The Derp

Gold Member

- Apr 12, 2017

- 9,620

- 661

- 205

- Banned

- #1,341

Mortgages bought during the bubble, with skyrocketing home prices, lower down payments and weaker borrowers were most certainly worse than mortgages bought pre-bubble.

The mortgages the GSE's were buying were the same pre-bubble as they were during the bubble. We have the delinquency figures to tell us that. So you again, are ignoring the facts. Why?

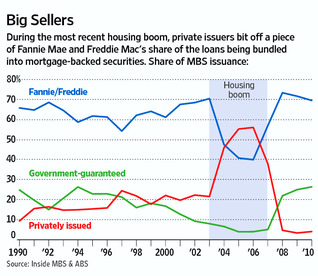

That's why the line on the chart below for GSE's remains steady and consistent

Yes, your ignorance of what the chart says is obvious to me.

The chart here clearly shows the subprime bubble popped beginning in 2006 as delinquency rates for private-label subprimes rose. All other loans, including GSE-backed loans, FHA loans, and non-prime loans saw their delqinuency rates rise nearly two years after the rates for private label subprimes began to rise. Which means, quite clearly, that the private label subprimes were responsible for the bubble and not the GSE's.