expat_panama

Gold Member

- Apr 12, 2011

- 3,899

- 814

- 130

For the past three years, the Justice Department has filed a series of bruising lawsuits against U.S. lenders for race discrimination while hiding behind opaque investigative methods and hoping banks don't challenge the cases in court. But while most banks have quietly settled the record number of lending-bias claims, some are fighting back against what they call a never-ending "witch hunt."

In interviews with IBD, bankers and their lawyers complain that Attorney General Eric Holder and his army of civil-rights prosecutors have built their cases around dubious statistical models instead of complaints from actual victims of discrimination.

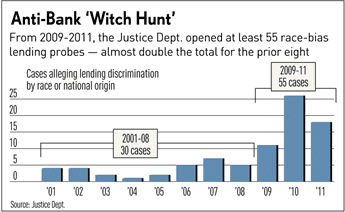

The DOJ filed at least 55 race-bias claims vs. lenders in 2009-11, up from just 30 in the prior eight years. Bank executives say the government's econometric models, which crunch reams of public loan data, don't dig down into race-neutral factors. If prosecutors did, bankers say, they would see that differences in credit risk explain racial differences in lending and pricing, and that any "disparities" reflect prudent business decisions.

They point out, moreover, that most of Holder's racism charges are based on "disparate impact."

The legal theory reduces the standard of proof to mere speculation of intent to discriminate. Basically, all prosecutors have to show is that lending decisions adversely impact minorities in a "statistically significant" way.

The Supreme Court could reject or restrict "disparate impact" in lending if justices ever hear such a case. Holder apparently agrees.

[snip]

(Excerpt) Read more at news.investors.com ...

In interviews with IBD, bankers and their lawyers complain that Attorney General Eric Holder and his army of civil-rights prosecutors have built their cases around dubious statistical models instead of complaints from actual victims of discrimination.

The DOJ filed at least 55 race-bias claims vs. lenders in 2009-11, up from just 30 in the prior eight years. Bank executives say the government's econometric models, which crunch reams of public loan data, don't dig down into race-neutral factors. If prosecutors did, bankers say, they would see that differences in credit risk explain racial differences in lending and pricing, and that any "disparities" reflect prudent business decisions.

They point out, moreover, that most of Holder's racism charges are based on "disparate impact."

The legal theory reduces the standard of proof to mere speculation of intent to discriminate. Basically, all prosecutors have to show is that lending decisions adversely impact minorities in a "statistically significant" way.

The Supreme Court could reject or restrict "disparate impact" in lending if justices ever hear such a case. Holder apparently agrees.

[snip]

(Excerpt) Read more at news.investors.com ...