Blaming society? FHA DPA was a direct result of Clinton turning up the heat on banks with the CRA, Sub Prime prior to this was a 20%+ DP with rates at 4 to 5 percent above par.....

Those individuals you're describing wouldn't be Clinton, Greenspan, Summer, Rubin and Levitt? Didn't they claim Brooksley Born was way off about the derivatives market? That didn't hold water either....

The goal to open up housing to anyone that could put fog on a mirror was a bad idea, and they used every means possible to do it, the CRA is were it all started, don't stay in denial too long....

If a car speeds by you 50 mph above the speed limit, it doesn't force you or everyone else to drive 50 mph above the speed limit either. You make a choice to do so.

Individuals made conscious decisions of their own volition to extend horrendous loans that had absolutely zero, zip, nada to do with the CRA. A sliver of the mortgage market did NOT cause bank executives and lending officers to start acting like madmen. Credit standards always wax and wane in the cycle, but no government policy forced banks and other mortgage providers to extend NINJAs to speculators flipping condos.

How about this analogy, lets put a 55 gallon barrel full of jelly beans in a class room of 8 year olds and tell them they can't have any, in 24 hours half will be gone and everyone of them will swear they don't know what happened....

This is a over simplification of the CRA effect on the industry, but it makes it easier for people outside of the industry to understand....

I worked for one of the largest builders in the nation during this time, I am still in the industry today. Our COO met quarterly with Raine's and annually with Greenspan, Raine's did not have another agenda, but to open the doors to low income minority home ownership.....

Here is a clear and factual point to CRA's effect on the industry, you can debate this all you want....

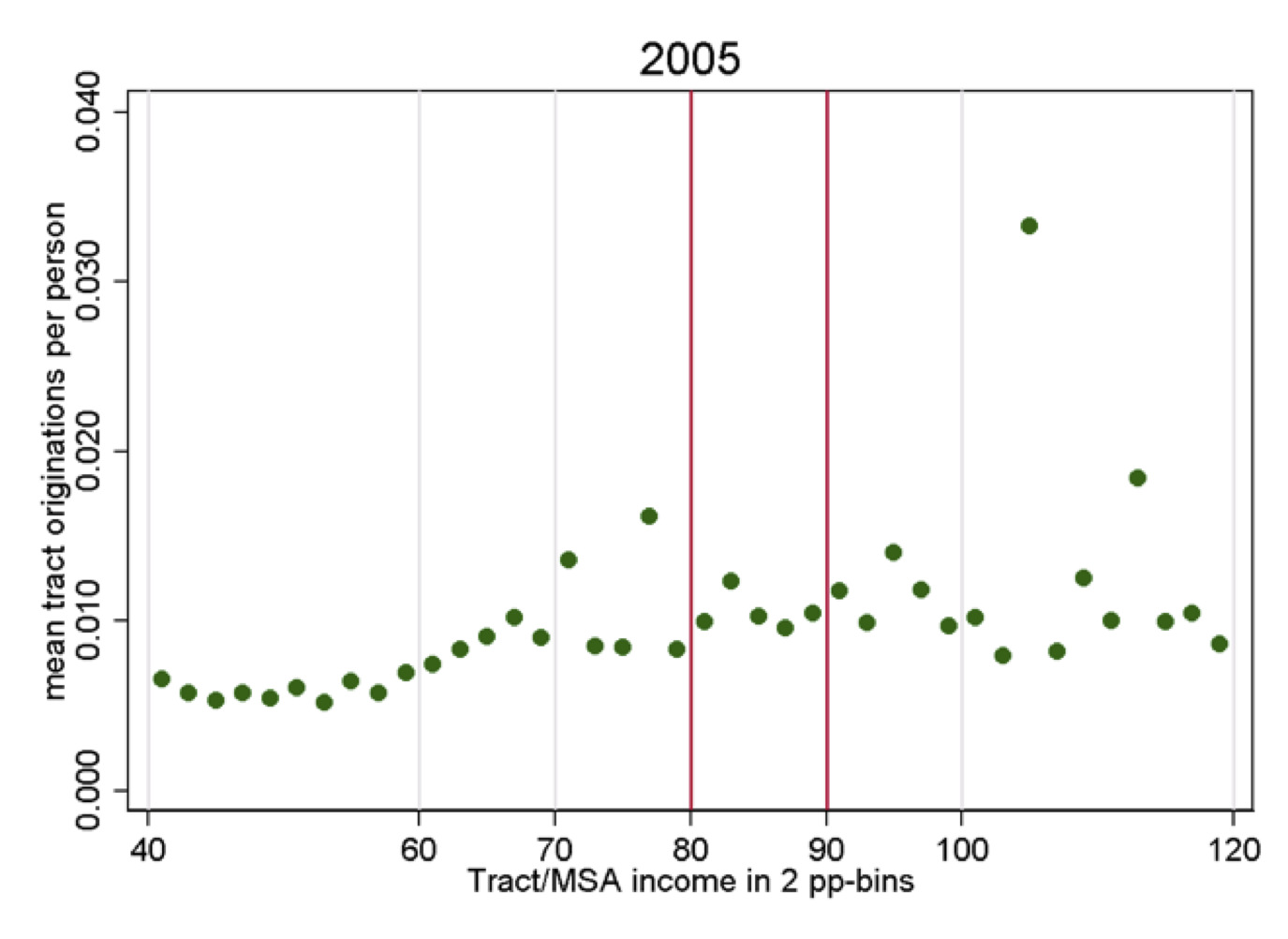

These three loan types helped the GSEs meet their affordable housing (AH) mandates under the "Federal Housing Enterprises Financial Safety and Soundness Act of 1992" (GSE Act). They were materially assisted in this effort by big banks and thrifts originating trillions in high risk loans to meet another mandate established under the federal Community Investment Act (CRA).

Speaking of CRA, let us not forget Krugman's assertion that CRA's involvement in the financial crisis is a myth. Over the 17 year period 1992-2008, there was a total of $6 trillion in announced CRA commitments, covering all types of CRA lending. Ninety-four percent of this $6 trillion in commitments were issued by four banks or banks these four ended up purchasing by way of merger. The banks were Wells Fargo, JP Morgan Chase, Citibank, and Bank of America. As a result, CRA single family origination volume over the period 1993-2008 also exploded, totaling an estimated $2.7 trillion.

RealClearMarkets - How Did Paul Krugman Get It So Wrong?

Edward Pinto is a consultant to the mortgage-finance industry and was the chief credit officer at Fannie Mae in the 1980s

I have seen this on a day to day basis for the last 18 years.....

On 1/15/2011 Wells Fargo introduced FHA lending starting at 500 to 579 FICO scores with 10% DP, 580 to 599 with 5% DP and 600+ (lowest in the industry by 20 points) with 3.5% DP. All of this is per the FHA regs. It will be interesting to say the least how the nations 4th largest bank will do this, they are going to get slammed with loan apps....