What makes you think the Fed controls it?

For instance, what did the Fed do during the Great Depression to shrink money supply by 1/3rd?

why try to change subject????

so for 4th time who controls the money supply if not the Fed and what makes you think they control it????

It's slow work trying to educate you.

I'd rather not hold your hand, you're not a child, are you?

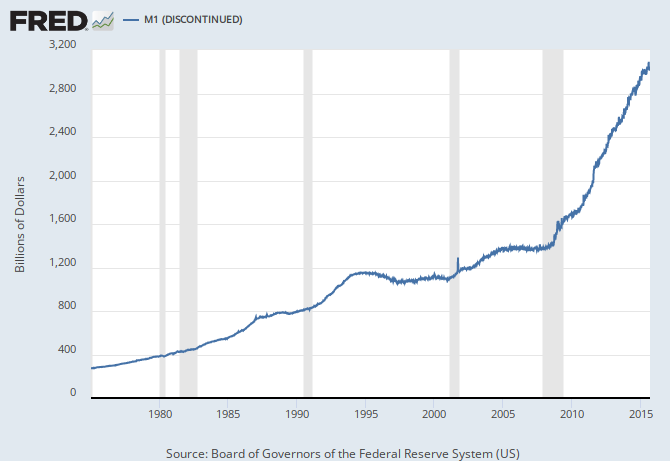

Did you ever learn what makes up money supply?

For instance, what makes up M2?

why try to change subject????

so for 5th time who controls the money supply if not the Fed and what makes you think they control it????

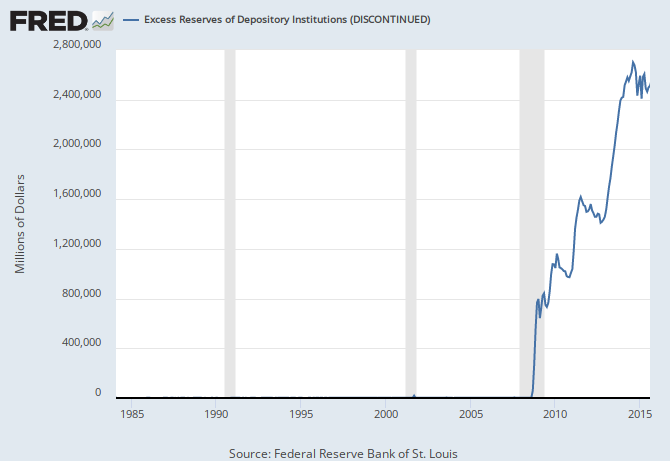

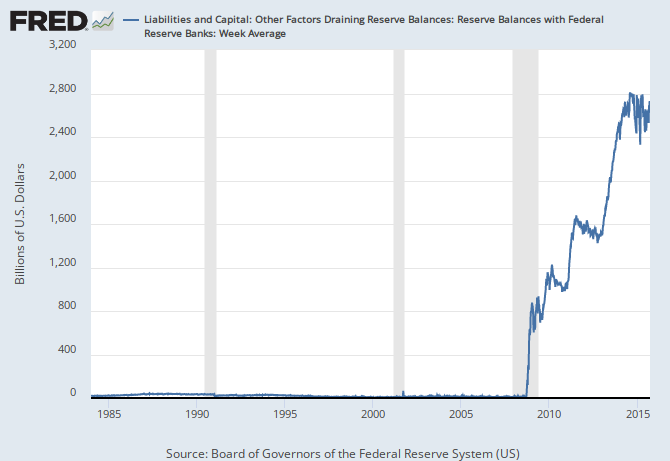

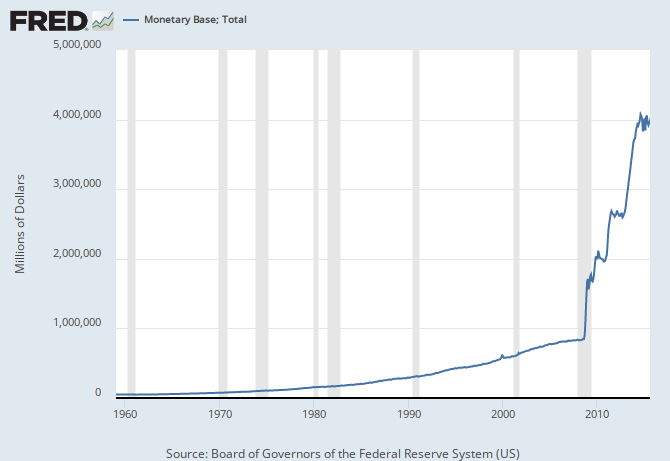

The series equals total balances maintained plus currency in circulation.

Ringing any bells yet?

wow you seem like such a smart guy....... so why are you trying so hard to change subject??

so for 6th time who controls the money supply if not the Fed and what makes you think they control it????

Have you digested the various monetary measurements yet?

Or do I have to wait before I attempt to educate you further?