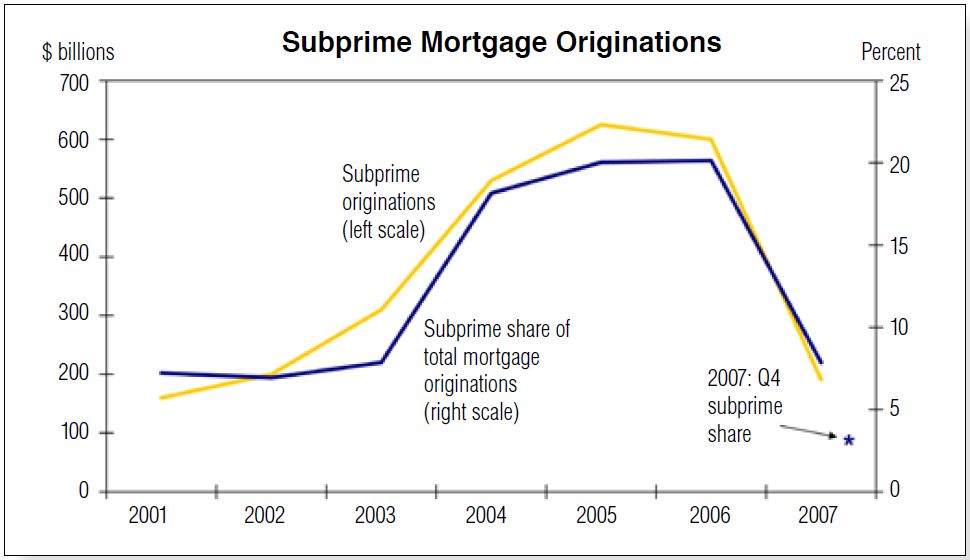

What's that, that loans done under Gov't regulations 2004-2007 were better performing by 450%-600%? lol

VA loans are a very small percentage of the overall mortgage portfolio, in fact when a VA loan is 30 days late the VA has created The Loan Guaranty Program to assist in helping veterans avoid foreclosure. The Zero Down Payment VA Loan doesn't really exist anymore. There is a funding fee that starts at 3% and varies depending on a number of issues, i.e. disability, number of times it has been used by the veteran, not to mention it is one of the toughest to make appraised value, and in most cases the seller will not come down so the veteran has to make up the difference out of pocket or walk away. But you would have to know what you where talking about. I'll keep teeing your dumb dumb ass up...

Your buddy Jimmy Carter the 2nd biggest f'up behind Oblammer to occupy the POTUS created CRA in '77. In 1995 Bubba Clintoon revised CRA and by the 4th quarter of '96 he created FHA Down Payment Assistance. This FHA program dominated the FHA portfolio for over the next decade plus. For as little as $0 down you could own the American Dream. During this housing boom FHA Loans were 40% of Loan Originations. These are simple facts you can find with your friend Google.

Just a little fact that you seem to not know about...

"Elimination of Non Profit Down Payment Assistance: On July 30, 2008, President Bush signed the Housing and Economic Recovery Act of 2008 which prohibits seller-funded DPA (Down Payment Assistance) for loans backed by the Federal Housing Administration. Prior to this bill, the seller could contribute up to 6% to the buyer to cover either a down payment or closing costs on an FHA loan. The changes took effect on Oct. 1, 2008. We provide this information for reference only. These grants are no longer available."

Funny how the IRS thought Bubba Clintoon's FHA DPA programs where a scam...

"On May 27, 2006, the IRS issued Revenue Ruling 2006-27, categorizing the non-profit seller funded down payment assistance programs (DPA programs) as "scams."[11] The IRS ruled that organizations such as AmeriDream and Partners in Charity are no longer eligible for non-profit status and are not acting as "charitable organizations" as defined by the IRS. This ruling was based largely on the circular nature of the cash flows, in which the seller pays the charity a "fee" after closing. Many believe that the "grant" is really being rolled into the price of the home. According to the Government Accountability Office, there are higher default and foreclosure rates for these mortgages.[12]"

The grant was rolled into the price and absorbed through the appraisal. Today there is a buffer between loan officer and appraisal group by design. LO's cannot speak directly with the appraiser, I wonder why?!?!?!

As I have pointed out before Sub Prime was a minimum 80% to 70% LTV before the FHA DPA mentality was born by Bubba Clintoon, but you would have to know what you were talking about to understand this...

The copy below is where it really sticks to Clintoon's ass, I can't make this shit up...

"Born was appointed to the CFTC on April 15, 1994 by President Bill Clinton. Due to litigation against Bankers Trust Company by Procter and Gamble and other corporate clients, Born and her team at the CFTC sought comments on the regulation of over-the-counter derivatives,[4] a first step in the process of writing CFTC regulations to supplement the existing regulations of the Federal Reserve System, the OCC, and the National Association of Insurance Commissioners. Born was particularly concerned about swaps, financial instruments that are traded over the counter between banks, insurance companies or other funds or companies, and thus have no transparency except to the two counterparties and the counterparties' regulators, if any. CFTC regulation was strenuously opposed by Federal Reserve chairman Alan Greenspan, and by Treasury Secretaries Robert Rubin and Lawrence Summers.[5] On May 7, 1998, former SEC Chairman Arthur Levitt joined Rubin and Greenspan in objecting to the issuance of the CFTC’s concept release. Their response dismissed Born's analysis and focused on the hypothetical possibility that CFTC regulation of swaps and other OTC derivative instruments could create a "legal uncertainty" regarding such financial instruments, hypothetically reducing the value of the instruments. They argued that the imposition of regulatory costs would "stifle financial innovation" and encourage financial capital to transfer its transactions offshore.[11] The disagreement between Born and the Executive Office's top economic policy advisors has been described not only as a classic Washington turf war,[9] but also a war of ideologies,[12] insofar as it is possible to argue that Born's actions were consistent with Keynesian and neoclassical economics while Greenspan, Rubin, Levitt, and Summers consistently espoused neoliberal, and neoconservative policies."

Are you having a problem with a rebuttal on USDA Loans Census Tract question I gave you? Did you finally figure out what the population limit is and that one of your hero's keeps signing Executive Orders forgoing the laws requirements on population?

The three year period you keep harping on had a long road before the Mortgage Meltdown and two of your hero's laid the eggs that ultimately hatched the 3rd QTR '08 collapse...

You're not alone, there are a lot of f'ing idiots that will keep you company that do not want to accept the burden is on Carter and Clinton...

It's pretty clear you're lineage was part of the "Flat Earth" society...

Also, I think it's safe to say you will probably never learn the Mortgage Meltdown of 2008 was born long before Bush 43 took office...

I am starting to feel embarrassed for you...

Does motherto3 know how someone on the internet owns your ass?

YOUR LINK BUBBA

"From 2000 to 2004, the total proportion of FHA-insured single-family purchase money loans that had an LTV ratio greater than 95 percent and that also involved down payment assistance, from any source, grewfrom 35 to nearly 50 percent"

"... Approximately 6 percent of FHA-insured loans received down payment assistance from nonprofit organizations in 2000, but, by 2004 this figure had grown to about 30 percent"

..."

As figure 2 illustrates, the total number of FHA-insured loans originated fell dramatically between 2001 and 2005. Realtors that we spoke to from across the country told us that fewer homebuyers were using FHA-insured

mortgages, opting instead for conventional low and zero down payment

mortgage products and loans with secondary financing that do not require

private mortgage insurance. In addition, officials from government

agencies that provide down payment assistance noted either a decrease in

the use of FHA mortgage insurance, an increase in the demand for

conventional mortgages, or both"

WEIRD RIGHT?

"Although the number of FHA-insured loans decreased markedly from 2001

to 2004, the number of FHA-insured loans with down payment assistance

did not. As a result, these loans constitute a growing share of FHA’s total

portfolio"

WHAT? YOU MEAN THE EXECUTIVE BRANCH OVERSIGHT OF DUBYA

"States that have higher-than-average percentages of FHA-insured loans

with nonprofit down payment assistance, primarily from seller-funded

programs, tend to be states with lower-than-average house price

appreciation rates (fig. 3). From May 2004 to April 2005, 34.6 percent of all

FHA-insured purchase money loans nationwide involved down payment

assistance from a nonprofit organization, and 15 states had percentages

that were higher than this nationwide average. Fourteen of these 15 states

also had house price appreciation rates that were below the median rate for

all states. In addition, the eight states with the lowest house appreciation

rates in the nation all had higher-than-average percentages of nonprofit

down payment assistance. Generally, states with high proportions of FHA-

insured loans with nonprofit down payment assistance were concentrated

in the Southwest, Southeast, and Midwest"

OH SO NOT THE AREAS HIT HARD BY DUBYA'S SUBPRIME BUBBLE? LOL

AGAIN, GOV'T BACKED LOANS PERFORMED 450%-600% BETTER THAN PRIVATE MARKET LOANS 2004-2007, HOW IS THAT POSSIBLE? lol

http://www.gao.gov/new.items/d0624.pdf

FACTS on Dubya s great recession US Message Board - Political Discussion Forum