Seymour Flops

Diamond Member

6:30:

She explains to him that "premiums" will not be going up once the COVID subsidies are allowed to expire. Premiums wills still be at the same incredibly high rate that they quickly rose to once Obamacare passed. The change in January will only result in one subsidy not being paid to insurance companies. The overwhelming majority of the premium will be paid for by tax dollars.

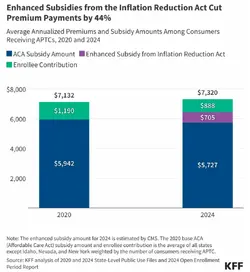

Here is a visual from KFF, AKA Kaiser:

If the enhanced subsidies — the purple bar in the 2024 column — go away, a family would have to pay that amount out-of-pocket, which would get added to the green bar above it. But the federal government would still pay for the vast majority of premium costs, the blue bar in the graph. In this case, the federal government would fund “only” 78 percent of premiums, as opposed to 88 percent of the total premium under the enhanced subsidies.

The shocking part is how much premiums were able to skyrocket, once consumers were no longer paying for the majority of them. Clearly, the insurance companies pushed premiums up enough to capture the premium, while leaving consumers still experiencing climbing out of pocket payments for their share of the premiums.

In other words, there is no evidence that this has anything to do with how much it costs an insurance provider to provide coverage, but instead is based on what the market will bear. Once Uncle Sam gives a boost, the market can bear a huge increase.

She explains to him that "premiums" will not be going up once the COVID subsidies are allowed to expire. Premiums wills still be at the same incredibly high rate that they quickly rose to once Obamacare passed. The change in January will only result in one subsidy not being paid to insurance companies. The overwhelming majority of the premium will be paid for by tax dollars.

Here is a visual from KFF, AKA Kaiser:

If the enhanced subsidies — the purple bar in the 2024 column — go away, a family would have to pay that amount out-of-pocket, which would get added to the green bar above it. But the federal government would still pay for the vast majority of premium costs, the blue bar in the graph. In this case, the federal government would fund “only” 78 percent of premiums, as opposed to 88 percent of the total premium under the enhanced subsidies.

The shocking part is how much premiums were able to skyrocket, once consumers were no longer paying for the majority of them. Clearly, the insurance companies pushed premiums up enough to capture the premium, while leaving consumers still experiencing climbing out of pocket payments for their share of the premiums.

In other words, there is no evidence that this has anything to do with how much it costs an insurance provider to provide coverage, but instead is based on what the market will bear. Once Uncle Sam gives a boost, the market can bear a huge increase.