. Bush stopped reform). And then he stopped it again

Testimony from W's Treasury Secretary John Snow to the REPUBLICAN CONGRESS concerning the 'regulation of the GSE's 2004

Mr. (BARNEY) Frank: ...Are we in a crisis now with these entities?

Secretary Snow. No, that is a fair characterization, Congressman Frank, of our position. We are not putting this proposal before you because of some concern over some imminent danger to the financial system for housing; far from it.

June 17, 2004

(CNN/Money) - Home builders, realtors and others are preparing to fight a Bush administration plan that would require Fannie Mae and Freddie Mac to increase financing of homes for low-income people, a home builder group said Thursday.

Home builders fight Bush's low-income housing - Jun. 17, 2004

Private sector loans, not Fannie or Freddie, triggered crisis

The "turmoil in financial markets clearly was triggered by a dramatic weakening of underwriting standards for U.S. subprime mortgages, beginning in late 2004 and extending into 2007," the President's Working Group on Financial Markets

Private sector loans, not Fannie or Freddie, triggered crisis

Time to put you in your place???

Sure thing.

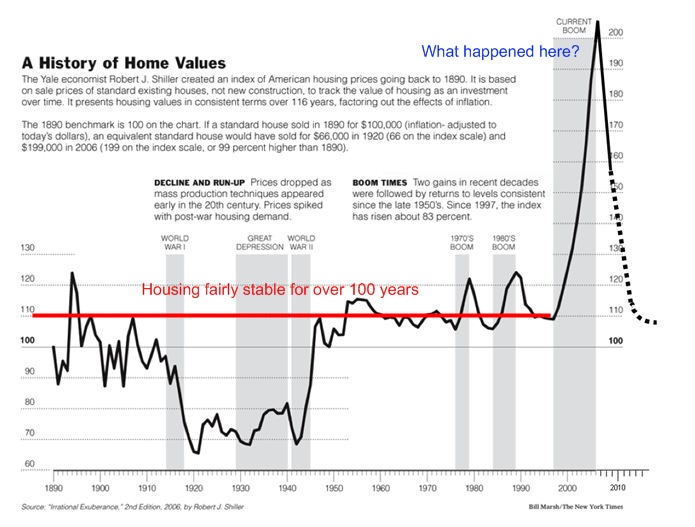

a. Congress passed a bill in 1975 requiring banks to provide the government with information on their lending activities in poor urban areas. Two years later, it passed the Community Reinvestment Act (CRA), which gave regulators the power to deny banks the right to expand if they didn’t lend sufficiently in those neighborhoods. In 1979 the FDIC used the CRA to block a move by the Greater NY Savings Bank for not enough lending.

b. In 1986, when the Association of Community Organizations for Reform Now (Acorn) threatened to oppose an acquisition by a southern bank, Louisiana Bancshares, until it agreed to new “flexible credit and underwriting standards” for minority borrowers—for example, counting public assistance and food stamps as income.

c. In 1987, Acorn led a coalition of advocacy groups calling for industry-wide changes in lending standards. Among the demanded reforms were the easing of minimum down-payment requirements and of the requirement that borrowers have enough cash at a closing to cover two to three months of mortgage payments (research had shown that lack of money in hand was a big reason some mortgages failed quickly).

d. ACORN then attacked Fannie Mae, the giant quasi-government agency that bought loans from banks in order to allow them to make new loans. Its underwriters were “strictly by-the-book interpreters” of lending standards and turned down purchases of unconventional loans, charged Acorn. The pressure eventually paid off. In 1992, Congress passed legislation requiring Fannie Mae and the similar Freddie Mac to devote 30 percent of their loan purchases to mortgages for low- and moderate-income borrowers.

e. Clinton Administration housing secretary, Henry Cisneros, declared that he would expand homeownership among lower- and lower-middle-income renters. His strategy: pushing for no-down-payment loans; expanding the size of mortgages that the government would insure against losses; and using the CRA and other lending laws to direct more private money into low-income programs.

f. Shortly after Cisneros announced his plan, Fannie Mae and Freddie Mac agreed to begin buying loans under new, looser guidelines. Freddie Mac, for instance, started approving low-income buyers with bad credit histories or none at all, so long as they were current on rent and utilities payments. Freddie Mac also said that it would begin counting income from seasonal jobs and public assistance toward its income minimum, despite the FHA disaster of the sixties.

g. Freddie Mac began an “alternative qualifying” program with the Sears Mortgage Corporation that let a borrower qualify for a loan with a monthly payment as high as 50 percent of his income, at a time when most private mortgage companies wouldn’t exceed 33 percent. The program also allowed borrowers with bad credit to get mortgages if they took credit-counseling classes administered by Acorn and other nonprofits. Subsequent research would show that such classes have little impact on default rates.

h. Pressuring nonbank lenders to make more loans to poor minorities didn’t stop with Sears. If it didn’t happen, Clinton officials warned, they’d seek to extend CRA regulations to all mortgage makers. In Congress, Representative Maxine Waters called financial firms not covered by the CRA “among the most egregious redliners.”

i. Mortgage Bankers Association (MBA) shocked the financial world by signing a 1994 agreement with the Department of Housing and Urban Development (HUD), pledging to increase lending to minorities and join in new efforts to rewrite lending standards. The first MBA member to sign up: Countrywide Financial, the mortgage firm that would be at the core of the subprime meltdown.

j. A 1998 sales pitch by a Bear Stearns managing director advised banks to begin packaging their loans to low-income borrowers into securities that the firm could sell. Forget traditional underwriting standards when considering these loans, the director advised. For a low-income borrower, he continued in all-too-familiar terms, owning a home was “a near-sacred obligation. A family will do almost anything to meet that monthly mortgage payment.” Bunk, says Stan Liebowitz, a professor of economics at the University of Texas: “The claim that lower-income homeowners are somehow different in their devotion to their home is a purely emotional claim with no evidence to support it.”

k. Any concern was quickly dismissed. When in early 2000 the FDIC proposed increasing capital requirements for lenders making “subprime” loans—loans to people with questionable credit, that is—Democratic representative Carolyn Maloney of New York told a congressional hearing that she feared that the step would dry up CRA loans. Her fellow New York Democrat John J. LaFalce urged regulators “not to be premature” in imposing new regulations.

l. In July 1999, HUD proposed new levels for Fannie Mae’s and Freddie Mac’s low-income lending; in September, Fannie Mae agreed to begin purchasing loans made to “borrowers with slightly impaired credit”—that is, with credit standards even lower than the government had been pushing for a generation.

m. In 2004 Congress pressed new affordable-housing goals on the two mortgage giants, which through 2007 purchased some $1 trillion in loans to lower- and moderate-income buyers. The buying spree helped spark a massive increase in securitization of mortgages to people with dubious credit.

n. In October 1994, Fannie Mae head James Johnson had reminded a banking convention that mortgages with small down payments had a much higher risk of defaulting. (A Duff & Phelps study found that they were nearly three times more likely to default than conventional mortgages.) Yet the very next month, Fannie Mae said that it expected to back loans to low-income home buyers with a 97 percent loan-to-value ratio—that is, loans in which the buyer puts down just 3 percent—as part of a commitment, made earlier that year to Congress, to purchase $1 trillion in affordable-housing mortgages by the end of the nineties. According to Edward Pinto, who served as the company’s chief credit officer, the program was the result of political pressure on Fannie Mae trumping lending standards.

o. In 1992, the Boston Fed produced an extraordinary 29-page document that codified the new lending wisdom. Conventional mortgage criteria, the report argued, might be “unintentionally biased” because they didn’t take into account “the economic culture of urban, lower-income and nontraditional customers.” Lenders should thus consider junking the industry’s traditional income-to-payments ratio and stop viewing an applicant’s “lack of credit history” as a “negative factor.” Further, if applicants had bad credit, banks should “consider extenuating circumstances”—even though a study by mortgage insurance companies would soon show, not surprisingly, that borrowers with no credit rating or a bad one were far more likely to default. If applicants didn’t have enough savings for a down payment, the Boston Fed urged, banks should allow loans from nonprofits or government assistance agencies to count toward one. A later study of Freddie Mac mortgages would find that a borrower who made a down payment with third-party funds was four times more likely to default, a reminder that traditional underwriting standards weren’t arbitrary but based on historical lending patterns.

p. The Congressional Hispanic Caucus launched Hogar in 2003, an initiative that pushed for easing lending standards for immigrants, including touting so-called seller-financed mortgages in which a builder provided down-payment aid to buyers via contributions to nonprofit groups. As a result, mortgage lending to Hispanics soared. And today, in districts where Hispanics make up at least 25 percent of the population, foreclosure rates are now nearly 50 percent higher than the national average, according to a Wall Street Journal analysis.

q. Republicans and Democrats, meanwhile, have scrambled to reignite the housing market through ill-conceived tax credits and renewed federal subsidies for mortgages, including the Obama administration’s mortgage bailout plan, which recalls the New Deal’s HOLC. Behind these efforts is a fundamental misconception among politicians that housing drives the American economy and therefore demands subsidy at virtually any cost. Our praiseworthy initial efforts—to eliminate housing discrimination and provide all Americans an equal

opportunity to buy a home—were eventually turned on their heads by advocates and politicians, who instead tried to ensure equality of

outcomes.

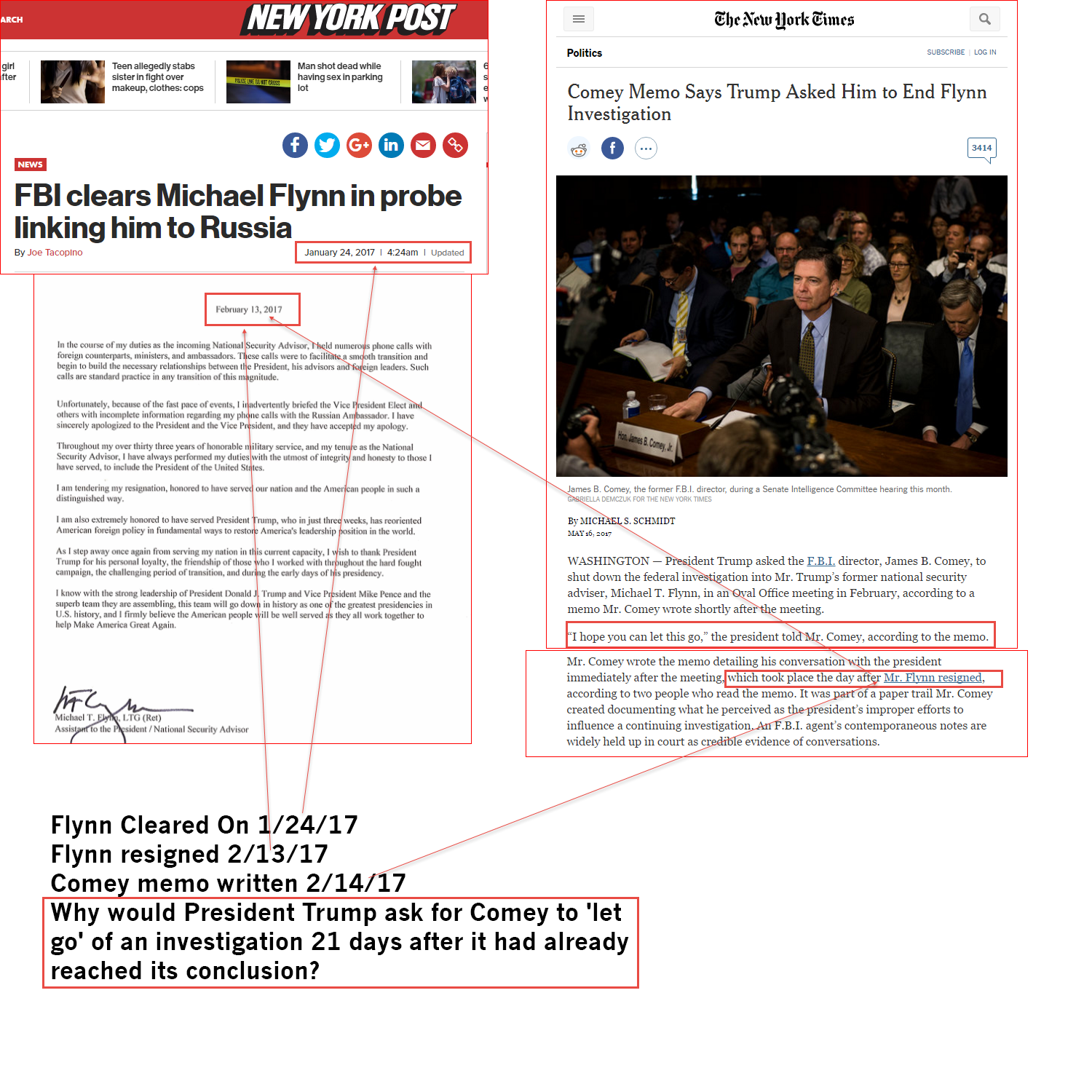

Timeline shows Dems were warned:

")